The notion that the desirability of a common stock was entirely independent of its price seems incredibly absurd. Yet the new-era theory led directly to this thesis.… An alluring corollary of this principle was that making money in the stock market was now the easiest thing in the world. It was only necessary to buy “good” stocks, regardless of price, and then to let nature take her upward course. The results of such a doctrine could not fail to be tragic.

–Benjamin Graham & David L. Dodd, Security Analysis, 1934

Growth Stocks’ Returns Continue to be Supported by Investors Accepting Lower Discount Rates

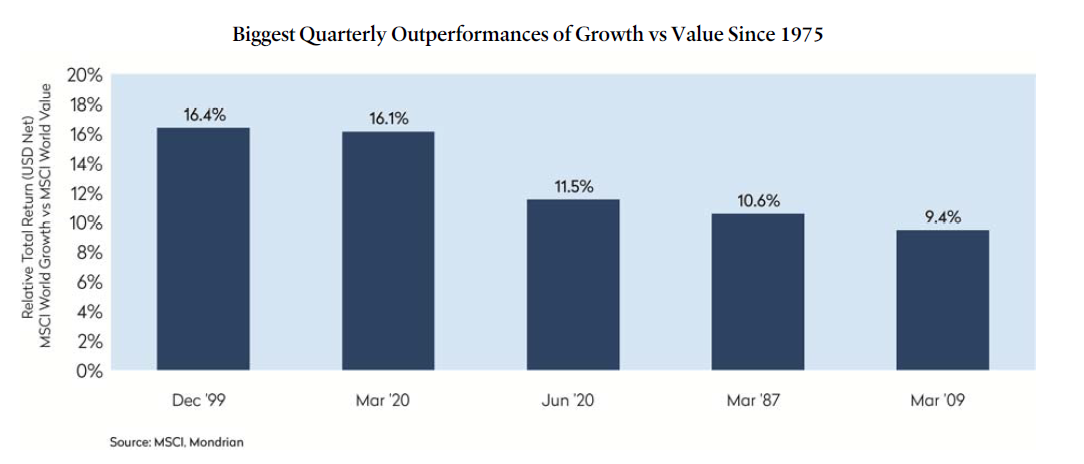

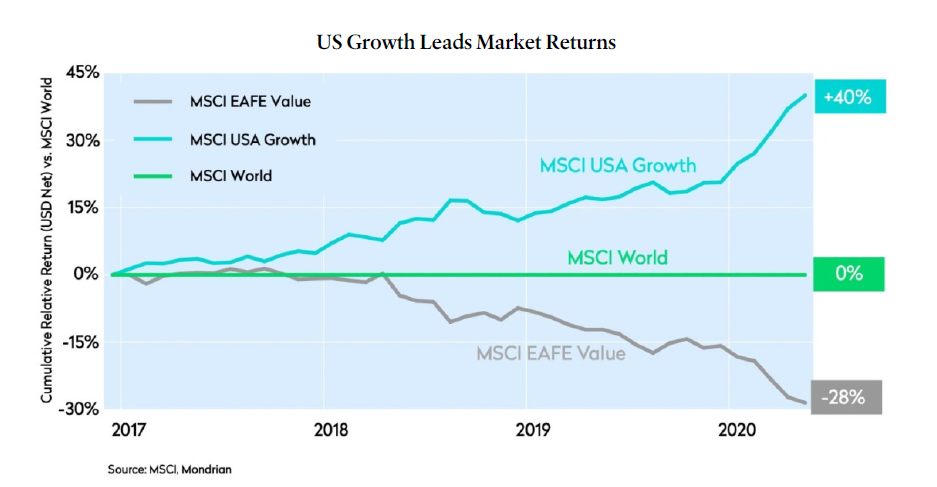

Growth-oriented investments in equity markets have significantly outperformed value since the financial crisis. As we have written previously, we believe that this can be understood in a DCF or DDM framework as exceptionally loose monetary policy suppressing investors’ discount rates. If discount rates are dragged lower, investors much more willingly trade off cash flows today against cash flows far into the future. At the same time, technology and other forces have caused significant structural changes in our economy and in certain cases, disrupted businesses, many of which are in the value sub-index: the rise of e-commerce penetration in retail, the disruption from electric vehicle penetration in autos, and ESG concerns reducing oil demand over the long term. The confluence of these factors has caused significant divergence between value and growth subsectors in the past decade, much more than what the fundamentals warrant in most cases in our view. This has become extreme since the COVID-19 crisis hit Europe and the USA in the second quarter of this year. As the chart illustrates, the first two quarters of 2020 were the second and third best ever quarters globally for the growth sub-index against value, and compounded, the MSCI World Growth sub-index has now outperformed value by almost 30% in the first half of 2020.

