2021 Review

If global news flow in 2020 was dominated by a lethal virus that originated in China, 2021 in emerging markets (EM) were subject to countless policy related headlines placing a question mark over the health of investing in Chinese equities. Although 2021 was notable for strong equity markets globally as a result of a post Covid-19 vaccine fueled recovery, MSCI China fell 21.7%. While many parts of the asset class posted strong returns, China was the notable laggard. MSCI EM therefore fell 2.5% despite MSCI EM ex-China appreciating 10%. While China accounts for approximately one third of MSCI EM, for EM overall to produce robust returns in 2022, a reversal in Chinese fortunes will be essential. Below we will review 2021 and discuss our expectations for 2022.

To begin with sectors, the worst were those dominated by the most troubled Chinese areas – consumer internet related stocks and real estate – consumer discretionary fell 29%, real estate 22% and communication services 9%. While the portfolio had no exposure to real estate and was underweight discretionary, an overweight to communication services combined with poor stock selection weighed on relative and absolute performance. The portfolio’s overweight to IT however added over 300 basis points in value given strong performance across most names held. We remain overweight given the long term structural growth in sustainable demand we envisage for products and services. Energy was the strongest sector given the oil price rally during the year. The portfolio was roughly in line with the benchmark weight and slightly added value from energy stock selection.

