Implications of the Iran Conflict

Since the end of the Second World War, the US has underpinned a largely rules-based order, built on collective security and international law. However, the global balance of power is currently evolving from a US-led unipolar system to a more fragmented multi-polar version; geopolitical risks have risen as a consequence. US commitments to decades-old alliances and institutions like NATO and the UN have been reappraised. This has triggered a sense of panic amongst US allies, most notably from European nations that had relied on US defense support whilst curbing their own defense spending. In this more uncertain geopolitical landscape, there are now two theatres of major military conflict – Ukraine and the Persian Gulf. Below we consider the shorter-term scenarios for the military phase of the Iran conflict (which is rapidly evolving and appears to be entering a truce period at the time of writing), and the longer-term post-war implications for global markets.

Short-term Scenarios for the Military Phase of the Conflict

A short duration campaign in Iran seems politically expedient for the Trump administration, to avoid straining the domestic support base. A short conflict is also imperative from a global energy supply and price perspective. Approximately 20% of the world’s oil and LNG supply passes through the Strait of Hormuz, mainly destined for Asia. With Iran controlling access through the Strait, ~20mbd (million barrels per day) of oil has been blocked. Some of this oil has been rerouted: ~4-5mbd of the stranded oil now flows through Saudi Arabia’s East-West pipeline to the Red Sea, ~0.5mbd now flows through the Fujairah pipeline in the UAE, ~0.2mb is exported from Iraq, and Iran has agreed to the passage of some cargoes destined for India and China. Overall, ~12-14mbd (million barrels per day), equating to 12-14% of the global oil supply, has been effectively stranded by the closure of the Strait.

To help offset this supply shock, releases from various strategic oil reserves (IEA, US) have been authorized, but flow rates here are low and likely only ~4-5mbd. In addition to the closure of the Strait of Hormuz, approximately 4mbd of exports transit from the Red Sea through the Bab-el-Mandeb Strait, where hostile, pro-Iranian Yemeni Houthis forces could threaten safe passage. The overall effect of this supply shortage has driven up oil prices from approximately $60/bbl in February to well over $100/bbl at times in March. The exhibit below shows these two chokepoints:

![]()

