Executive Summary

- Emerging Markets Debt is a large and growing asset class offering much higher yields than traditional fixed income

- Given exploitable inefficiencies, the asset class ideally lends itself to active management

- The two broad forms of EMD are Local Currency EMD and Hard Currency EMD

- Local Currency EMD is denominated in the domestic currencies of issuers while Hard Currency EMD is issued in an advanced economy currency, predominantly the US dollar

- Local Currency EMD is by far the larger, more liquid, and generally higher credit rating quality of the two

- Both long term strategic allocation considerations and short-term valuations are favorable for Local Currency EMD

- Mondrian’s systematic and consistent approach to portfolio construction has yielded strong long-term results in this asset class

Introduction

An allocation to high-quality, developed market government bonds continues to play an important role in reducing the volatility of a well-diversified portfolio. However, there is no getting away from the fact that, despite recent rises, yields in developed country bond markets are low by historical standards and often fail to compensate even for relatively modest projections for inflation. Given the secular forces that have led to the long-term decline in equilibrium real interest rates, this situation is likely to persist. An allocation to Emerging Markets Debt (EMD) can complement traditional fixed income by enhancing long run returns and acting as an important diversifier within global portfolios.

The EMD Asset Class

Over the past couple of decades, EMD has matured into a large, diverse, and growing asset class. According to the Bank for International Settlements (BIS), there is currently more than US$35 trillion of emerging markets bond issuance outstanding – about a quarter of the total global fixed income universe. The asset class encompasses a broad variety of issuers including both governments and corporates. It lends itself ideally to active management given inefficiencies that can easily cause valuations to become detached from fundamentals. For instance, currency trading and access to certain bond markets can be restricted for non-residents and there are often unwarranted bouts of risk aversion, contagion, and exchange rate overshooting. These can all be exploited by an active approach. It is also an asset class where an integrated approach to Environmental, Social and Governance (ESG) issues is particularly useful in making a rounded assessment of asset valuations. For instance, institutional factors such as corruption, the rule of law and preparedness for health or climate-related emergencies are often what separate those countries with poor credit fundamentals from those with good credit fundamentals.

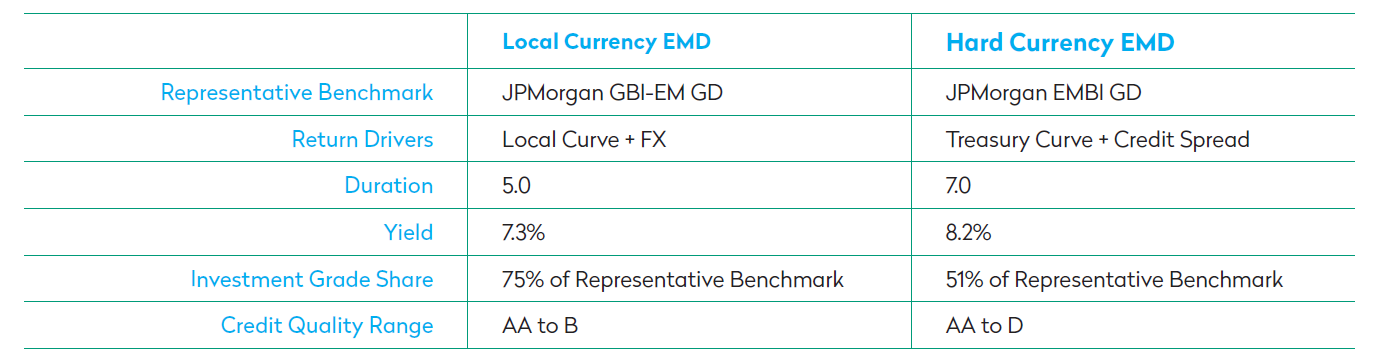

Although there are many ways to dissect the EMD asset class, the most important distinction is between Local Currency EMD (denominated in the domestic currency of the issuer) and Hard Currency EMD (denominated in a developed market currency, such as the US dollar or euro). The structural characteristics of these two broad segments of the asset class are quite different.

