Definition of a Green Bond

A green bond is one whose proceeds are directed exclusively to financing projects that have a positive environmental impact. Bonds are typically governed by concerns regarding credit quality of the issuer, liquidity and duration, and green bonds are no different in this respect. Their emergence represents a notable development as a bond with the same characteristics can be assessed on its use of proceeds, also known as its “green-ness”, which is unrelated to the issuer’s credit quality.

However there is still no one widely accepted definition of what constitutes green. Whilst the International Capital Market Association (ICMA) Green Bond Principals have been widely adopted, they are relatively loose and as the market has developed there has been a proliferation of different standards, whether it is at the national level or criteria for green benchmark index inclusion. Efforts to harmonize green bond standards are underway, with a standardized definition key to development of the market.

To date, Europe has been the largest source of green bond issuers and investor demand, and the development of the EU Taxonomy and Green Bond Standard has been closely followed by market participants.

EU Taxonomy and Green Bond Standard

The proposed EU Green Bond Standard differs from ICMA’s Green Bond Principals by making a number of existing recommendations into requirements, such as use of proceeds in legal documentation, disclosure of proportion of proceeds used

for refinancing, impact monitoring and reporting, and undergoing and publishing an external review.

The key difference relates to eligibility criteria. Whilst the existing Green Bond Principals publish high level categories for green projects, the EU Green Bond Standard requires alignment with the EU Taxonomy, including four requirements;

- Substantial contribution to environmental objectives (as defined by the taxonomy)

- Do no significant harm to any of the EU Taxonomy’s environmental objectives

- Social safeguards – ensure compliance with minimum social safeguards as defined by the eight fundamental conventions identified in the International Labour Organisations declaration on Fundamental Rights and Principles at Work

- Technical screening criteria – including principles, metrics and related thresholds for particular sectors deemed environmentally sustainable

The EU Green Bond Standard is voluntary; however the current draft proposal specifies that issuers are encouraged to issue their bonds as “EU Green Bonds”. Whilst measures to encourage uptake of a common framework and definition are positive, there is a risk that if the standard requirements are too onerous, then they could potentially stifle market growth or create a two-tier green bond market. In our conversations with issuers and market participants, we have found that there are concerns regarding data availability to meet point 4 in particular, although specific screening metrics are yet to be defined.

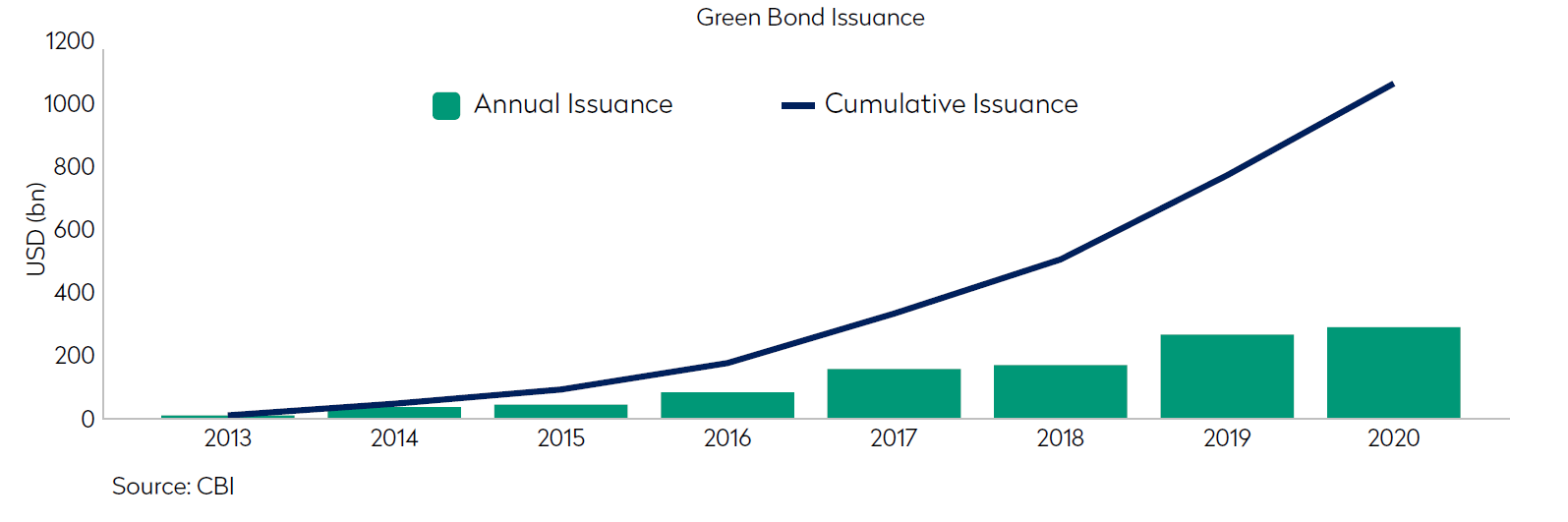

The Rise of the Green Bond Market

The green bond market continues to show sharp growth with 2020 a record year of issuance despite disruption during the market volatility in Q1/Q2 (chart below).