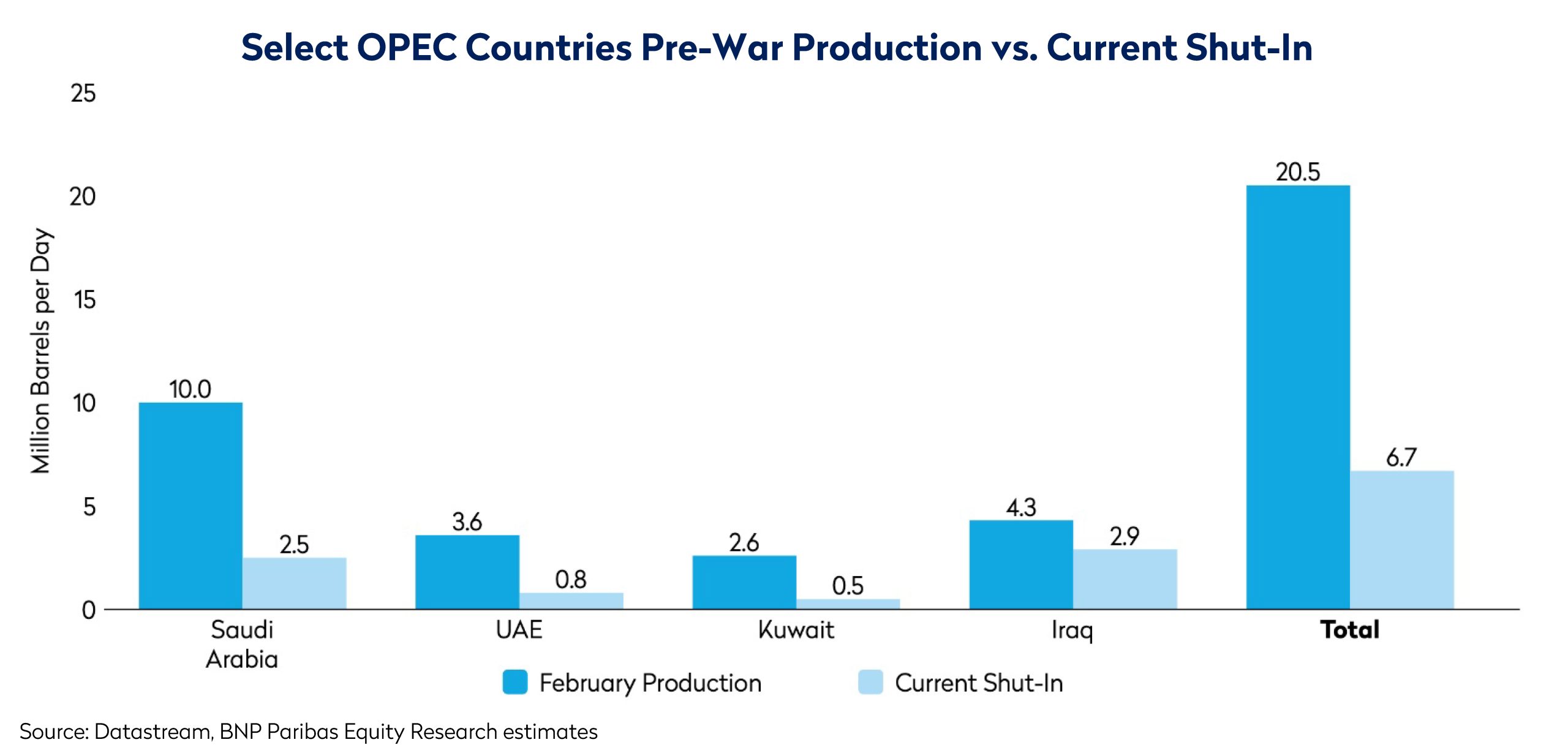

The duration of the conflict is an important consideration extending beyond the immediate bottleneck effects of the Strait of Hormuz, to include broader cascading impacts. Once oil storage capacity in the Middle East is full, and oil cannot find an export route out, Middle Eastern production will start to get “shut-in”. Once producing assets are shut-in, it is not always straightforward to reopen them, and any damage / degradation only becomes apparent on reopening. This tipping point has now been reached in parts of the region, as the exhibit below illustrates. In the downstream, refineries can be shuttered, but the longer they are offline, the more expensive and time-consuming it becomes to restart.

There is also the risk that energy infrastructure is targeted by military action. Some material damage has already been inflicted (the partial damage to the Ras Laffan LNG plant in Qatar, impacting ~17% of Qatar’s LNG export volumes potentially for several years; and damage to processing facilities at the giant South Pars gas field in Iran, affecting ~12% of Iran’s gas production). Further damage to upstream assets, midstream pipelines or downstream refining assets could impair production capacity for a much longer period than the duration of the military conflict.

As duration is the key factor from a political and an energy price perspective, we see two main timelines to consider:

- Conflict lasts one-to-three months (“extended period of higher oil and gas prices, with material headwinds to global growth for 2026”): the conflict would last long enough to see storage capacity limits reached, triggering some shutting-in of producing assets in the Middle East. An extended period of fighting would likely lead to some damage to energy infrastructure, delaying the normalization of energy markets well beyond the point of resolution of the military action. Asset restart times would vary between days / weeks / months depending on the extent of the downtime & the extent of the reservoir damage. LNG production from Qatar would take longer to recover due to the extensive damage incurred at Ras Laffan, leading to elevated spot LNG prices. The oil price would likely remain around $100/bbl for several months (i.e. significantly higher than pre-war levels) as the lag effect of undersupply is worked through, and we would likely see episodes of product rationing and demand destruction. Domestic US support for the Iran conflict would likely weaken should the campaign drag on, and the economic cost of a higher oil price be increasingly felt by consumers. Global inflation would likely move higher, monetary policy would be expected to remain somewhat tight, consumer confidence would weaken, and global growth would likely disappoint.

- Conflict lasts longer than three months (“nightmare scenario for global economic growth”): an oil supply shortfall of more than 10mbd for an extended period would likely drive oil prices up beyond $150/bbl. We would likely see extensive demand rationing, demand destruction, and an accelerated push into non-fossil fuel sources of power in energy importing countries. Global inflation rates would rise, monetary policy would likely remain tight, and economic growth would suffer significant headwinds, with many major economies entering recession.