Local Currency EMD is the more modern variant and, in terms of issuance, is much more dominant. The drivers of return to local currency EMD primarily come from local yields, principal returns (due to yield curve shifts, changes in inflation expectations and creditworthiness) and currency returns. Given that countries can be at different stages in the economic cycle, interest rates and returns can be quite uncorrelated to those in developed markets. In addition, with deepening domestic markets, local currency bonds tend to be more liquid than hard currency ones with bid-offer spreads that remained relatively narrow even during the market stress of 2008 and 2020. The list of markets with investible local bond markets, by which we mean sufficiently liquid and accessible to foreign investors, is steadily increasing. Moreover, such issuers also tend to be of higher quality. The market leading benchmark for this segment of EMD is the JPMorgan GBI-EM Global Diversified and more than 75% of the benchmark’s weight is composed of investment grade issuers.

Hard Currency EMD, on the other hand, is essentially a credit product offering a yield premium (or spread) over US Treasuries in the case US dollar denominated debt. As well as more established middle-income emerging markets, many low income, weaker credits or “frontier markets” are compelled to issue in hard currencies to attract foreign investment. The most important hard currency indices are the JPMorgan EMBI and CEMBI series, which track hard currency EM sovereign and corporate issuers respectively. Of these, the most popular benchmark for Hard Currency sovereigns is the EMBI Global Diversified, almost 50% of which is sub-investment grade. Although the headline yield on this is currently 8.2%, one must be mindful that thirteen countries, representing around 4% of the benchmark, have defaulted or trade in distressed territory as of July 2022. Excluding these issuers, the yield is more than a percent lower. Issuance in Hard Currency EMD also tends to be smaller which means that liquidity is generally much lower resulting in large bid-offer spreads and trading costs.

The table below summarizes the characteristics of these two sub-asset classes (as at 31 July 2022).

The Strategic Case for Local Currency EMD

The key motivations for adding EMD to an asset allocation are (1) return enhancement and (2) diversification. In theory, there are three fundamental reasons why EM debt should provide higher returns over the long term than traditional developed market fixed income assets:

- Higher yielding assets

- Improving fundamentals

- For local currency issues, the potential for FX appreciation

Taken as a whole, EM debt provides higher yields both in nominal and real terms than developed markets. Much of this is due to higher potential growth but also because the yields embed a higher risk premium. Over the long term, as EM economies as a whole continue to develop and catch up with their developed market peers, improved governance standards, fiscal rules and independent monetary policy provide the potential for an additional source of return: the reduction of risk premia. Issuer engagement not just on economic policy but also environmental and social factors is much more likely to reap benefits in EM debt than in developed market debt for this reason. Although one must recognize that any process of development is not a straight line and emerging markets are often hit by setbacks and

sporadic bouts of capital flight. However, contagion appears to have lessened over time as investors have become more familiar with the idiosyncrasies of distinct issuers.

In local EM markets, investor bases are becoming broader, deeper, and more stable, with the growing importance of local institutions. Increasing financial development also helps, as banks offer financial products such as savings vehicles and insurance. This helps liquidity in local markets and creates demand for governments to issue into. It also provides a source of demand in times of market stress. The growth of local bond markets is also important for the development of local pension plans, providing them with a natural home for duration and cash flow matched pension assets. There is therefore a virtuous circle involved in the twin development of pension funds and local bond markets.

In terms of diversification benefits, it is often assumed that, given an allocation to EM equities, there is no justification for an allocation to EM debt as the overall exposure to EM has already been gained through the equity allocation. This is incorrect, especially when one considers the geographical spread of the benchmark MSCI EM equity index. Investing across geographical regions aids diversification given weak correlations between them. However, with close to 75% of the EM equity index accounted for by Asia-Pacific countries (with China comprising over 30% alone) little geographical diversification (and hence diversification of returns) is offered by the benchmark EM equity index. This suggests allocations to EM equity and debt are complementary to one another as EM debt provides exposure to different sets of countries and diversification can be enhanced by investing in both asset classes.