EMEA

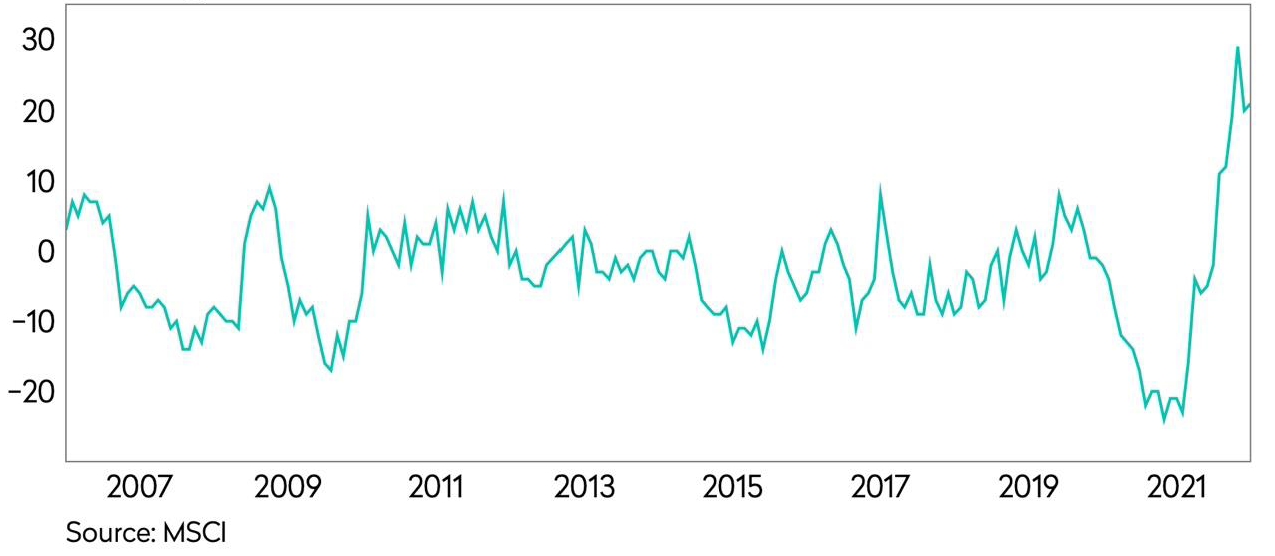

Given strong energy prices, the best performing region last year was the Middle East which gained 35% as did Saudi Arabia, making it the best performing ‘major’ market. We have no exposure to the region as we have struggled to find value there, especially when we layer on the ESG risks we consider. The underweight here cost approximately 150 bps in relative performance. Strong energy markets also helped Russia post a 19% gain. We are slightly underweight Russia but do own oil major Lukoil which gained 28%. However, our other holding is a gold company, Polymetal, which fell during the year and therefore saw us lose 30 bps from Russian positioning. When we layer on top our zero exposure to Central Eastern European markets which also outperformed, we lost c.200 bps in total from being underweight the EMEA region. This positioning was the main reason for our underperformance in 2021. In fact, as can be seen in the chart below, last year’s outperformance of EMEA was the greatest versus EM on record. Hence, any mean reversion this year would help us regain some of this lost alpha which we think is likely given relatively lofty valuations in the Middle East in particular.

Rolling 12-Month Relative Performance of MSCI EMEA over MSCI EM

Latin America

Latin America was the weakest region as many countries exhibited political volatility amid a disappointing response to Covid-19, and continuing structural challenges dampening growth. Brazil, Peru, Chile and Colombia all fell between 17-20%, with only Mexico posting a positive return of 22.5%. Our positioning in the region was mixed with zero exposure to Colombia and Chile helping, as did the holding in the Mexican bank, Banorte, and more defensive stock selection in Brazil. However, this was somewhat offset by an overweight to Peru via the holding in the leading bank, Credicorp. We remain cautious towards Brazil ahead of the presidential election in October 2022, which often creates heightened volatility, but do see deep value in some names so have moved slightly overweight while retaining a natural currency hedge through our exposures. We also added to Credicorp given particularly attractive long term valuations.

Asia

Asia was extremely mixed. Taiwan continued to deliver above average returns, +26%, as semiconductor stocks such as TSMC, UMC and Mediatek made large gains on the back of sustained high demand for their chips and manufacturing services. The portfolio is overweight Taiwan and added value as a result. We continue to find value opportunities in Taiwan although we have taken profits throughout the year. India was also strong, adding 26% as stocks across sectors performed well as the economy bounced back from a Covid-19 induced slump. We started the year overweight India but valuations look less attractive now given the outperformance, and hence we have taken profits from software holdings, Infosys and HCL Tech, as well as Reliance Industries. We ended the year underweight India. Korea fell 8% and we took advantage of weakness to move the portfolio from an underweight to neutral position as certain stocks in the memory, EV battery and financials sectors look especially undervalued.

China

The main area dragging down EM though was of course China. Investors sold Chinese stocks during the year for three principal reasons.

- Concerns regarding a more severe and unpredictable regulatory environment.

- Concerns for the VIE structure used for most US listed ADRs, and some Hong Kong stocks.

- Concerns for the underlying health of the Chinese economy as a result of the country’s largest property developer defaulting on its debt.

We have already written at length explaining our China views in the Q3 Focus piece on China.

In short, while we are cognizant of all the above, we believe there is a great deal of bad news discounted in many China stocks now. While the regulatory environment can be unpredictable, as we enter 2022, investors and crucially the companies themselves are now fully aware of how serious the Chinese authorities are in achieving their goal of ‘common prosperity’. We think stocks are already priced for regulatory risk, and furthermore we don’t expect the impacts to be anywhere near as damaging as many prices suggest. The same is largely true for VIE risks where the Chinese authorities continued to implicitly endorse these structures. It is eminently possible that ADRs will be delisted in the next 2-3 years but all of our ADR holdings already have secondary Hong Kong listings, so we keep our focus on business fundamentals which are sound for the stocks we own. Regarding the economy, we do expect a moderate slowdown in economic growth but, at the same time, there remain many stimulus policy measures available to the Chinese government. Furthermore, in the short term China is unlike many economies in the world in that it is actually in a loosening not tightening monetary policy cycle. Over the medium term, we still expect China to sustainably grow faster than most EM economies, especially driven by consumption growth, which most of our investments are linked to.

