For the last five years, International Equity investors have navigated an exceptionally challenging environment. A global pandemic, rising inflation, an aggressive interest rate cycle, sharp sector rotations and persistent geopolitical uncertainty have all tested active managers in multiple ways.

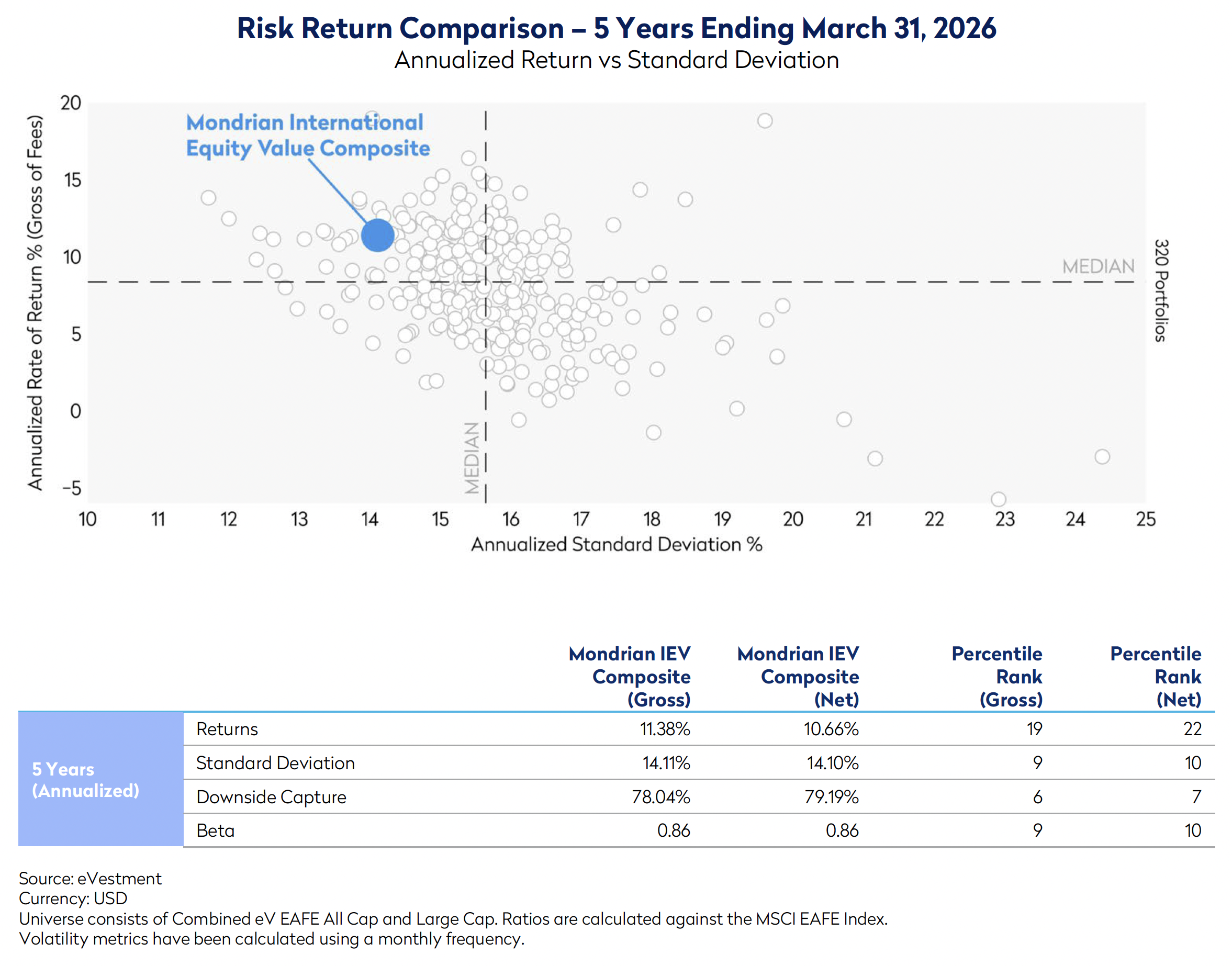

Amid this volatility, Mondrian’s International Equity Value strategy has delivered top quintile returns against both the MSCI EAFE benchmark and the peer universe in the five-year period to March 31, 2026, and did so with lower realized volatility than the median manager. Equally important, however, is how those returns were achieved.

In an environment that broadly rewarded concentrated bets on cyclicals or perceived AI-beneficiaries, Mondrian’s results came from the consistent application of our philosophy delivering attractive asymmetric return characteristics. Our strategy has focused on delivering attractive real long-term returns through a diversified portfolio, grounded in fundamental analysis, valuation discipline and strong focus on risk-adjusted outcomes.

The chart illustrates the relationship between return and risk across the peer universe. While many of our peers delivered attractive outcomes over the period, the volatility required to achieve those returns varied considerably. Mondrian’s positioning highlights the strategy’s risk-adjusted return profile: top-quintile returns were achieved alongside lower realized volatility than the median peer. Importantly, in line with our investment philosophy, the strategy also exhibited strong downside capture characteristics, demonstrating an ability to protect capital more effectively during periods of market weakness. Together, these outcomes reflect a disciplined approach to generating strong relative returns while maintaining a more balanced risk profile.

This outcome reflects our disciplined investment process focused on identifying mispriced securities through a consistent bottom-up valuation framework, while maintaining diversification and disciplined oversight of risk exposures. Portfolio positioning is not bound by specific regional or sectoral relative weights but are the result of where our valuation process identifies the most attractive long-term opportunities and risk-adjusted return potential.

Over a period that has tested investors across multiple market regimes, Mondrian demonstrated that attractive returns, downside protection, and lower risk need not be mutually exclusive. For investors seeking not only returns, but confidence in how those returns are generated, that distinction is important.

Disclosures

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials. The information set forth herein is a summary only and does not set forth all of the risks associated with the investment strategy described herein.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed, and it may be incomplete or condensed.

It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this document. Examples of securities will represent only a small part of the overall portfolio and are used to illustrate our investment approach. Any holdings are subject to change and may not feature in any future portfolio. More information on holdings is available on request.

Unless otherwise stated, all returns are in USD.

All references to index returns assume the reinvestment of dividends after the deduction of withholding tax and approximate the minimum possible re-investment, unless the index is specifically described as a “Gross” index

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.

Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority (Firm Reference Number: 149507). Mondrian Investment Partners Limited is also registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).