Post Financial Crisis economic concordia breaking down, exposing underlying financial market and economic fragility

After 15 years of post-crisis reconstruction – through low interest rates, debt socialization and the strengthening of capital buffers in the global banking system – high energy prices, high inflation, rising interest rates and war in Ukraine have pushed volatility higher and are once again exposing the fragile backdrop to the global financial system. The ongoing mini-crisis that erupted in the UK at the end of September, triggered by poorly thought out and poorly executed economic policy, underlines the broader systemic fragility, the challenges and risks of portfolio illiquidity and the very narrow execution space for policymakers. With the ongoing battle between higher interest rates and inflation unresolved, policy-makers will need to be wary of similar crises emerging elsewhere across financial markets.

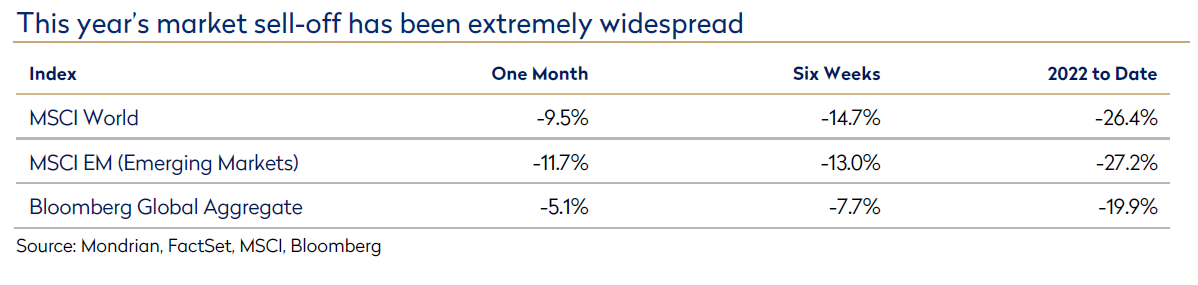

While we have been concerned about ongoing financial system fragility for some time, what has been striking over the past six weeks, and indeed this year, is how few places there have been to hide.

Asset class returns for equities and bonds have been weak across the board this year. But after a strong market bounce in July, high correlations within asset classes through the August and September weakness have made the recent quarter, after a relatively defensive start to the year, a challenging market for those managers like Mondrian who focus on downside protection.

Mondrian does not attempt to predict future short-term market directions. Instead we focus on estimates of probable underlying valuation as a basis to forecast future, expected long-term real returns. In the current volatile environment, with publicly traded assets bearing the pressures of illiquidity elsewhere in portfolios, we believe that significant long-term valuation anomalies against fundamentals are emerging, especially within global assets. We believe that a defensive, cash-flow oriented, shareholder-return focused investment philosophy can be particularly attractive in a highly uncertain environment.