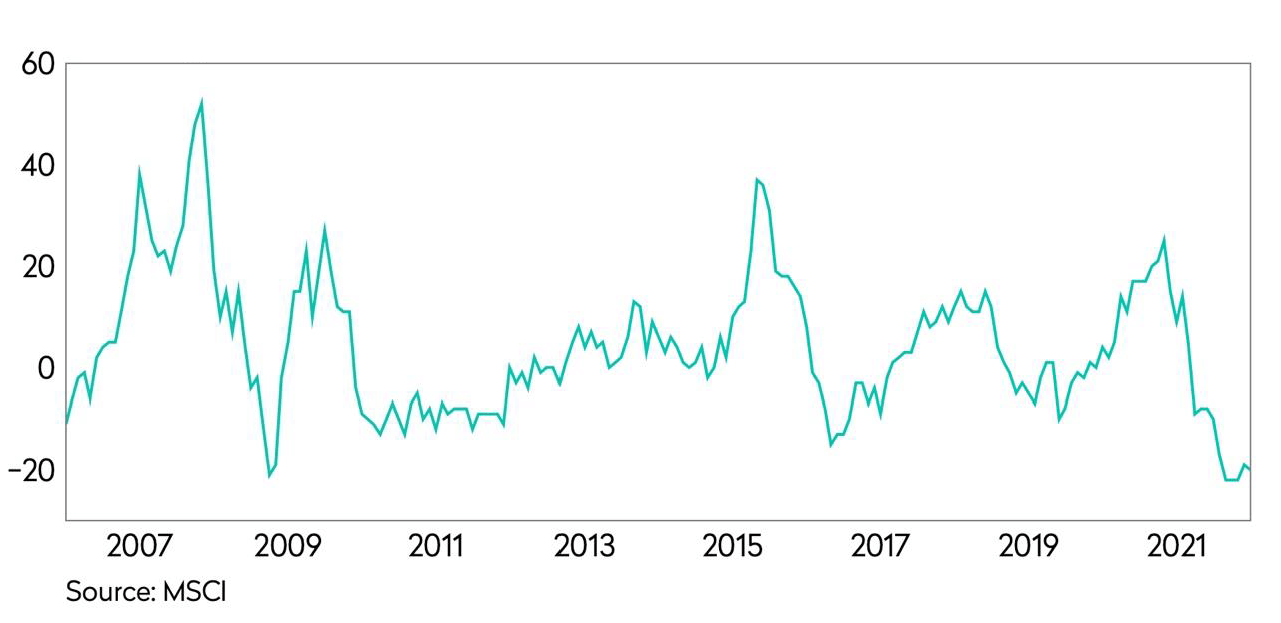

As can be seen in the chart below, China’s underperformance last year was the greatest on record vs EM. We think the likelihood of this reversing in some way during 2022 is reasonably high given the excessive pessimism implied by valuations.

Rolling 12-Month Relative Performance of MSCI China over MSCI EM

Upholding our disciplined valuation process, we move into 2022 confidently positioned. That confidence though rests on a recovery in China and our selected stocks in particular. We have added to extremely undervalued Chinese stocks and sit approximately 6% overweight the market. Within EMEA where we see less compelling valuations we are c.7% underweight. Additionally, we have reduced India to c.4% underweight post strong performance and the market trading on the highest PE in EM of 27x and index low dividend yield of 1%. Therefore, any combination of mean reversion from 2021, with regard for underlying fundamental valuations, and 2022 should produce better relative and absolute returns for the portfolio.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice. It should not be assumed that investments

made in the future will be profitable or will equal the performance of any security referenced in this paper.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without

notice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,”

“estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance

that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which

are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance that

the investment objectives of the strategy will be achieved.

This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission

of Mondrian Investment Partners Limited.

Mondrian Investment Partners Limited, Sixty London Wall, Floor 10 | London EC2M 5TQ | United Kingdom | +44 207 477 7000 • Philadelphia +1 215 825 4500 • www.mondrian.com

Registered office as above. Registered number 2533342 England. For your security and for training purposes, telephone conversations may be recorded.

Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority. Mondrian Investment Partners is a trademark of Mondrian Investment Partners Limited.