The Tactical Case for Local Currency EMD

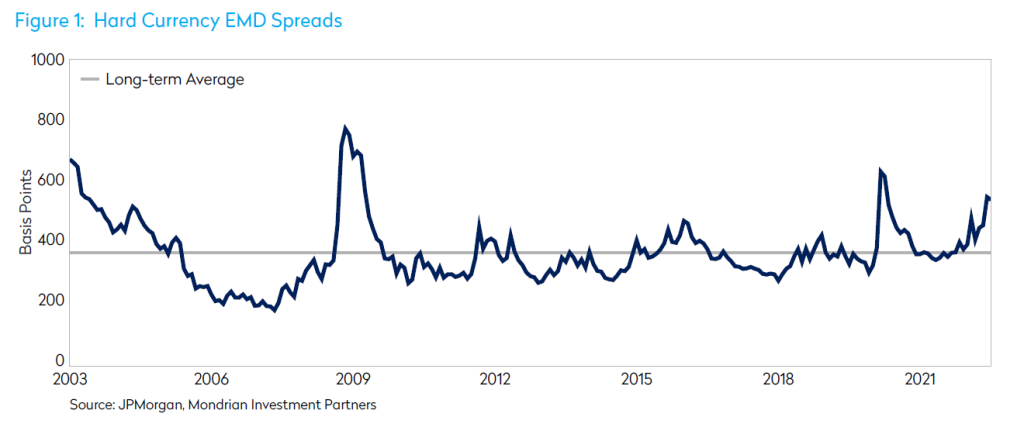

EMD has had a challenging time since the COVID-19 pandemic. Consequently, it is our view we are now at a point where both currency and bond market valuations look attractive. However, at the time of writing local currency EMD valuations look more compelling than those of Hard Currency EMD.

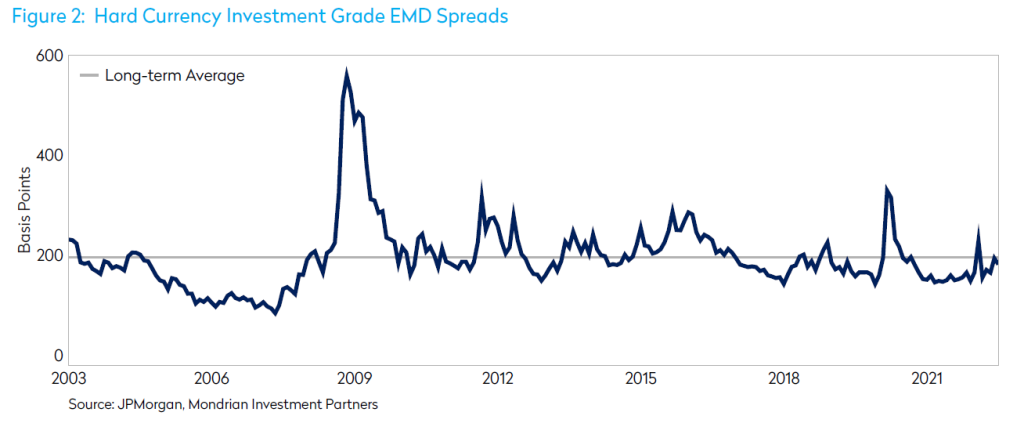

However, most of this rise has occurred for the very poorest quality credits many of which are now trading in distressed territory i.e. already in default or with a high expectation of default. Investment grade EM credit spreads are much tighter (Figure 2) and do not signal good value.