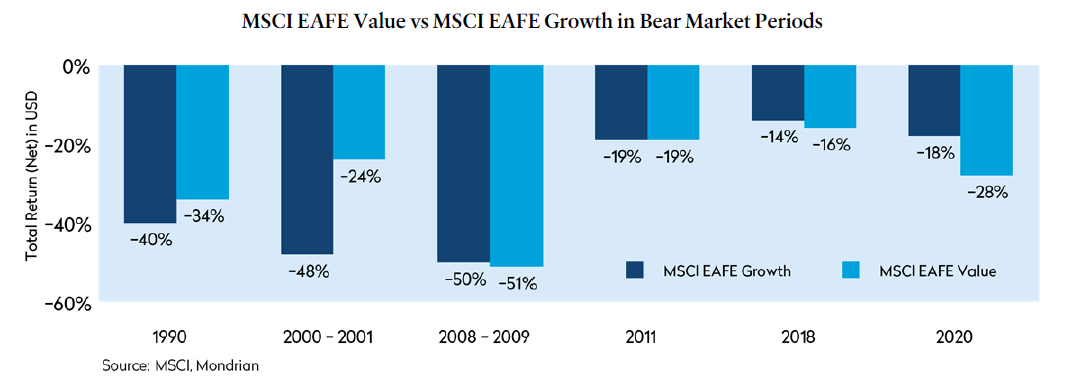

Value Stocks Have Not Offered Protection in Challenging Markets

As a defensive manager, this has presented a specific challenge for Mondrian. Historically, value has not

lagged growth by such a significant margin in a bear market since the MSCI index series were created as the

data below for MSCI EAFE illustrates.

While “value” to Mondrian is not a simple valuation screen; a dividend discount model is a forward-looking model that considers both today’s valuation and tomorrow’s growth outlook. Our analytical work earlier this year was increasingly indicating that the price for future growth was already too high, whereas the price for current earnings capacity was possibly too low. This meant that our portfolios, and the stocks we felt were mis-valued, were increasingly focused on investments in cyclical sectors, and the stocks in the portfolio were disproportionately drawn from the value sub-index.

Reactions to COVID-19 Exacerbating Discount Rate Distortion

In the immediate response to the crisis, investors, struggling with uncertainty, have returned to the playbook that has worked well over the post-financial-crisis period: uncertain economic outlook, central banks intervene, interest rates fall, volatility declines, all causing investors to feel justified in lowering their discount rates and buying future growth. With recent history to support them, the more uncertain the immediate economic outlook, the more comfortable investors feel buying future growth.

