Executive Summary

The recent UN Climate Change Conference (COP26) provides the world with a road map towards achieving the goal of carbon neutrality and limiting temperature rises to 1.5 degrees Celsius versus pre-industrial levels by 2050. The path to achieving these goals is complex, involving governments, corporates and investors. These ambitions pose profound implications for the investment landscape, creating opportunities and challenges with changes in risk appetite, inflation expectations, growth implications, access to capital and asset valuations. This paper highlights how Mondrian is well positioned to navigate the evolving investment environment in terms of pricing opportunities and risks. We showcase a few investments in Mondrian’s small cap portfolios, which bring to light how companies are exploiting opportunities and adapting their business operations in this evolving transition.

The Politics of Decarbonization is Complex

It has been seven years since the Paris UN Climate Agreement, and we observed for the first time during the COP26 meetings that there is a global consensus that climate mitigation efforts need to be accelerated. There has been a shift from targeting a warming limit of 2 degrees Celsius to a stricter target of 1.5 degrees Celsius1, as well as an increase in the number of countries pledging net-zero emissions plans. Our view is that despite the public commitments from many governments around the world, such an ambitious, but abstract and distant goal is unlikely to be achieved in a timely and straightforward manner.

Meeting the ambitious 2050 goal requires dynamic, global, coordinated commitments involving governments, corporates and investors. These commitments require mutual trust, followed by actions and supported by annual reviews on delivery versus targets.

We anticipate that the journey will be unsteady, and characterized by fits and starts, given the juggernaut-like agenda involving governments around the world employing different policies with different spending drives and funding requirements. The transition process is likely to involve i) regulatory tightening and enforcements including carbon levy/carbon border tariff adjustments on select sectors, ii) changes in taxation, in part to aid infrastructure spending to support decarbonization, as well as subsidies to minimize the impact of rising costs for some of the electorates, and iii) policies and incentives to target new areas for growth in a clean, green global economy.

