The emerging markets (EM) asset class experienced a challenging quarter as negative news flow seemed to follow its largest component, China. Overall EM fell 8.1%, but China fell 18.2% while EM ex-China only fell 2%.

The sell down in China begun in earnest as a slew of regulations hit the education, consumer tech and gaming sectors. This created a level of fear and uncertainty that hit some of China’s largest and best known companies such as Tencent, Alibaba, Meituan and New Oriental Education amongst others.

An already anxious investor base had further cause for concern when the country’s largest and most indebted developer Evergrande appeared to be teetering on technical default. This placed question marks over China’s economic health, despite reason to believe that the government will step in and manage issues of leverage and liquidity at troubled developers. Finally, a power shortage engulfed many parts of the country, which Goldman Sachs estimates will affect as much as 44% of the country’s industrial activity. They and other investment banks have consequently downgraded GDP growth estimates for the country.

Unsurprisingly, this confluence of negative events had a damaging impact on Chinese stocks, even causing some commentators to question the validity of investing in China at all. As investors in China and global emerging markets for over 25 years, Mondrian has witnessed and managed through countless disruptive events. We have learnt not to panic or overly generalise, but to analyse and evaluate each situation in a calm and balanced way using our tried and tested process. Emerging markets after all, has always been about pricing risk effectively. In almost all situations over those 25 years, when fear and uncertainty is heightened, opportunities arose to buy high quality businesses at uncharacteristically attractive prices. While the events of the last few months in China have of course caused us concern and necessitated a stress testing of our models, our long term analysis suggests once again that a clear opportunity to add to many positions in China has emerged.

Regulation

A shared goal behind recently implemented regulation is that of ‘common prosperity’. Common prosperity is a pillar of economic strategy that aims to establish a fairer Chinese economy, and hence Chinese authorities are addressing strategic obstacles impeding China’s advance toward common prosperity. This ideal essentially represents a greater focus on the social welfare of average households and requires public and private enterprises to share the responsibility for achieving greater social equality.

We believe it is important to distinguish between the regulatory changes for the education sector and those targeted at consumer tech companies. The seemingly harsh action against Education companies reflects the belief that their for profit business models were causing more social harm than good. The government felt the cost and pressure of education on children was burdening livelihoods and inhibiting population growth, as would be parents feared for the cost of raising children. This was the antithesis of common prosperity goals, and previously successful education companies have seen their stock prices fall c.90% this year – the inevitable consequence of being told to go not-for-profit.

In contrast, we believe that the regulatory actions taken against technology companies such as Alibaba, Tencent, Meituan and others are different in nature, as the social good these companies have created far outweighs the harm. Many of these companies had grown significantly, were arguably gaining too much power and behaving somewhat monopolistically in certain areas. The government has therefore engaged in various rounds of catch up regulations, ultimately aiming to promote fairer competition, as well as ensuring the best interests of lower paid workers, safeguarding the use of data, and protecting social harmony with the likes of gaming time limits for minors.

Somewhat contrary to the education companies however, many of the big tech companies have been at the heart of innovation in China, investing heavily in R&D and enabling China to meet GDP growth targets by creating millions of jobs and helping to transition China’s economy towards consumption. We don’t believe the intention is to destroy their profitability which is after all the incentive for further innovation, although the inevitable consequence will most likely be a slowdown in profit growth in the near term, and a need to invest for the common good. Furthermore, and most importantly, whereas for the education stocks it is fairly straightforward to ignore the sector as uninvestable, within consumer tech each company needs to be considered differently as the tighter regulatory environment will affect different companies in different ways, and in some cases, possibly hardly at all.

Finally regarding the issues surrounding Evergrande, we believe the importance of the real estate sector to the underlying economy is well understood by the Chinese government. As a result, we believe they will step in to stabilise the financial system when required, while not bailing out investors who should be accountable for taking speculative risks.

How to Navigate Chinese Stocks now

While we cannot argue these regulations are good for stocks in the short term, it is as much the abrupt and abrasive manner in which regulation has been implemented that has created the apprehension. The initiatives themselves are not fundamentally harmful if they enhance social welfare while concurrently protecting economic growth. It is the unpredictability that is the problem. We have witnessed elevated regulatory cycles before in China, and each time opportunities arise, hence the need to look stock by stock to assess where mispricing is most obvious from a lack of clear understanding on the potential impact from regulation. Additionally, it is important to reflect on the positives of investing in China, both standalone and relative to other emerging markets.