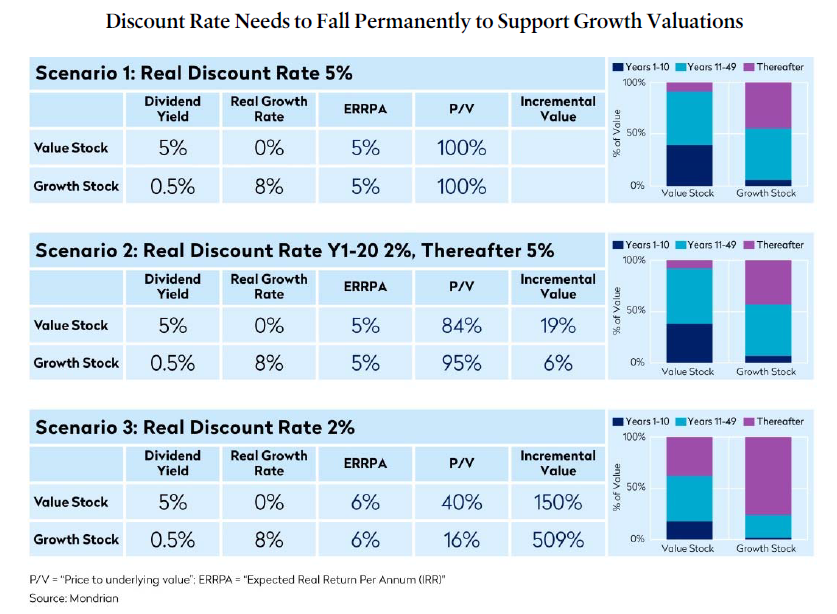

To explain the differential impact of changing discount rates on stocks with typical value and growth characteristics, we highlight below three scenarios that illustrate the differing return profiles created from changing discount rates. Assuming perfect foresight and no change to the starting share price, Scenario 1 uses Mondrian’s consistent 5% real discount rate, whereas Scenario 3 uses a lower long-term 2% real discount rate. Scenario 2 is an amalgamation that assumes a 2% real discount rate for twenty years and then reverts to a 5% real discount rate thereafter.

A bear market quarter is defined as one in which the benchmark (MSCI EAFE) showed a negative return.

Using Scenario 1 as the base, Scenario 3 shows that simply lowering the discount rate can potentially be very supportive of growth stocks, as the “incremental value” increases geometrically with long-term lower discount rates. However, while mathematically true, the investment challenges from this analysis are: i) the ERRPA or IRR does not change materially (both stocks remain similarly attractive based on anticipated cash flows) and ii) as demonstrated by the graph, the value “created” is mostly back-end loaded, capitalized terminal value that can easily disappear if investors discount rates change again or the growth proves ephemeral.

Scenario 2 illustrates the other problem: the lower discount rate needs to last forever, a formidable assumption even in today’s world, to incrementally benefit the return to growth stocks. The capitalization of earnings many years into the future implicit in the terminal value for growth stocks means any hint of a higher discount rate quickly skews relative returns to benefit the value profile.

Long-Term Equity Discount Rates More Complex than just Interest Rates

In today’s economic context, it is easy to see why growth is intuitively attractive. With COVID-19 uncertainty forcing companies to withdraw immediate earnings forecasts, earnings five, ten and even twenty years into the future look, for many growth companies, more assured and easier to model than earnings a year from now.

This is an optical illusion, or perhaps a mathematical illusion. Does anyone remember the Blackberry, never mind the Palm Pilot? In fact, actual discount rates are much more complex. In addition to long-term real interest rates, they incorporate an equity risk premium which needs to take into account any additional future expectations on inflation, investors’ return expectations and risk tolerance, and time value and utility of money.

While a decrease in interest rates in isolation could result in lower discount rates, changes in other variables should very likely offset the impact of low rates. Over time (as measured ex-post), the market risk premium can fluctuate significantly on a long-term horizon, and in fact it is perfectly reasonable, for example, to assume it should now be higher in a more challenging and uncertain macroeconomic and geopolitical environment. With investors focusing on the monetary policy component of discount rates, they leave themselves very exposed to a change in one of the other components.