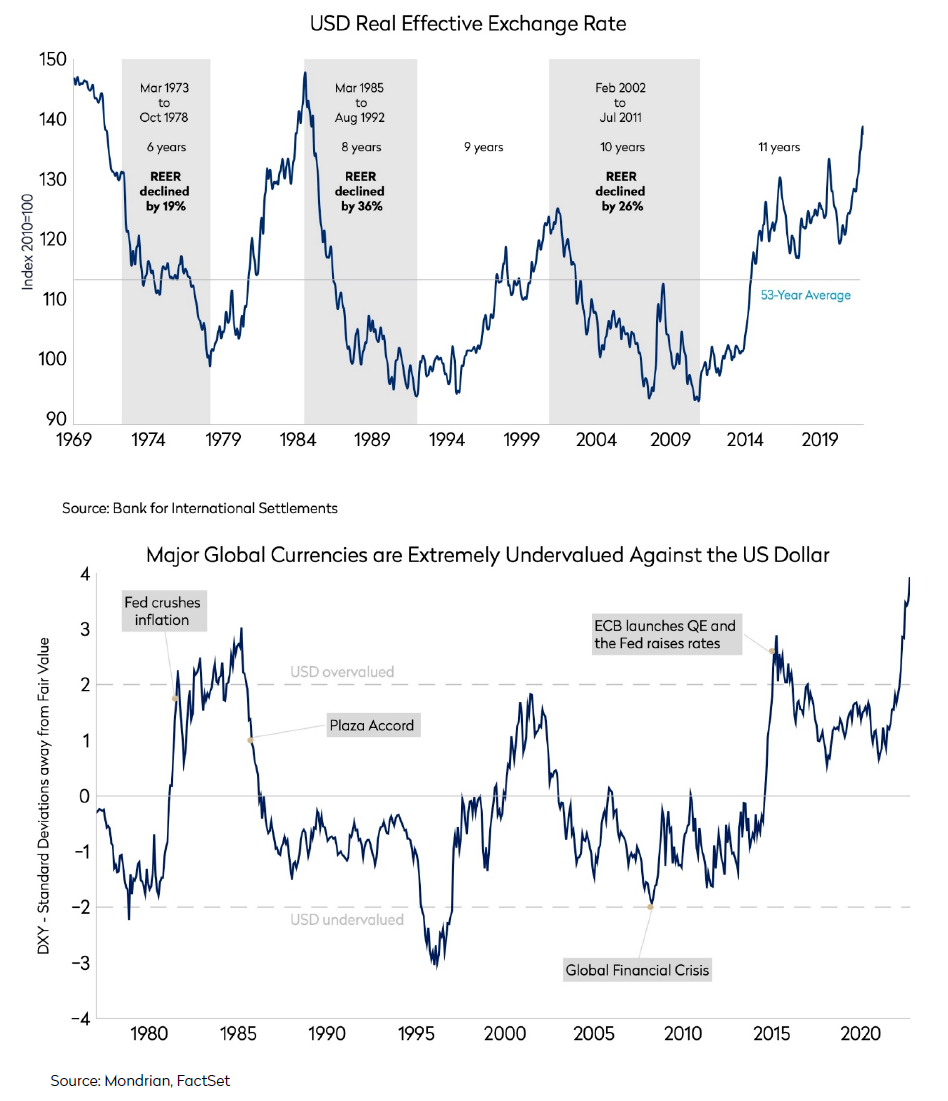

Extreme US dollar overvaluation a manifestation of financial market fragility

Dislocations have arisen in foreign exchange markets. US dollar real exchange rates are approaching mid-1980s highs.

Using Mondrian’s Purchasing Power Parity (PPP) methodology, the undervaluation of most currencies against the US dollar is now extreme. A lot of column inches have been written by commentators on the nuances of different valuation methodologies and comparisons with previous periods of extreme overvaluation. While the magnitude and historic positioning of the current overvaluation may be debated, the broad conclusion is no longer seriously contested. Our recent research trips to the US, Europe and Japan have reinforced the conclusions from the PPP analysis.

Risk aversion and higher interest rates have made the US dollar an attractive asset. This is now beginning to create economic strains across the world. The strong US dollar is exporting at least some US inflation to the rest of the world through commodity prices and the prices of other goods traded in dollars. Limited post-pandemic travel has meant that holders of US dollars are investing and spending less of their money abroad, reducing some natural economic equilibrium mechanisms. In some emerging markets, despite relative resilience so far, heightened inflation and US dollar denominated debt are beginning to exacerbate existing system stresses.

While a small number of countries made provisional forays into currency markets in September, there is not yet a global consensus to enable broader intervention in foreign exchange markets. While the 1980s Plaza Accord abruptly changed the trajectory of the US dollar valuation, the general policy of central banks in the almost 40 years since has been to limit intervention in the market. This has been evident in the way the Bank of Japan has handled the recent weakness of the yen. Over the past year, numerous market commentators have declared “must-defend” levels, but as the yen has moved through each of those, the Bank of Japan has broadly declined to act. Towards the end of September, the Bank of Japan finally stepped into the market, only to be overwhelmed the next day by the eruption of the UK mini-crisis. While the precise policy direction to manage the exchange rate polarity remains unclear, currency markets look to be approaching breaking points and US dollar overvaluation is likely high on most central bank agendas.