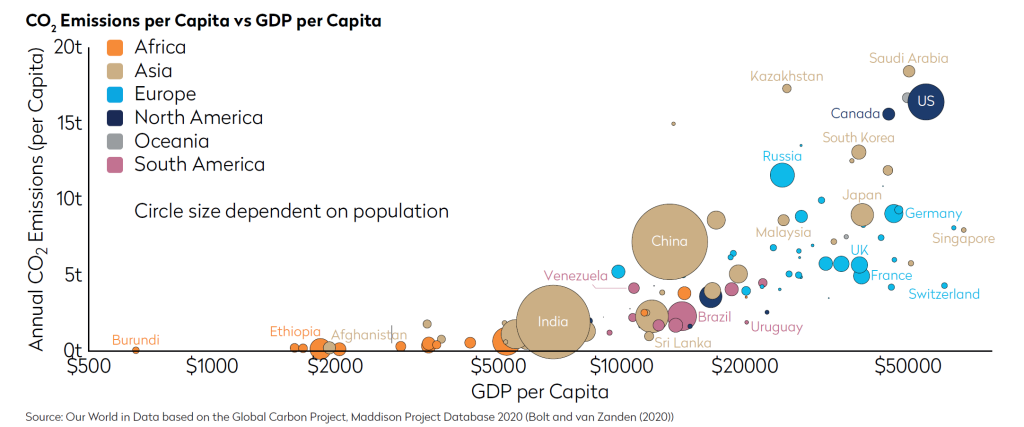

A paper written on this topic a decade ago most likely would have included a discussion of, “Are we contributing to climate change?” Whatever an individual’s view on global warming, governments have committed to a dramatic change in how our economies evolve. Further, accounting changes will give visibility into companies’ use of oil-based products and their greenhouse gas emissions. Chart 1 shows the scale of the challenge faced by some countries. Generally, higher income countries emit more carbon dioxide per person. However, for other countries, the challenge is to support the low-carbon transition whilst meeting their socio-economic obligations: how to move up the income scale without the use of fossil fuels? Coal and oil provided the means for many of the wealthier countries to industrialize over the last few centuries. Today’s emerging economies want to move to higher income levels, but to do so without fossil fuels will be difficult, expensive and may slow the pace of their domestic growth. Looking out into the future, the problem of slowing growth will likely be worsened with a shrinking workforce in many emerging economies (especially in Asia), whilst there are outstanding questions about their ability to offset this with productivity improvements. Given the scale of their populations and their relative importance to global economic growth, it is essential that the world seeks a commitment from the likes of India, China and Russia to assist in this transition – though leaders from China and Russia were notably absent during the recent COP26 conference. A consensus may be difficult to reach, as the emerging economies perceive it to be unfair when they are only just embarking on their socio-economic progress, to have this undertaking forced upon them with implications to their economic ambitions.

At COP26 financial commitments were made to developing nations to help them transition to stronger carbon-light economic growth. However, this comes at a time when the public finances in many countries – including both developed and emerging countries – have been constrained by the costs of dealing with COVID-19.

The transition path is likely to be uneven; if climate change actions are accelerated too quickly, it risks unintended consequences. For example, costly bottlenecks within global supply chains and land space constraints in some nations pose risks of higher inflation with implications to growth. Significant expenditure needs to be undertaken to meet the climate change agenda. As it is, thresholds for returns on investments across all asset classes are already artificially suppressed, due to accommodative monetary policy. This incorrect pricing of risk, coupled with a significant investment undertaking, is likely to fuel a further accumulation of tail risks. Furthermore, there is a likelihood of increased geopolitical risk, with a possible re-emergence of global trade tensions, as control of the supply chain for renewables (particularly solar) and key raw materials currently resides mainly with China.

On the other hand, if climate change mitigating actions fall short against commitments, there could be a bigger price to pay with accelerated actions at a future date. Such adverse effects could be two-fold. First, to make up lost ground in meeting targets and having run down the clock towards the 2050 deadline, governments may be forced to undertake more dramatic actions. Secondly, a poor performance on this issue may lead to governments buckling under greater pressure from environmental activists. Already, environmental activists have demonstrated a willingness to challenge governments to do more through civil disobedience campaigns. As time passes, so does a generation, and we note that the younger cohort have already shown a vociferous desire to implement climate change actions. Therefore, the momentum is unlikely to slow in the foreseeable future. Further, lobbying has become more sophisticated with calls for divestment from some companies, especially those with exposure to fossil fuels.