Despite the recent problems with Evergrande and power shortages, we expect China to continue to deliver above average GDP growth of approximately 5% per annum for the next few years with consumption growth above this. The private sector retains a critical role in ensuring that the Chinese economy continues to innovate and prosper, and that China reaches its goal of doubling GDP by 2035. The Chinese workforce continues to be skilled and educated, and one that has proven to be innovative and entrepreneurial. We think the outlook therefore continues to be bright for companies that can adapt to new regulatory frameworks and align with policy objectives. Therefore, we believe it should pay to be selective and take advantage of mispricing opportunities. Whilst further policy details or even new policies are likely to continue for the short term (which may weaken sentiment further), we believe that as long as they stay rational and within the wider stated framework then the long term opportunities for investments in China remain attractive despite the higher risk, given the sharp sell-off we have witnessed.

Value Opportunities

During challenging times for the portfolio as we have just experienced, we separate the noise and negative sentiment and trust in our long term valuation process. We find our range of outcome valuations particularly insightful, especially when even under various negative scenarios, we find our stocks trading at or below our worst case valuations as is the case with some Chinese names now. This is typically a strong signal and gives us the confidence to add.

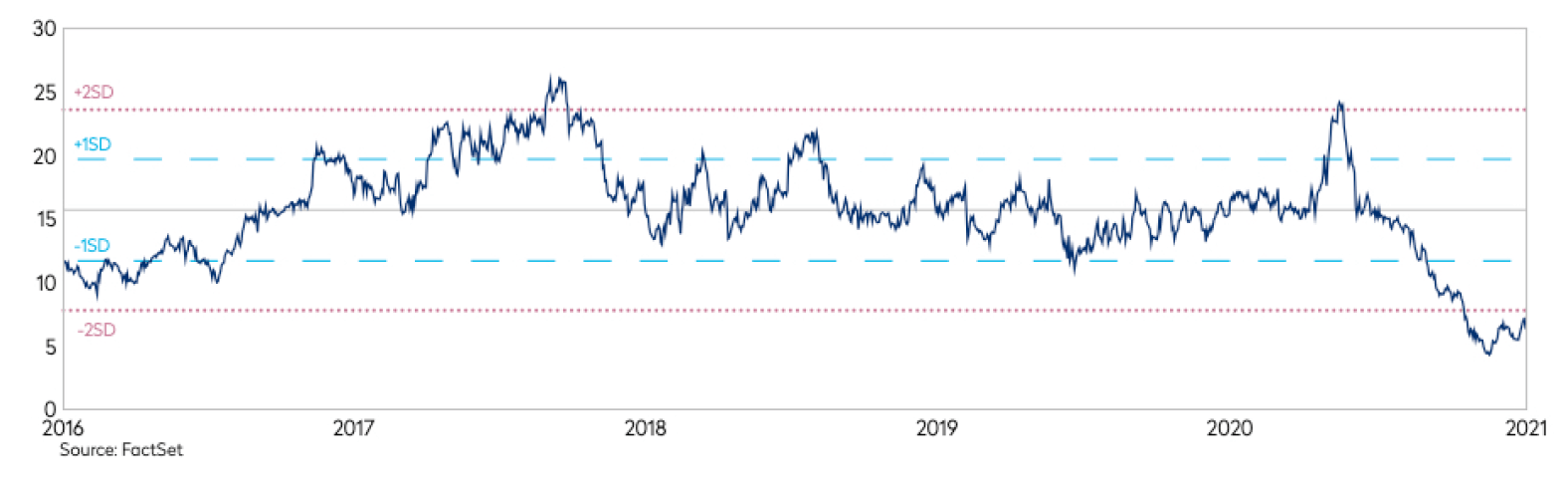

Autohome, China’s largest online car portal has been hit by a series of concerns, but in our opinion, while it has in part sold off amidst the wave of regulatory fears, we do not think it is impacted much at all by regulation. Autohome shares are heavily down, and now trade on net cash equivalent to approximately 50% of its market cap while continuing to generate free cash flow this year. While profits will fall this year given the global auto chip shortage, it is trading on all time low forward multiple levels (see below). The stock is also trading at close to our worst case valuation. We have added, believing there to be significant long term upside for patient investors. This is one example of many, but they don’t only sit in the consumer tech space. Across China stocks have been hit hard.