The balance of probabilities suggests a relatively short conflict, supported by multiple factors: President Trump’s rhetoric shows a preference for a short campaign, the negative effect of high oil prices on global growth supports a quick resolution, the upcoming US midterm elections in November would become more challenging for the Trump administration if this conflict were to drag on, and the lack of an Iranian popular uprising against the incumbent powers suggests that regime change would be difficult to achieve. Recent news of a two-week ceasefire supports this as the most likely outcome.

However, three key factors remain unresolved: (i) Regime change in Iran; (ii) Iranian control of partially enriched uranium; and (iii) Iranian control of the Strait of Hormuz. Any curtailment of the conflict with these factors outstanding would mean a risk overhang for oil supply, potentially extending into the longer term. On this basis, the tail risk of the second scenario cannot be ignored. The list of demands from both sides for ending the war makes peace talks complicated.

Long-term Implications

Turning to the likely longer-term implications of the conflict in Iran on energy markets: this war, together with Russia’s ongoing invasion of Ukraine, highlights the chokepoints in the energy system. 20% of global oil and LNG passes through the Iranian-controlled Strait of Hormuz, and pre-2022, Europe relied on Russia to supply ~40% of its gas needs – two material fragilities in the global energy system. However, whilst piped gas is inherently a regional product, making the Ukraine conflict a mostly European problem, LNG and crude oil are largely fungible and globally traded products. Oil price benchmarks have risen around the world, not just in the Middle East or Asia. The Hormuz situation has the potential to be far more dangerous to the global economy.

The conflicts in Ukraine and Iran have forced a re-appraisal of the energy trilemma, with security of supply and affordability increasingly weighted more heavily versus climate sustainability. This is likely to lead to a relaxation of energy transition requirements (including disclosure regulations, decarbonization targets, emissions trading schemes), alongside a reassessment of permitting for strategic or domestic fossil fuel resources.

Governments will face pressure to ensure diversification of energy supply across fuel types and geographic sources. This will likely see an acceleration of energy generation across all sources to help mitigate the weaponization of fossil fuels. This conflict has shown the durability of even weakened rogue regimes like Iran, and a reminder of the volatility of this region, which is likely to restore a geopolitical risk premium to the oil price.

In the long term, as the multi-polar world searches for a new equilibrium, we see heightened geopolitical risks, looser ties between the US and its allies, a rising culture of mercantilism and national self-interest, and a greater emphasis on energy independence.

Conclusion

The portfolio had a slight underweight to the energy sector going into this conflict, which detracted from relative returns in March, having been a positive for most of the prior three years.

We are revisiting our oil and gas price assumptions and now expect an upward revision in the short term. The oversupply situation in the first half of 2026 has effectively been resolved by the war, leading to tighter market fundamentals for the remainder of 2026. The duration of the conflict will determine how long this tightness lasts.

Longer-term, Iran’s demonstrated ability to close the Strait of Hormuz even under significant military pressure, highlights a fragility in global supply, which is likely to be reflected in a risk premium. However, there are certain factors that help to moderate upward changes to our long-term oil price assumptions. Firstly, apart from Ras Laffan, the structural integrity of the oil and gas assets in the region remains largely intact for now and this remains a priority for the US. Secondly, North American oil production from shale is far larger today in the global supply mix and higher oil prices have the potential to increase production in a fairly short period of time. Finally, on the demand side, renewable energy and electric vehicles are more economically viable options today than ever before and can help to curtail demand, alongside any slowdown in economic growth. Looking ahead, the portfolio’s overweight exposure to more defensive sectors like health care and consumer staples, combined with an underweight exposure to more economically sensitive sectors such as information technology and consumer discretionary, should provide resilience if the Iran conflict continues longer than expected or results in a broader economic slowdown.

We continue to focus on identifying the most attractive risk-adjusted opportunities, investing with a long-term perspective grounded in rigorous scenario analysis.

Disclosures

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials. The information set forth herein is a summary only and does not set forth all of the risks associated with the investment strategy described herein.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed, and it may be incomplete or condensed.

It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this document. Examples of securities will represent only a small part of the overall portfolio and are used to illustrate our investment approach. Any holdings are subject to change and may not feature in any future portfolio. More information on holdings is available on request.

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.

Mondrian Investment Partners Limited is authorised and regulated by the Financial Conduct Authority (Firm Reference Number: 149507). Mondrian Investment Partners Limited is also registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).