Following the issuance of the first green bond by the European Investment Bank (EIB) in 2007, green bond issuance remained limited and dominated by supranational issuers until 2014, when growth became broader based and began to accelerate. This coincided with the publication of the Green Bond Principals by ICMA.

There have been concerns raised that the supply of green bonds will not keep pace with demand and that policy measures are needed to spur investment in green assets and infrastructure to provide the green assets necessary for green bond market development. Mondrian believes that this concern is addressed by the factors listed below.

- There is already a substantial pool of green assets financed by non-green bonds. As the green bond market grows in size and common standards such as the EU Green Bond Standard remove uncertainty and reputational risks faced by issuers, this pool of assets is more likely to be opened up to green finance. The Climate Bond Initiative, an international organization promoting green finance, now estimates green bond issuance that meets their criteria has exceeded $1 trillion and significantly more if every bond that could in theory be labelled green was issued under a green label.

- In addition to this existing pool of green assets, it is widely acknowledged that current levels of investment are not sufficient to meet both domestic carbon reduction targets and those pledged by signatories of the Paris Climate Accord. The necessary additional investment will need financing, and whilst not all of it will come from the bond market, the nature of the assets and sectors that require investment: infrastructure, transport and energy, indicate a relatively high proportion of debt financing.

- Sovereign green bond issuance is growing and is generally seen as an important step in green bond market development.

- The Network for Greening the Financial System¹ was established in December 2017 as a forum for regulators and supervisors to find solutions to address climate-related financial risks. It has 36 members currently, including central bank representatives from Europe, the US, China, Australia, Singapore, Canada and the Bank for International Settlements (BIS). The network has three work-streams: supervision, macro-financial and mainstreaming green finance.

- Countries have been introducing targeted incentives for green bond issuers. For example, the Monetary Authority of Singapore has a green bond grant scheme² that will absorb the full cost of external reviews. The Ministry of Environment in Japan has introduced subsidies to help cover third party costs of green bond issuance such as external reviews, structuring and consulting³. The Hong Kong government is currently operating a pilot grant scheme that will subsidize the cost of getting green bond certification. The People’s Bank of China (PBoC) will include green bonds as eligible collateral for its medium-term lending facility, and green credit is now part of the banks’ Macro-Prudential Assessment (MPA): the higher the volume of green assets held (loans, bonds, etc.), the higher a bank’s MPA score.

The Case for Investing in Green Bonds

Green bonds offer a strong appeal to investors on a number of levels as the asset class rises out of its infancy. Clearly, green bonds are differentiated from other bonds due to the exclusive use of proceeds, but in almost every other sense their characteristics are remarkably similar and can be considered equally alongside one another. Importantly, green bonds hold the same payment rank to non-green bonds in the capital structure of the issuer and ultimately recourse to that issuer. They are not separated out or tied to the performance of the assets they are funding, so there is no distinction in overall risk. Returns have been exceptionally similar between green bonds and non-green bonds with similar characteristics, and there has been no clear historical performance sacrifice for investing in green bonds. However, the additional benefits of green bonds can be significant, as we outline below.

To Make a Positive Impact on the Environment

One of the key advantages of investing in green bonds is that they can provide a transparent conduit for positive impact investing. The proceeds of a green bond must be used exclusively for environmentally beneficial projects, contributing to objectives such as climate change mitigation, climate change adaptation, natural resource conservation, biodiversity conservation, and pollution prevention and control. Investors will have a clear view of how the proceeds of the bond are being used and what projects are being supported. The ability of issuers to deviate from this core principle and not invest the proceeds toward true environmental projects is also significantly restricted. Not only do issuers have to report on how the proceeds are being used but it is also common practice for independent third party companies to verify that the issuer is upholding this commitment. Finally, investment managers should be undertaking their own analysis to ensure that they are only investing in true green bonds. Mondrian employs a full assessment of any green bond it considers for investment and monitors the portfolio on an ongoing basis to this end.