Autohome: 1-Year Fwd EV/EBITDA Multiple

(5 Year to September 30, 2021)

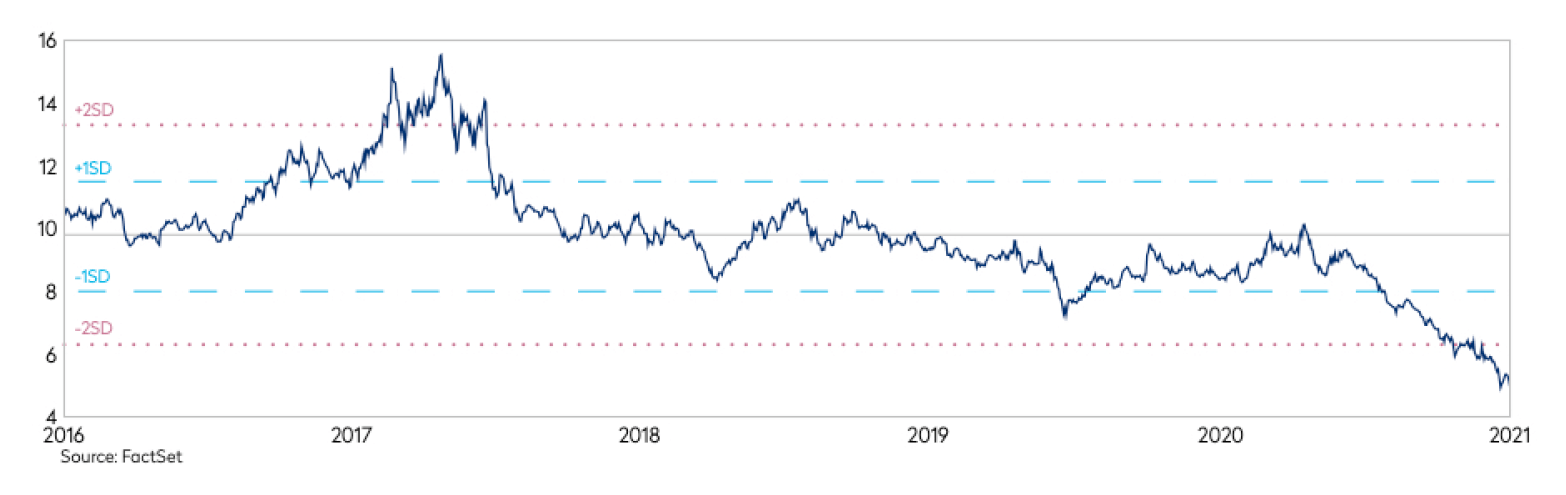

Ping An, one of the country’s largest life insurers was down 30% in the quarter, sold off on short term concerns for both the financial sector and regulation. In both cases, we don’t think the long term investment case or valuation has changed that much. As a result it also trades on abnormally low forward multiples (see chart below), and below our worst case valuation.

Ping An Insurance: 1-Year Fwd PE Multiple

(5 Year to September 30, 2021)

Gree Electric is another trading at levels where approximately 50% of its market cap is in cash while Baidu has approximately 40% in cash and investments. We have selectively added to our China holdings where we believe the potential risks are more than priced in.

Conclusion

Emerging markets is a risky asset class illustrated by periods of elevated volatility. This being so, pricing risk effectively is critical to being successful. Therefore, after a period of substantial absolute and relative weakness, we assess the price of Chinese assets today relative to the risk of investing there, but also how that compares to other emerging markets. In our opinion, many Chinese assets look very attractively valued on a long term risk-adjusted basis. As discussed above, we don’t think this is true for the education sector, while one needs to act with caution in other specific areas such as gaming, online entertainment content and fintech, but we can pick many specific stocks where the margin of safety or skew is strongly in our favour. We have therefore taken advantage of the sell off to top up many existing positions on the portfolio and rebalance from areas that have been more resilient, but still maintaining our market overweight position.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.