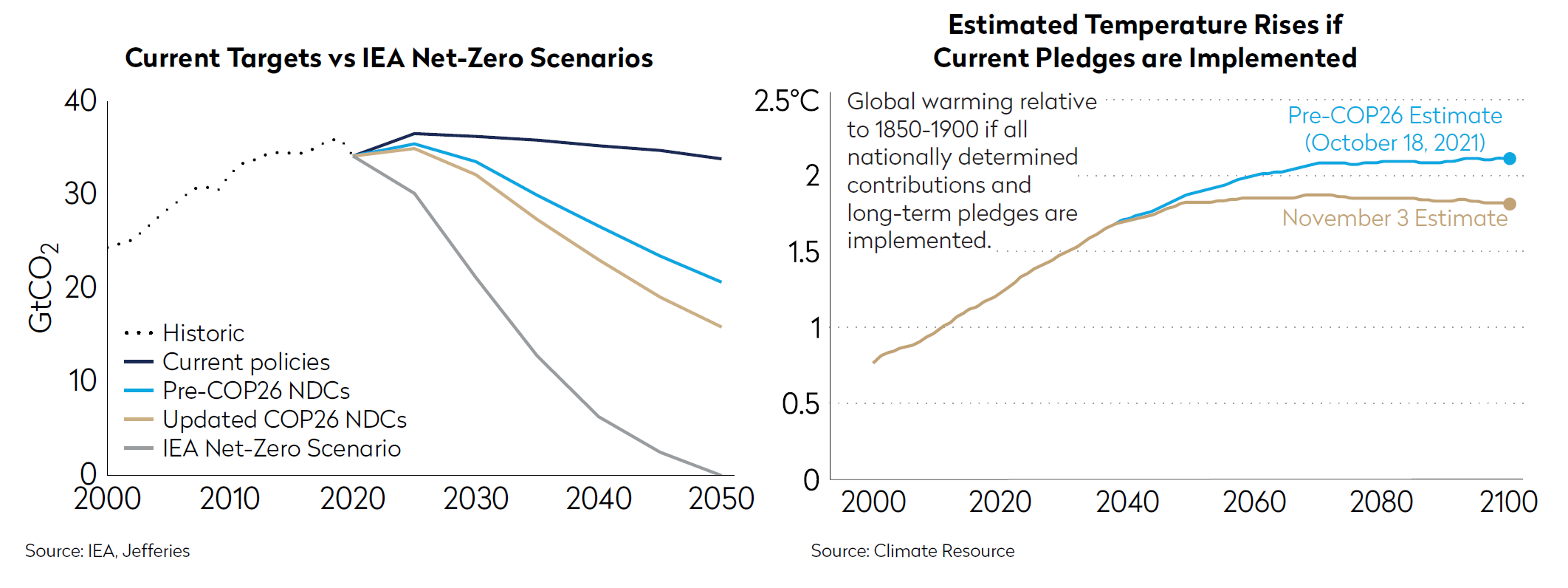

According to Climate Resource’s forecast climate models, if all countries meet their current long term emissions pledges, global warming would be reduced to c.1.8 degrees Celsius by 2100.

Positive Outcome with Standardized Regulatory Reporting

Currently, voluntary environmental and social disclosures can be vague and difficult to compare. The increase in standardized regulatory reporting on how companies account for their environmental and social impact will create a level playing field for disclosures, and remove confusion over targets with different frameworks and different metrics. We observe efforts by the IFRS Foundation’s launch of the International Sustainability Standards Board in bringing the rigor of mandatory financial reporting to current voluntary and vague environmental and social impact disclosures. Several stock exchanges – including London, Singapore, and Hong Kong – will be requiring climate disclosures in line with the Taskforce for Climate-related Financial Disclosures (TCFD) recommendations as part of listing obligations. Additionally, in June 2021 the G-7 backed the idea of compulsory TCFD reporting, with the US SEC signaling the proposal of mandatory climate disclosure by the end of 2021. The UK has gone a step further, requiring listed companies to report not only their climate risks but also their transition plans commencing from 2023. Mandatory disclosures lend themselves to transparency and accountability. Transparent and standardized disclosures force investors to rethink how to utilize the information and engage with companies.

Mondrian is Well Positioned to Navigate the Evolving Investment Landscape

The decarbonization journey – with its accompanying policies, regulations, subsidies, incentives, levies and disclosure requirements – poses both investment challenges and opportunities, with implications to risk appetite, access to capital and equity valuations. We believe Mondrian is well placed to adapt to the evolving investment environment in terms of pricing risks and opportunities. Mondrian utilizes a disciplined valuation framework to analyze companies based on their fundamentals, together with a long term investment horizon, and scenario analysis to understand the skew in returns of base against best and worst case outcomes.

Mondrian’s fundamental research analysis includes a process of company visits and rigorous engagement to understand management skills and ambitions, business plans, long term growth prospects and risks. This involves top-down, industry and environmental, social and governance (ESG) related considerations. Interaction with country, regulatory and sector experts is also integrated within our research process. We focus on financially material ESG factors to understand their impact on assets, liabilities, revenues and costs which affect a company’s sustainable cash flow generation and long-term valuation, as determined by Mondrian’s proprietary inflation-adjusted dividend discount methodology. Mondrian’s long-term fundamental focus and investment horizon provides an advantage to exploit mispricing created by short-term factors, as well as those created by material ESG factors which typically influence over the medium term. Analysis of material ESG factors has therefore always been incorporated in our investment approach. Mondrian has added to the process by licensing the Sustainability Accounting Standards Board’s (SASB) framework to help identify material ESG factors at the sector and stock level in a more structured manner.