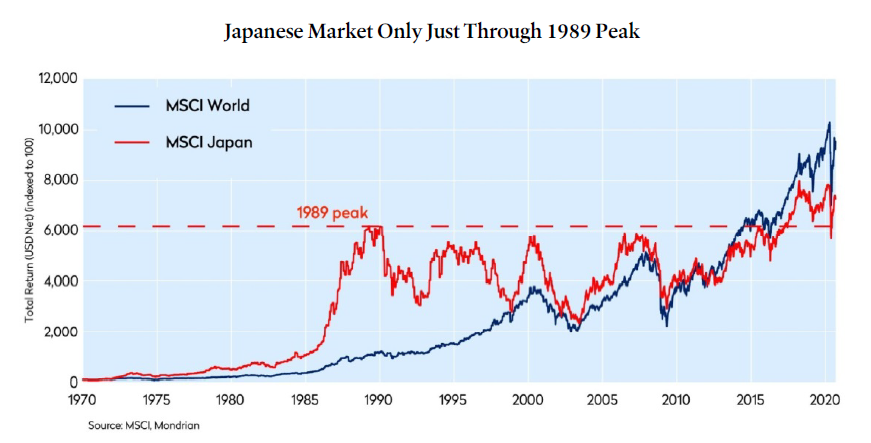

Assuming Low Discount Rates Capitalizes Future Returns: Japan in the 1980s

In using a lower discount rate to justify current valuations, investors are implicitly accepting lower future expected returns while still assuming equity-type risk. In Japan circa 1990 (before the collapse of the bubble), many investors argued that with interest rates at consistently low levels compared to other developed markets, and inflation apparently dormant, the high growth in the Japanese economy (which sounds like an oxymoron today) could support stratospheric valuations. With Japan set to overtake the US as the world’s largest economy, investors felt justified in using lower discount rates for Japanese assets compared to other markets. With hindsight, as the chart below shows, they had just capitalized the next 30 years of returns.

Even though interest rates continued to fall for much of the subsequent period, returns didn’t exceed their 1989 peak until 2017. As we argued at the time, investors focused on future returns were able to find much better investment opportunities on offer elsewhere.

Future Growth is Inherently Uncertain: Discount Rates Need to Capture this Risk

The Japan example also illustrates that future growth is inherently uncertain. In 1990, Japan was increasingly leading in industries such as autos, semiconductor manufacturing, and consumer electronics, all industries of the future and areas that the US had previously dominated. The yen was strong, driven higher by international central bank collaboration. The land around the Imperial Palace in Tokyo was worth more than all of California, and books such as Ezra Vogel’s Japan as Number 1 were flying off the book shelves (pre-Amazon days). These heady growth forecasts already capitalized in the valuation models never materialized. It turned out that much of the expected growth was fueled by unsupportable leverage, undervalued exchange rates and over-optimistic forecasts.

Lower discount rates capitalize future growth. But growth forecasts twenty, thirty, fifty years into the future are inherently uncertain and have a wide range of possible outcomes. Political change, pandemics, Brexit, trade disputes, government instability, regulation, (hyper) inflation, investment, exchange rates and things we haven’t even thought of can dramatically alter outcomes and the probability of achieving a return. A dollar earned today is not the same as a dollar earned twenty years from now. At its most simple, the utility of that future dollar is substantially lower. The role of the discount rate is to capture these risks.

Long-Term Sustainable Discount Rate Best Approach to Optimize Future Returns

The challenge for investors is that lower discount rates today will capitalize future returns, but they do not necessarily lower future liabilities. Investors need to be aware of that when they build portfolios. At Mondrian, we use a consistent 5% real discount rate in our dividend discount models. This discount rate is both the rate at which we discount future cash flows to account for many of the risks that we have discussed above, but it is also the minimum expected return hurdle rate for investments within our portfolio. We believe that this discount rate captures the interacting underlying discount rate components: the cyclicality of real interest rates, the passage of time, the variations in long-term equity risk premia, and changing inflation rates. We set our discount rate, or minimum level of expected equity return, to reflect the very long-term historical returns achieved from equity markets over many decades: time periods which have included high and low interest rates, differing levels of inflation, differing levels of economic growth, numerous wars and other conflicts as well as a wide range of political and tax regimes.

We capture the inherent uncertainty of future outcomes for different assets through detailed scenario analysis, developing worst case and best case scenarios – in addition to a base case valuation – for each individual holding. Taking into account our scenario analysis and the math outlined above (especially the ERRPA), we do not believe that our portfolio would change meaningfully if we adopted a lower discount rate. Ultimately we have to build our portfolios looking forward for the best future returns. Investors who adopt a lower discount rate to justify many of today’s valuations are fundamentally accepting lower long-term returns.

Bifurcation of Valuations Increasingly Stretched by Differing Discount Rates

Higher returns today are created by investors willing to pay higher multiples on profits earned well out into the future. How long is that future? When will investors say, “Is Apple the next Blackberry?”, “Should Amazon be split up?” or “What about the Nissan electric car?” At Mondrian, we debate these issues every day as we build our valuation models, and we know that the range of outcomes to answer these questions can be very wide. We believe that the market today is valuing many stocks for a certainty of growth and others for certain disruption: applying the best case and a low discount rate for one subset of stocks and the worst case for another.

