Mondrian’s 3rd Quarter 2019 International Equity Fund’s Investment Outlook , A More Favorable Perspective for International Equities was recently featured in Advisor Perspectives.

Strong market returns in 2019 despite geopolitical overhang

World equity markets have produced strong returns year-to-date, driven by declining interest rates and rising growth stocks. Despite double-digit gains for the MSCI World index, geopolitical gloom, notably trade wars and Brexit, hangs over investors, economies and the share prices of more economically-sensitive companies.

To many observers, the news flow around Brexit seemed to worsen in the third quarter. Boris Johnson took over as prime minister in July and adopted a far more adversarial tone in comparison to his predecessor, pledging to leave the European Union (EU) with or without an agreement on October 31st “do or die.” While his rhetoric is targeted at suffocating a challenge from the recently-formed Brexit Party, parliament, suspicious of the prime minister’s tone and presumably fearful that he might not be bluffing, has imposed itself on proceedings by passing a law compelling the government to seek an extension from the EU on October 19th unless a withdrawal deal has been passed. Although cynics will question whether the government has somehow a means to circumvent this new law, it seems far more likely that the no deal tail risk has, at the very least, been pushed out to 2020. Moreover, although a deal still seems highly improbable given the time constraints and the political constraints, the only path towards honoring the “do or die” pledge would be a negotiated departure.

Practically, a deal would only partially address the Brexit issues, since the wrangling would just start again with more detailed arguments over the structure of the UK’s future relationship with the EU. In the absence of a deal, an extension followed by a general election later in the year or in the first half of next year is most likely. We acknowledge that the Brexit uncertainty and the tail risk of a disorderly Brexit, even if it remains unlikely, will continue to weigh on the UK economy and on the performance of UK stocks. In the short term, this is challenging for the Fund as we see a number of UK stocks as being very undervalued. On a 5.5% starting yield, the UK market would only need a half percent long-term real growth in dividends to offer a minimum of a 6% long-term real return. Even with Brexit, that should be achievable. The UK now looks the most attractively-valued major stock market globally, especially after considering that 77% of the MSCI UK index’s corporate profits are earned outside of the UK.

The other economic overhang is the trade war which, despite occasional signs of a thaw, has generally continued to escalate over recent quarters. We are still a long way from the US and China agreeing a wide-ranging trade agreement. Moreover, the US government has now begun to impose tariffs on European goods in response to a World Trade Organization investigation on aircraft parts. Although most analyses suggest that the intensification of trade tensions may have a significant but manageable impact on the global economy the International Monetary Fund (IMF) estimates -0.75% from real global growth of approximately 4% next year), in reality, simulating the spill-over effects from further rounds of protectionism into business confidence and asset prices/ wealth effects is likely to have a wide error band. Events could easily gather momentum. Our assessment of broad equity market valuations would suggest that in capturing economic sensitivity, the market is disproportionately focusing on the “risk” in the value part of the market. Valuations elsewhere in the market look increasingly exposed.

With the right policies, economies should stabilize unless reckless policymakers are determined to drive off a cliff

With Brexit and trade tensions overhanging the global economy, it is not surprising that recent economic data points, especially from Europe, Japan and China have continued to be very soft, although some weakness can continue to be explained by temporary factors such as the change in auto emissions regulations in Europe, a Brexit-related investment slowdown and stockpiling, and consumer edginess in China.

Worries about a sharper slowdown are real, but despite the length of the economic cycle and the flattening and slight inversion of the yield curve in the past year, on balance, a severe recession seems less likely as long as central bankers remain vigilant, inflation stays benign around the developed world, real interest rates remain negative in most developed markets and governments use fiscal policy thoughtfully and carefully. Indeed, despite limited ammunition, central banks have reacted in a largely coordinated way to try and support growth. While the pace of easing has disappointed some political leaders and market participants, the FT reported that more than half of central banks cut interest rates in the third quarter. With supportive monetary conditions and hopefully some resolution to the Brexit and trade challenges, the probability is that economic growth will continue, albeit more slowly, as the IMF has forecast.

Against a backdrop of loosening monetary policy, value has lagged growth

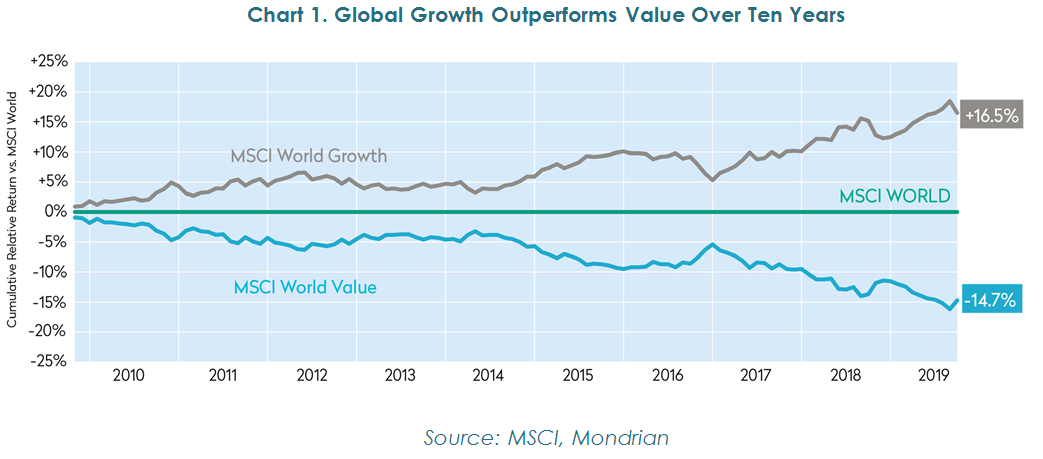

Since the financial crisis, investors are well aware that growth investments in equity markets have significantly outperformed value, although the extent of it can still be surprising (see Chart 1 below). As we have written previously, we believe that this can be understood in a Discounted Cash Flow (DCF) or Dividend Discount Model (DDM) framework as exceptionally loose monetary policy suppressing investors’ discount rates. As discount rates are dragged lower, investors much more willingly trade off cash flows today against cash flows far into the future. There is a conflict, however, between on the one hand ascribing such a large share of a company’s value to far-off cash flows, and on the other hand the inherent difficulty of projecting those far-off cash flows with any degree of precision. Despite Mondrian’s International Value Equity Fund having a shorter duration, the challenge of forecasting cash flows even 5-10 years out explains the strong emphasis that we have always placed on scenario analysis and on the skew of outcomes for any prospective investment.

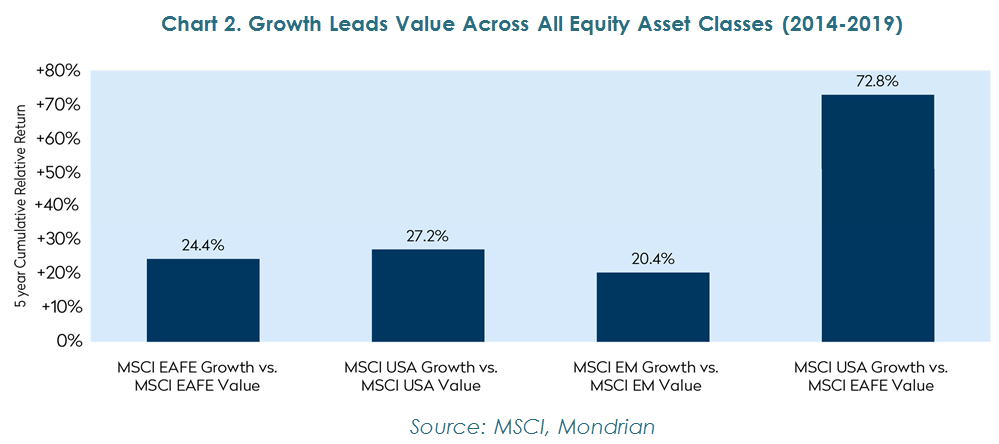

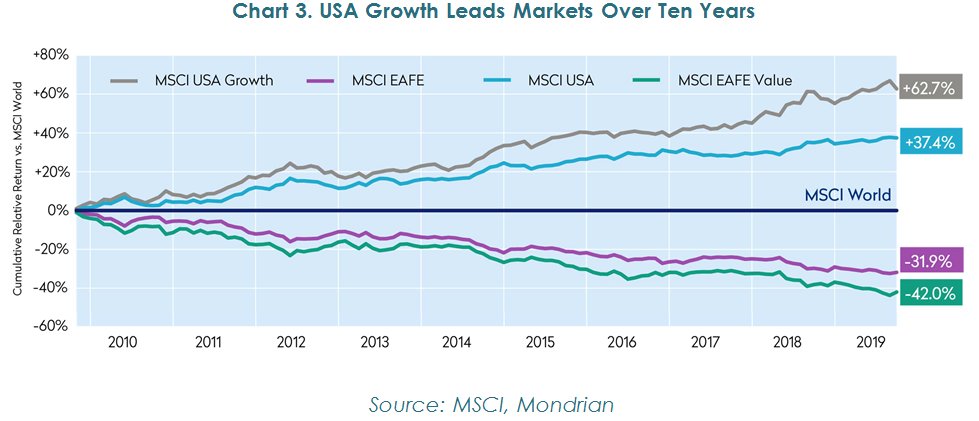

The outperformance of growth stocks has accelerated in the past five years. Over that time period, US growth stocks have returned 81.5% and outperformed MSCI World by 28.3% while EAFE Value has underperformed US growth by a staggering 72.8%. Investors have increasingly shunned international value stocks in favor of US growth companies.

As a result, the biggest gap in aggregate returns over the past 10 years has been US growth against EAFE value.