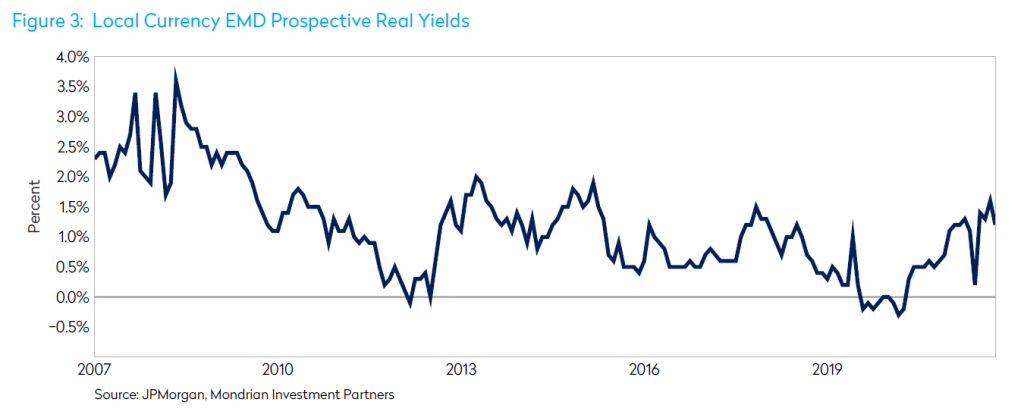

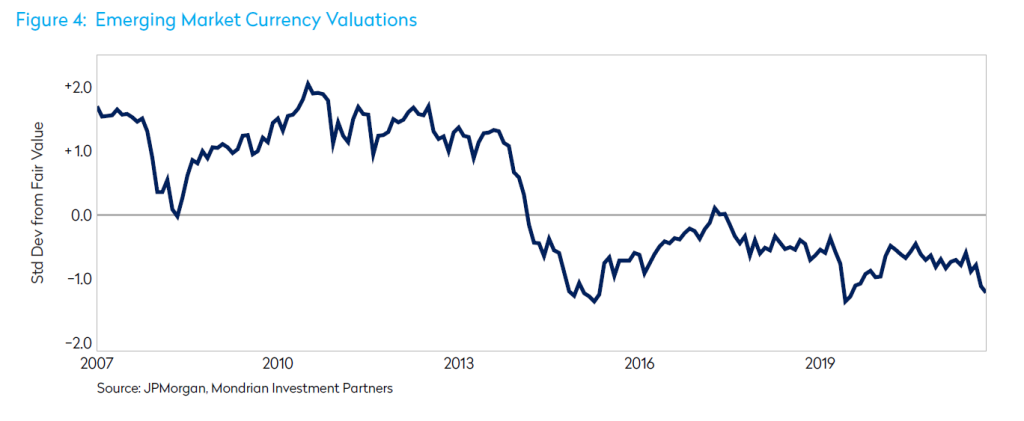

According to Mondrian’s internal metrics, local currency EMD valuations on the other hand, do look compelling. Prospective Real Yields (in other words, nominal yields adjusted for prospective inflation and credit risk) are much higher than those in developed markets and EM currencies are now cheaper in real terms than during the financial crisis of 2008 as shown in Figure 3 and Figure 4 below which show the overall Prospective Real Yield and PPP valuations respectively for the JPMorgan GBI-EM Global Diversified benchmark.

In conclusion, EMD offers considerable potential for both return enhancement and diversification. It is highly conducive to active management and valuations suggest a favorable entry point to the asset class now.

Disclosure

The value of fixed income instruments is affected by interest rates, inflation, and credit ratings. Although, investments in emerging markets offer a higher yield, they involve a greater risk of loss and higher volatility than investments in developed markets. Higher yielding bonds tend to carry a greater risk of loss due to issuer default.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without notice. This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

This document is an internal research paper. The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance that the investment objectives of the strategy will be achieved.

The value of fixed income instruments is affected by interest rates, inflation, and credit ratings. Although, investments in emerging markets offer a higher yield, they involve a greater risk of loss and higher volatility than investments in developed markets. Higher yielding bonds tend to carry a greater risk of loss due to issuer default.

This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission of Mondrian Investment Partners Limited.

Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority.

Mondrian Investment Partners Limited is registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).