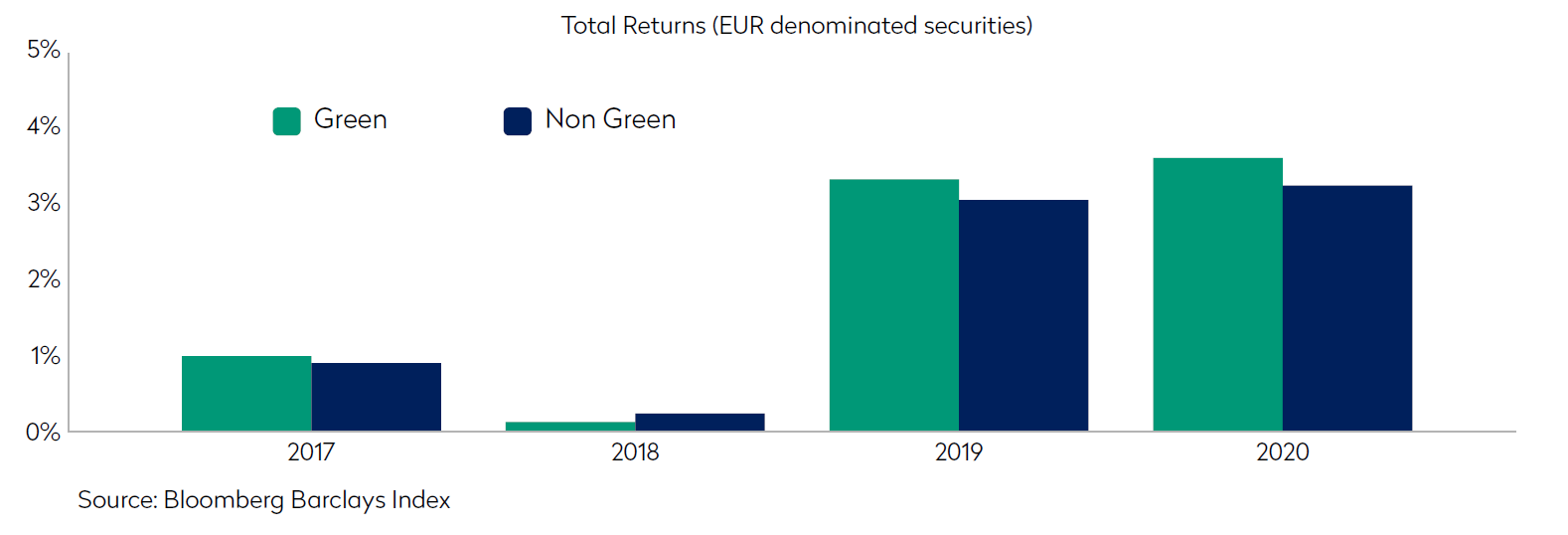

Without the Need for Lower Returns

Not only have green bonds historically offered similar return profiles to their non-green counterparts, but, if anything, they have slightly outperformed. Taking an analysis of total returns over the past three calendar years has shown that green bonds have more than kept pace with the total returns recorded by their like-for-like non-green counterparts (see chart below).

It is perhaps a common misconception that green bonds are priced at a premium to non-green bonds and the returns are therefore weaker, but clearly this has not been the case in recent history. Green bonds have historically offered very similar returns and volatility characteristics that investors have long targeted in allocating to bond markets, and there is no reason to believe that investors would be sacrificing any of the above with an investment in green bonds.

To Diversify

The green bond market has continued to show exceptional growth rates. As mentioned in the previous section, the growth rate of the green bond market is likely to be sustained by a number of underlying forces. There is a clear drive to be more ESG-aware and invest sustainably across markets and green bonds will be a key part of that. Whilst it is not specified that these investments need to be backed by bonds or green bonds, these instruments are likely to play a central role in supporting these significant funding needs. This has seen an increasing number of new issuers enter the market and that trend is certain to continue. Diversification is increasing in terms of issuer type, sector, credit quality and currency. As time goes on, the high-level characteristics of the green bond market should look more and more like the traditional global fixed income market that investors have become accustomed to.

To Better Engage with Issuers

Green bonds provide investors with transparency on the use of proceeds and a basis for engagement usually reserved for equity holders. In the current shift towards integration of Environmental, Social and Governance (ESG) factors into the investment process, this opportunity to engage is invaluable. Green bonds issuer reporting demands not only allow investors to have a distinct understanding of what exactly they are funding, but also provide a clear route for investors to target the projects they feel will yield the highest positive impact. In turn, this opens the door to engagement between issuers and investors as well as pushing issuers into supporting and funding the highest impact environmental projects. We have engaged with multiple issuers across sectors about climate-aware policies including both those with green bonds issuance and those without. It is clear to us that there is a broad and growing determination to support this asset class and both issuers and investors will have influence on its development going forward.