The market is mis-valuing risk, leaving value stocks at very attractive levels

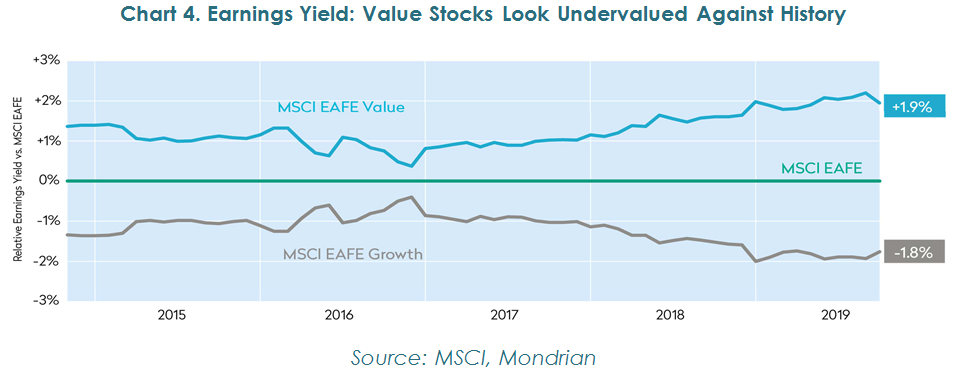

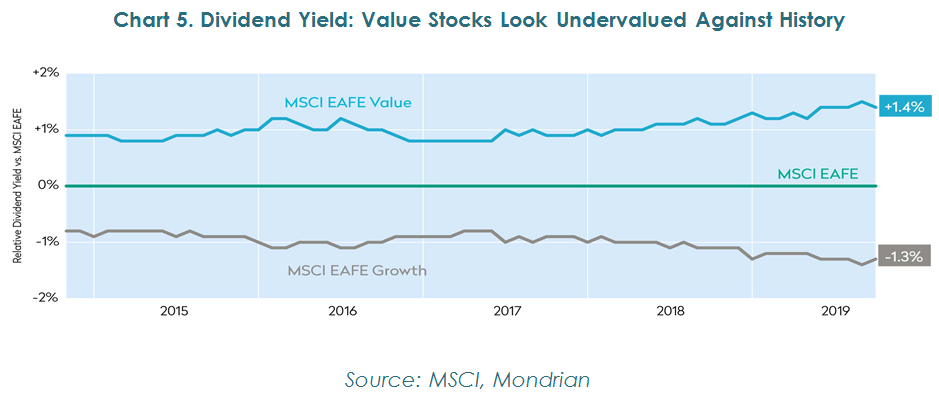

While the performance differential between value and growth stocks has been very substantial, the underlying stock earnings and dividend trajectory has not reflected a difference of such magnitude. This has opened a substantial valuation gap between the value sub-sector of the market and companies at the growth end as shown by this relatively simple analysis of earnings yield and dividend yield versus the broader index for the growth and value sub-indices. Against a longer-term (20 year) history of approximately +/- 1.0%, for earnings yield and +/- 0.8% for dividend yield, the valuation gap has widened out significantly over the past five years.

We believe that in its valuation decisions, the market is making two classic mistakes: because discount rates have fallen and are now at extreme lows, it is overvaluing growth profits which will hopefully be earned at some point well into the future and penalizing companies earning money today. This is exacerbated by the market’s fears about economic cyclicality, geopolitical risk and longer-term transitions, such as the development of electric vehicles.

With the return backdrop of the past five years, we appreciate that it can be challenging for investors to remain confident of value strategies. While changes in investors’ discount rates impact near-term share price movements, it is the long-term future business profits and cash flows, as they become known, which are the primary determinants of asset valuations. Mondrian’s long-term investment process, which focuses on the present value of future cash returns to investors, aims to enable clients to earn relatively steady returns from their portfolios by capturing investment income in periods when market re-rating moves against them such as in the past few years, while offering them the opportunity to benefit from capital preservation and return when investment markets focus on economic and valuation realities. Forecasting that switch can be extremely challenging, if not impossible, but we take solace in the fact that the prevailing exceptional conditions in capital markets are presenting very attractive opportunities for patient value investors.

This information should not be relied upon as research or investment advice regarding any particular security. This is intended to provide insight into the manager’s investment process and strategy. Forward looking analytics are not a forecast of the Fund’s future performance.

To determine if the Fund is an appropriate investment for you, carefully consider the fund’s investment objectives, risk, and charges and expenses. This and other information can be found in the funds full and summary prospectus which can be obtained by calling 888-832-4386 or by visiting www.mondrian.com/mutualfunds. Please read the prospectus carefully before investing.

Investing involves risk, including the possible loss of principal. International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, as well as increased volatility and lower trading volume. The Fund may invest in derivatives, which are often more volatile than other investments and may magnify the Fund’s gains or losses.

The Mondrian Investment Partners Limited Funds are distributed by SEI Investment Distribution Co. (SIDCO). SIDCO is not affiliated with the advisor, Mondrian Investment Partners Limited. Mondrian Investment Partners Limited. Mondrian Investment Partners Limited is Authorised and Regulated by the Financial Conduct Authority.