Mondrian’s engagement process encompasses discussions on key material ESG factors and includes a focus on accountability which involves tracking a corporate’s progress in meeting its business plan targets, including ESG related ambitions such as short- and long-term emissions reduction targets. Should a company held in our portfolio consistently disappoint in its deliverables, with implications to its long term valuation, we will engage with its management and the board for both understanding as well as to steer change. We may ultimately divest the holding if the engagement and proxy voting efforts are not fruitful.

Navigating the Opportunities and Risks with Thematic Research and Stock Selection

The world is still heavily dependent on fossil fuels, which account for more than 80% of global energy consumption. Despite significant progress with decarbonization efforts, renewables (comprising wind, solar, hydropower and biofuel) only account for 10% of the global energy mix. A combination of wind and solar with a base load mix of hydroelectricity, biofuels and nuclear (which is observing renewed attention), should help reduce greenhouse gas emissions. We also observe significant research to develop cost effective storage solutions to overcome the intermittency of renewable energy (when the wind doesn’t blow and the sun doesn’t shine), and further efforts to find solutions that can strengthen and “smarten” the energy grid to cope with higher energy demands and decentralized sources of electricity (comprising of renewables, electric vehicles, storage and distributed electricity using roof-top solar panels in industrial buildings and homes). There is significant spend on research and development by both governments and the private sector to bring these technologies to scale and make them economically viable relative to existing legacy systems, but there will be a transition period before most countries have the infrastructure to meet their net-zero carbon pledges.

Mondrian’s small cap team has been proactive with its research in understanding attractively valued opportunities as well as challenges within the small cap opportunity set as the world embarks on its low carbon transition. Below, we provide some examples of investments made within the Mondrian small cap portfolios.

Renewables

Renewable Electricity Production

Renewable electricity production is a sector that will enjoy long-term structural growth as the world pursues its decarbonization transition. The Mondrian International Small Cap portfolio (ISC) has invested in a range of independent green energy producers since as early as 2016, targeting generation methods with competitive cost of energy focusing on geothermal, small hydropower and wind as they become competitive. Investments focused on producers such as Innergex Renewable Energy (Canada) and Boralex (Canada), with predictable cashflow generation backed by long-term contracts and long-duration fixed-rate debt, have both supported the upside performance of the ISC portfolio as well as providing downside protection during periods of market volatility.

Investments in the Electric Grid

With the rising trend towards electrification supported by green energy solutions, electrical transmission and distribution grids across the globe will have to undergo significant capital spending. Such investment will enable the grid to cope with intermittent and decentralized sources of electricity and enable two-way power flow across the grid between energy producers and end users, utilizing smart solutions and storage assets. The ISC portfolio has invested in this supply chain, including the engineering consultant AFRY (Sweden) with its exposure to energy, industrial engineering and infrastructure. AFRY is a beneficiary of industrial automation and energy efficiency upgrades, structural growth in renewables power generation investment, and infrastructure spending in fiscally strong Nordic regions.

Buildings

Buildings have also received focus as part of the net-zero transition plan. The International Energy Agency (IEA) net-zero scenario, which has become a blueprint for the global net-zero transition, targets all new buildings to be zero-carbon ready by 2030 and more than 85% of buildings to be sustainable by 2050. Arcadis (Netherlands) is another investment in an engineering consultant within the ISC portfolio. Arcadis is a beneficiary of the tightening in building regulations in developed economies towards energy efficient new builds and retrofits, as well as public infrastructure spending on the protection and restoration of natural capital such as water, land and air ecosystems, as observed in the Biden Infrastructure and Stimulus Plan as well as the EU Recovery Fund.

