Mondrian takes a differentiated approach to currency valuation using a long-term Purchasing Power Parity method. Our PPP method provides a consistent measure of value across all currencies – a process we have employed since the founding of our firm in 1990.

Movements in the Japanese yen (JPY) can create significant investment opportunities. Below is a concise overview of the currency shift and recent developments in Japan.

Key Drivers of Japanese Currency Movement and Market Impact

Over the past month, the Japanese yen has appreciated by approximately 10%, driven primarily by the Bank of Japan’s recent rate hike on July 31st and Governor Ueda’s accompanying commentary. This, combined with weaker US labor market data and narrowing interest rate differentials, has amplified currency movements.

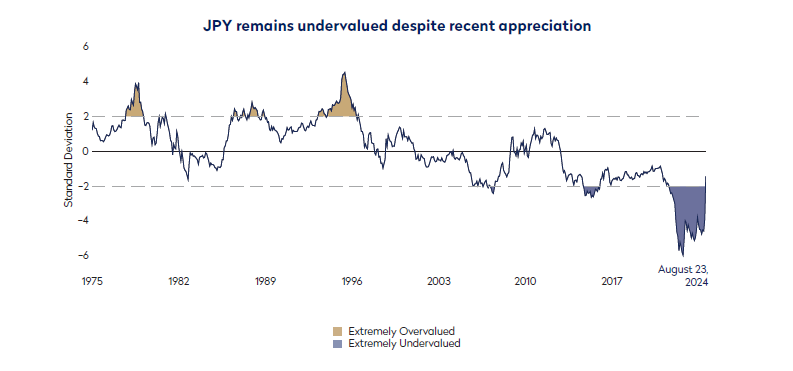

To read the chart above, the grey bar in the middle is Mondrian’s estimate of fair value against the US dollar, the dotted lines represent two standard deviations compared to fair value (which we deem as statistically significant), and the dark line represents the movement of the underlying currency.

Investment Implications

Despite the recent appreciation, it’s essential to recognize that the yen remains extremely undervalued according to our Purchasing Power Parity (PPP) valuations. Historically, the Japanese equity market has shown sensitivity to global trade and economic cycles, and while increased fears of a US and global recession have contributed to a recent market correction, we see a silver lining.

Many Japanese companies are well-positioned to withstand downturns, boasting strong net cash balance sheets and solid earnings. The cyclical nature of earnings notwithstanding, Japanese corporates are in good health, evidenced by solid earnings and record shareholder returns.

Opportunities for Active Management

We believe that heightened market volatility presents opportunities for active managers. Our focus remains on the skew of outcomes, underlying fundamentals, and valuations. The longer-term positives of improving corporate governance, capital allocation, and overcapitalized balance sheets in Japan continue to bolster our confidence in the market.

Looking back to 2023, our PPP currency analysis indicated significant undervaluation of the yen, so its recent appreciation aligns with our long-term projections.

Disclosures

Past performance is not indicative of future results.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. Views should not be considered a recommendation to buy, or hold or sell any security and should not be relied on as research or investment advice.

This introductory material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials.

The opinions expressed here are Mondrian’s views based on proprietary research. Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority (Firm Reference Number: 149507). Mondrian Investment Partners Limited is also registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).