We ran this chart in our outlook at the beginning of the year. Since then, the return gap between EAFE Value and US Growth has continued to widen. Our analysis indicates that despite the challenging economic outlook brought on by COVID-19, the return difference over this period is broadly explained by multiple expansion for growth and contraction for value. Moreover, we don’t dispute that looking forward we would most likely expect faster growth from stocks in the growth sub-index. The problem is that given current pricing multiples, future returns are highly dependent on the realization of that growth. You can see this on an individual stock level.

Unsustainably-Wide Relative Valuation Opportunities Opening at the Stock Level

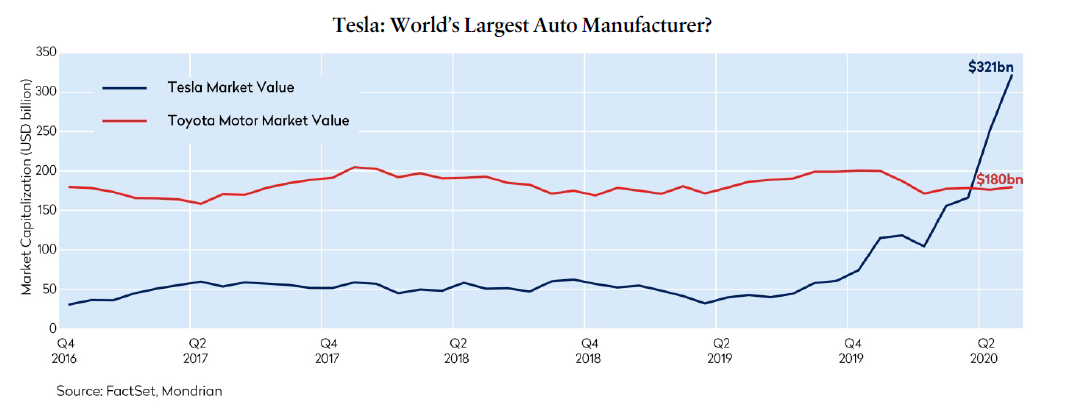

Much has been written about the market capitalization of Tesla surpassing Volkswagen and now more recently overtaking Toyota Motor to take the mantle of largest auto company in the world (see chart below).

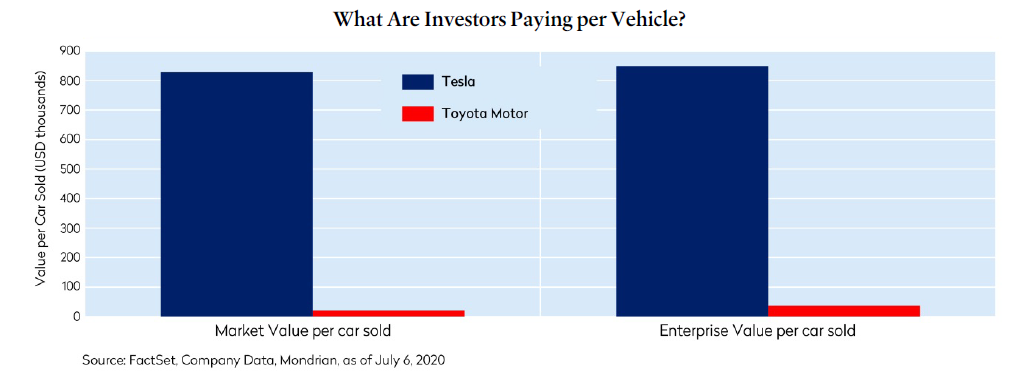

We struggle with this conclusion, even while agreeing that Tesla is an innovative auto company. Toyota currently sells almost 9 million vehicles worldwide, Tesla approximately 400,000. Toyota makes, even in this difficult operating environment, a profit on each vehicle sold. Tesla hovers around breakeven today. Toyota has significant experience (decades) in hybrid electric vehicles. Despite that substantial customer base, profitability and relevant EV technical knowledge, investors only pay about $20,000 per vehicle sold when purchasing Toyota. Tesla would cost them many times that, even when you take the most negative possible incorporation of Toyota’s leasing business and balance sheet debt into the enterprise value calculation (seechart below).