Household Goods

The Mondrian Emerging Markets Small Cap team has identified attractive opportunities in the smart appliances value chain through its investment in Shenzhen Topband (China), which is a leading global provider of smart controller solutions for high end home appliances and electric tools to allow internet of things (IoT) energy efficient features that support reduced energy consumption at the household level. The company also supplies customized lithium batteries with a focus on niche industries, such as e-scooters, caravans, furniture and home storage batteries.

Industrials

Companies are adapting their manufacturing process to reduce their greenhouse gas emissions. The ISC portfolio holds Verallia (France), a glassmaker which mainly makes glass bottles. The company is exposed to carbon pricing and it undertakes a forward hedging strategy to give better pricing visibility to its customers. Verallia’s packaging typically accounts for approximately 5% of the final product cost. This has enabled it to pass cost increases on to its customers. Despite this advantageous position, Verallia has made a commitment to reduce its emissions through a combination of i) increasing the use of recycled glass from 49% to at least 66%, ii) reducing the amount of glass required for each product, iii) reducing the carbon intensity of other raw materials, as well as a greater focus on reducing energy losses; and iv) moving to renewable energy sources. The ISC team has analyzed Verallia’s long term growth prospects including its plans to lower its emissions and improve cost efficiency. Our analysis incorporates carbon pricing risks, which enables us to understand the skew of returns of the base against best and worst case scenarios, to accommodate the evolving regulatory policies with respect to the pricing and coverage of carbon levies.

The Less Obvious Decarbonization Enablers – Denying Capital May Hamper the Decarbonization Transition:

There are also less obvious opportunities among companies and industries which may seem controversial as they are not clearly net-zero aligned at the outset. However, detailed fundamental long term analysis does reveal their potential as enablers to support the world in its low carbon transition.

As part of the transition, the developed markets plan to phase out – and the emerging economies plan to phase down – coal usage. Natural gas is a cleaner alternative to coal, and the ISC portfolio continues to hold Gaztransport & Technigaz (GTT, France), an engineering company with a leading global position in designing containment systems for the transport of LNG, including onshore and offshore storage. The company benefits from the transition, with the use of natural gas in thermal power plants as an interim solution prior to the end of fossil fuel energy production. There are further upside opportunities in growth for GTT: the company has a first mover advantage as its technical skills are applicable in the transport of liquid Navigating the Decarbonization Transition within Small Cap Equities December 2021 Page 5 of 6 hydrogen, if and when carbon-free green hydrogen becomes an economically viable solution both as a source of energy replacing coal and natural gas in thermal power plants and industrial processes, as well as storage in grid infrastructure and fuel cell vehicles.

Legacy thermal coal plants require some modification to accept alternative fuels, and existing gas distribution networks need upgrades to accommodate hydrogen. A company that benefits from spending on energy transformation and upgrades is Friedrich Vorwerk (Germany), an investment within the ISC portfolio. It is a leading provider of energy transportation and transformation across gas, electricity and hydrogen markets.

Boskalis Westminster (Netherlands) is another stalwart in the ISC portfolio. The company is the world’s largest independent dredging company. It derives recurring income from the maintenance of waterways, which will benefit from the near term cyclical recovery in global trade. Its expertise in maritime offshore services to the oil and gas sector has enabled it to extend its capability to support the offshore wind energy sector. There is further upside to growth if and when floating offshore wind installations become economically viable. The US Small Cap portfolio also made a similar investment in Great Lakes Dredge & Dock (US), the largest US dredging company that enjoys strong barriers to entry due to the Jones Act in the US. Great Lakes enjoys stable cashflow generation from the maintenance of ports, rivers and lakes including coastal restoration. There is further upside to growth with its participation in the offshore wind power generation sector.