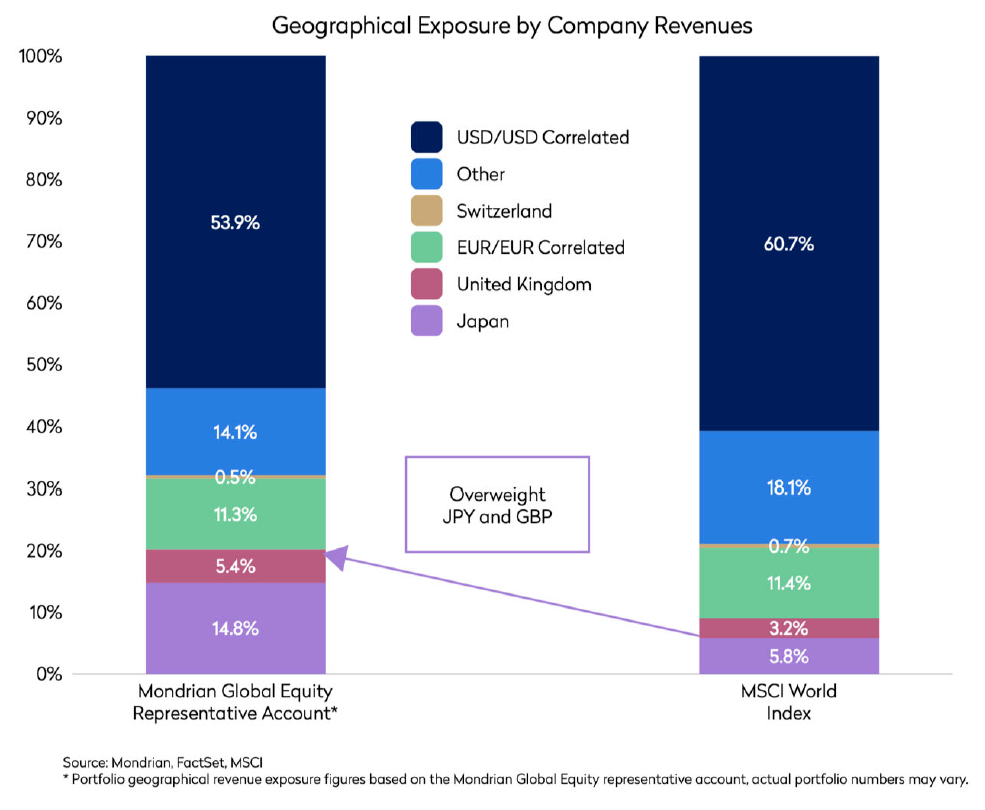

The portfolio’s underlying currency exposure is directed away from the US dollar

Economically, relative currency undervaluation should increasingly offer support to economies outside the US; it is a reasonable expectation that marginal investment will, over time, be attracted to those markets with lower asset prices and a lower cost base. This should particularly support relative economic activity in other parts of the world where real currency movements have been the largest even if exchange rates move off their current polar extremes.

While it is hard to know precisely what will change investors’ attitudes towards the US dollar, Mondrian’s investment strategy is continuing to identify attractive companies with revenue streams generated outside the US dollar. To illustrate this point, the chart below highlights the geographical distribution of revenues earned by the companies in Mondrian’s portfolios against the broader market.

The underlying earnings and cashflows in Mondrian’s portfolios are weighted away from the US dollar towards developed market currencies with a high degree of undervaluation, supported by the local valuations of stocks in the portfolio.

Could a reversal in currency valuations herald a structural change in investment returns?

Our investment focus has always been on maximizing risk-adjusted returns for our clients, taking into consideration currency movements, based on our long-run Purchasing Power Parity (PPP) approach. While the US market constitutes 70% of the MSCI World benchmark, in terms of money earned, the US is a smaller share of global GDP, representing less than 16% of the global economy. Clearly, there are many large, successful companies in the US but the US market is a highly concentrated index compared to other indices. Returns from different markets can rotate due to relative valuations, growth and competitive cycles. While we have identified a number of compelling US ideas this year, including Berkshire Hathaway, Micron and DuPont in the most recent quarter, we believe that there are a number of global businesses listed outside the US that are equally attractive, with undervalued exchange rates. Investing in global equities enables investors to move in and out of markets, taking advantage of the disparity in currency and stock valuations globally. We believe a defensive investment approach focused on cashflow generation within a structured scenario analysis framework creates portfolios with optionality on the upside, while providing downside protection. Marrying the two is critical as a global investment manager.

Disclosures

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.

For investment professionals only.

Purchasing Power Parity Valuations are calculated using proprietary Mondrian models. Further information on these models can be provided on request. Information and data is correct as at 30 September 2022. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority. Registered in England No.2533342. Mondrian Investment Partners Limited is registered as an Investment Adviser with the SEC (registration does not imply any level of skills or training).

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors. The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper.