Governments around the world are increasingly revealing their domestic targets to meet the Paris Agreement objective of limiting climate change to well below 2°C and ideally below 1.5°C. However, most of these pledges currently lack a strategy or roadmap of how to achieve these targets. Once these strategies develop it will become clear the vast amount of financing needed to support the transition but also the significant role that ‘brown’ sectors will need to play.

Brown sectors are imperative to the economy of today and cannot simply be shut down. There needs to be realistic transition in these sectors without fully compromising current vested interests. The transition to a greener and more sustainable future will be particularly challenging for the regions that are dependent on these industries such as mining, oil and gas extraction or chemical and material production. However if there is to be a global solution to limiting climate change and adapting it will arguably be these regions and industries that have the most significant role to play.

Whilst green bonds will not be the only source of finance across the full transition of these industries, there is still an opportunity for green finance now as well as in the future to facilitate the transition to greener, more sustainable ways of doing business and in doing so, open these industries to a growing demand for sustainable investment.

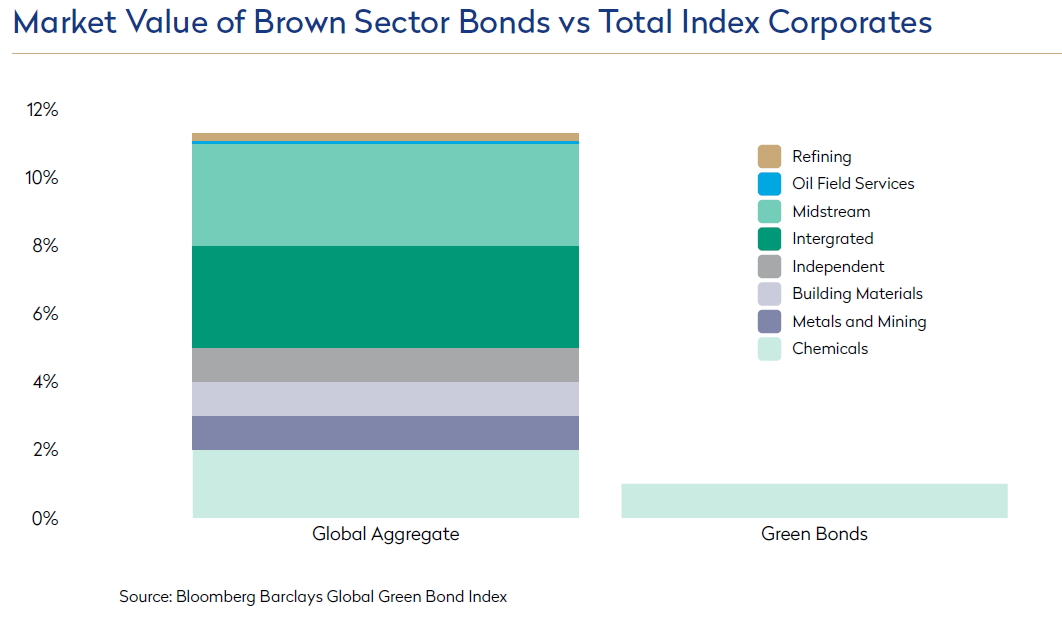

The opportunities for green investment in these industries could be vast. LG Chem Ltd, a chemical manufacturer, is the only issuer in the Bloomberg Barclays MSCI Green Bond Index from the obvious brown sectors. The company’s green projects include the development of batteries for electric vehicles and have outstanding green bonds of around USD 1.6 billion. This compares to ‘brown’ bonds outstanding in the Bloomberg Barclays Global Aggregate Index of over USD 1.1 trillion. Whilst there is not a clear link between refinancing current bonds into green bonds, the changes that these business will see in years to come will inherently ensure more green investment.

The obvious question is whether these sectors can feature in the Mondrian Global Green Bond strategy as we stand now. We believe they could. We aim to only invest in what we consider to be genuine green bonds and that will remain a cornerstone of our investment process. However, if the entities operating in these sectors invest in true green projects and support those initiatives with a clear strategic change to a greener future then we would consider these as eligible.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without notice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,”

“estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance

that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which

are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance tha the investment objectives of the strategy will be achieved.

This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission

of Mondrian Investment Partners Limited.