The ISC portfolio recently invested in Wood Group (UK), an integrated engineering and consulting company. It has expertise across asset life cycles, ranging from initial feasibility and design, through construction, operation, maintenance and decommissioning as well as technical consulting solving complex challenges (including carbon capture and storage solutions, obsolescence management and environmental solutions to protect and restore natural capital). The company has its roots in upstream and downstream oil and gas, where it has developed strong technical skill, engineering know-how and rigorous health and safety standards. These competitive advantages have enabled the company to extend its specialization to renewables, in particular supporting the development and installation of offshore wind projects; it has had a role in 20% of global installed renewable wind capacity. We believe its technical skill, engineering know-how, and health and safety standards position the company well to support the development and installation of global offshore renewable wind projects. Furthermore, long-standing relationship with many oil majors makes Wood Group critical in assisting their decarbonization path. In our view, oil majors such as Exxon and Shell are decarbonization enablers, thanks to their focus on complex areas including offshore wind, hydrogen and solutions for carbon capture and storage, enabled by their deep technical resources within their ecosystem and backed by their strong balance sheets. Wood Group is also a beneficiary of decommissioning of coal plants and other fossil-fuel-related assets resulting from increased global efforts towards decarbonization. The company has a strong reputation in environmental and remediation work and is a beneficiary of US Infrastructure spending as well as the EU Recovery Fund. Moreover, we believe Wood Group is likely to benefit from near term capital expenditure plans by low-cost Middle Eastern fuel producers, given their low spare capacity and the need to support near term global growth.

Wood Group is an example of a company within the oil and gas value chain with deep technical skills, engineering know-how and relationships within the ecosystem which position it well as an enabler, supporting the world in its decarbonization transition. Denying capital to such companies which are not net-zero aligned at the outset may hinder the world in achieving its climate goals.

Conclusion

The Glasgow Climate Pact (COP26) reached an unprecedented agreement with 195 countries towards achieving carbon neutrality and limiting temperature rises to 1.5 degrees Celsius versus pre-industrial levels by 2050. The decarbonization path is highly complex and requires a global coordinated commitment with mutual trust and actions involving governments, corporates and investors. The path is likely to be uneven as it involves many governments employing different policies with different spending drives and funding demands to support this transition process. On the one hand, a rapid acceleration of decarbonization actions may derail the path to net-zero, as it risks unintended consequences including political instability, costly supply chain bottlenecks leading to higher inflation expectations, growth implications, geopolitical uncertainty and a possible re-emergence of global trade tensions. On the other hand, if actions fall short against pledges, governments may come under pressure to undertake further accelerated actions which may contribute to political, regulatory and economic uncertainty in the future.

The decarbonization journey poses both investment opportunities as well as challenges with implications to risk appetite, access to capital and asset valuations. The move towards decarbonization seems to be most advanced in parts of Europe (for example, carbon levies, carbon border tariff adjustments and green hydrogen investment targets). With COP26 held in Britain, this country is at the heart of the debate, giving Mondrian an advantageous viewpoint on the issue. Whatever an individual’s view on climate change may be, this global consensus changes the investment landscape for the next decade and beyond. Mondrian is focused on positioning its portfolios to benefit from this low carbon transition. We believe our disciplined valuation framework, which analyzes companies based on their long term fundamentals incorporating scenario analysis, enables us to adapt to the evolving low carbon economic environment.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

Examples of securities will represent only a small part of the overall portfolio and are used to illustrate our investment style. Such examples are not intended to represent a recommendation to buy or sell, neither is it implied that they will prove profitable in the future. Holdings are subject to change and may not feature in any future portfolio.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without notice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

This document is an internal research paper. The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance that the investment objectives of the strategy will be achieved.

Mondrian Investment Partners Limited licenses and applies the SASB Materiality Map® Disclosure Topics in our work. This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission of Mondrian Investment Partners Limited.

Mondrian Investment Partners Limited | Sixty London Wall, Floor 10 | London EC2M 5TQ | United Kingdom | +44 207 477 7000 | Philadelphia +1 215 825 4500 | www.mondrian.com

Registered office as above. Registered number 2533342 England. For your security and for training purposes, telephone conversations may be recorded. Mondrian Investment Partners Limited is authorised and regulated by the Financial Conduct Authority. Mondrian Investment Partners is a trademark of Mondrian Investment Partners Limited.