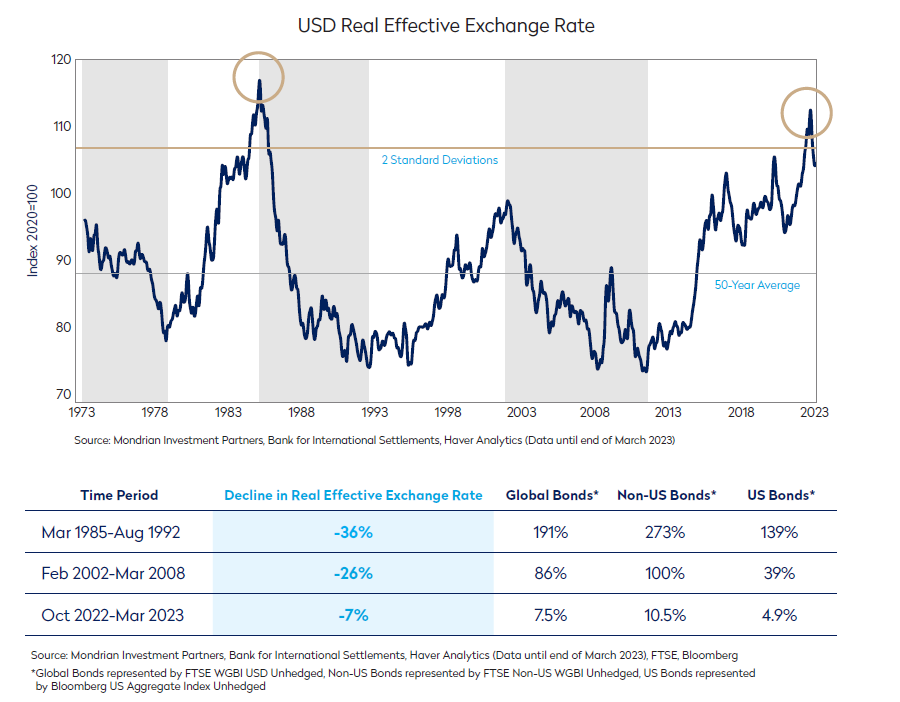

- Only the second time the USD has been over 2 standard deviations overvalued (see circled points in the chart above)

- If history is any guide, the dollar could have much further to fall, boosting the return on unhedged global bonds vs US domestic bonds

- High-quality global bonds have tended to be countercyclical, offering excellent long-term diversification benefits to domestic portfolios

- As in the 2000s, Mondrian is heavily underweight to the US dollar across our fixed income portfolio

Disclosures

The opinions expressed here are Mondrian’s views based on proprietary research. Past performance is not a guarantee of future results.

The value of fixed income instruments is affected by interest rates, inflation, and credit ratings. Although, investments in emerging markets offer a higher yield, they involve a greater risk of loss and higher volatility than investments in developed markets. Higher yielding bonds tend to carry a greater risk of loss due to issuer default.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without notice. This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,” “estimate,”

“anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

This document is an internal research paper. The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance that the investment objectives of the strategy will be achieved.

This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission of Mondrian Investment Partners Limited.

Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority.

Mondrian Investment Partners Limited is registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).