Active Management of Green Bonds – The Mondrian Approach

At Mondrian, we believe that a global green bond strategy lends itself ideally to active management, because there are several potential sources of alpha generation. From a top-down perspective there is country and currency allocation, while from the bottom-up there is credit allocation, duration positioning and opportunistic exposure to emerging markets debt, inflation-linked bonds and high yield bonds. These can all be exploited by an active approach to investing in global green bonds. Furthermore, the global green bond market is expanding very rapidly, therefore index compositions can potentially undergo significant changes over a relatively short amount of time. Attempting to replicate this by passive investment management could lead to excessive turnover and associated high trading costs.

The potential sources of alpha generation for running a global green bonds strategy are essentially the same as those for running a Global Aggregate Bond strategy, which we have been actively managing since 2003 and have a strong track record in. We believe this is repeatable for the following reasons:

- Mondrian is a financially robust, employee-owned firm fostering long-term continuity and stability

- We have a stable, well-resourced team with expert knowledge of the asset class

- We follow a disciplined process that has been shown to work over a long period

- We are not reliant on “star managers” with potentially unrepeatable calls

- We remain nimble with a manageable AUM and our focused team means that we can continue to rapidly exploit opportunities

Our heritage is as a global investor, and our Prospective Real Yield framework for country and currency allocation has been integral in the track records of all of our Global Fixed Income products, including both developed and emerging markets strategies. This is also a key part of our Global Green Bonds strategy. In essence, this framework relies on the selection of global bond markets that we believe best compensate for inflation and sovereign credit risks. It has three principal components:

- Inflation forecasting

- Sovereign credit assessment

- Real exchange rate analysis

Our Global Credit process takes a value approach that is quantitatively driven, extracting value across the credit cycle, by identifying the best value opportunities using our proprietary Relative Value Indicators. Our credit research is supported by a large team of equity analysts. A full credit assessment is performed on all of our Corporate issuers, and ESG considerations are integral to this assessment. Both our Sovereign and Corporate investment processes have been awarded 5 Stars in the most recent PRI assessment*.

.

“Green-washing” is a common concern among investors, and rightly so. This not only applies to the “green-ness” of a particular bond, but also to that of a portfolio as a whole. Many of our peers in the industry currently run green bond strategies which contain a significant percentage of non-green bonds. At Mondrian we do not believe in running a green bond strategy in this way. Not only do we strive for all of our bonds to be green, but also for all of our bonds to have a high degree of “green-ness”. We do this by applying MSCI’s Global Green Bond Index eligibility criteria as a first-level filter, supplemented by our own internal analysis as an additional assessment of “green-ness”. Furthermore, as part of our integration approach to ESG, we integrate a “green-ness” score into the issuer’s rating and therefore the valuation of our green bonds.

Green Bonds vs. Green Issuers

A question sometimes asked of green bonds is how should these securities issued out of traditionally non-green sectors be treated and there has perhaps been a tendency to bias away from these companies. Mondrian’s integrated approach to ESG is not to exclude companies operating in traditionally non-ESG-friendly sectors and instead incorporate these considerations into the overall analysis. We apply the exact same criteria in our green bond approach. By overweighting companies which are already “green”, then companies in carbon-intensive sectors can be deprived of the development capital that they urgently need to move to a greener business model. If an investor truly wants to make a positive impact on the environment then they should reward and deploy capital to those companies that are striving to reduce their carbon footprint rather than exclusively to those that already operate in green sectors.

¹ https://www.climatebonds.net/files/reports/cbi_sotm_2018_final_01k-web.pdf

² https://www.banque-france.fr/en/financial-stability/international-role/networkgreening-financial-system

³ https://www.mas.gov.sg/schemes-and-initiatives/sustainable-bond-grant-scheme

4 http://greenbondplatform.env.go.jp/en/support/subsidy.html

* 2023 PRI Assessment Scores: Policy, Governance & Strategy: 4 Stars; Direct-Listed equity-Active fundamental: 5 Stars; Direct-Fixed income–SSA: 5 Stars; Direct-Fixed income–Corporate: 5 Stars; Confidence Building Measures: 4 Stars. Please refer to www.unpri.org for the PRI assessment methodology. Mondrian’s full Assessment Report and Transparency Report may be requested via the PRI Data Portal. PRI = Principles for Responsible Investments.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.

This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission of Mondrian Investment Partners Limited.