Given the high upfront price of Tesla’s stock today and the still nascent profitability (ten years after listing), the return from Tesla is very back-end loaded and highly dependent on achieving substantial forecast future profitability levels over twenty plus years from now.

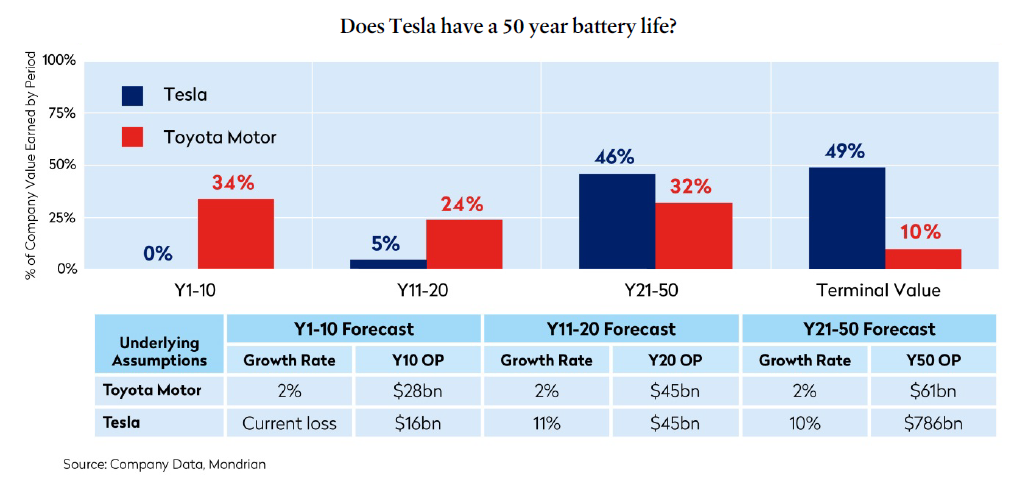

To challenge our conclusions, we built comparison Mondrian standard DDM models for Toyota and Tesla that analyze the underlying assumptions necessary for each stock to offer investors a long-term 5% real return. The assumptions and outcomes are summarized below. While each of these numbers is subject to debate, the underlying mathematical conclusion is robust: Toyota should be able to return to investors, through profit and cash flow generated from operations, about one-third of its expected return in the next 10 years and over 50% in 20 years, despite relatively little assumed growth.

Tesla, given costs and its growth investment still required, will only begin to achieve small excess returns twenty years from now. Moreover, given the high share price today, Tesla will need to earn 13 times what a stable Toyota does 50 years from now to offer the same long-term return to investors. That might not sound like a lot until you think about how many vehicles will have to be sold, the investment required to build the facilities to manufacture the vehicles, and the price and profit margin per vehicle required to reach that target.

Even if Rates Stay Low, Skew of Returns Favors Value-Oriented Portfolios

We build forward-looking DDM models all the time. We love great companies and we are as excited as anyone else about new products, but our experience has taught us that, as in Japan in 1990, paying high multiples, more likely than not, will mean future returns are already capitalized and today’s investor is just paying for someone else to exit. An alternative outcome requires even higher growth even further out into the future. The further out the forecast is made, the more uncertain it becomes. This creates significant risk for the investor given the back-end loaded nature of growth returns. Contrary to current perceived wisdom, high price multiple stocks are risky and their prices should be extremely sensitive to any future rise in discount rates, whether that is driven by interest rates or other perceptions of risk.

As the Tesla analysis illustrates, increasingly, the assumptions and prices that markets are expecting investors to accept for some stocks require a significant level of confidence that very high growth well out into the future can be achieved despite discount rates staying low forever. We build portfolios looking forward to achieve future returns. While Tesla is not the market (yet), in an environment where investors have already capitalized the future returns for some stocks, we believe it is reasonable to assume that the best returns will come from companies, such as today’s value stocks, where investors have applied low expectations and higher discount rates. This fundamental valuation logic has always been at the heart of Mondrian’s investment approach. We acknowledge that it has been a challenging few years on a relative basis for Mondrian’s portfolios, but this basic math says to us that even if interest rates stay where they are, the long-term skew of outcomes should now strongly favor a value portfolio.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice.

Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed.

It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.