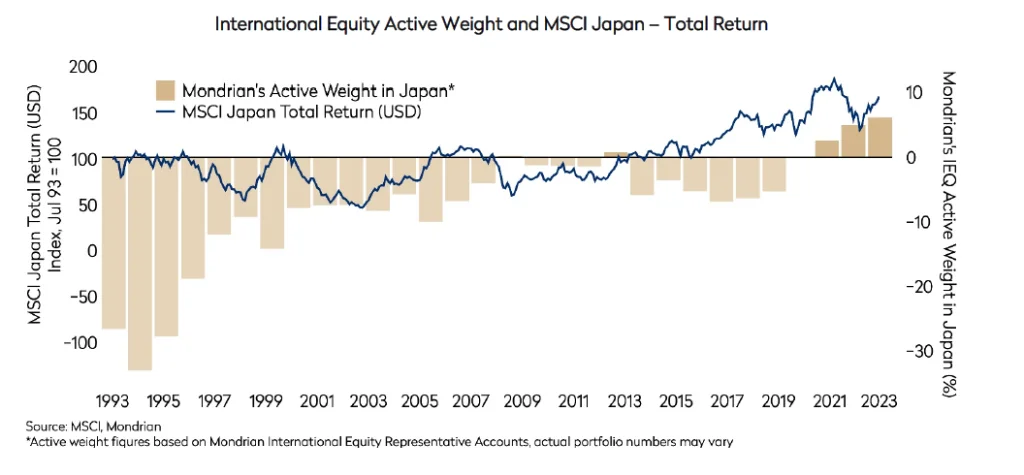

Mondrian portfolios have benefitted from overweight positions in Japan

The Japanese equity market has enjoyed a resurgence of popularity as corporate governance reforms led by the Tokyo Stock Exchange have drawn investors back. This has been welcome for Mondrian’s international and global equity portfolios which more recently have had a differentiated and contrarian overweight position.

Mondrian has a long-term track-record of adding value in Japan through both an active weight and through stock selection. Japan has been a challenged market, that only recovered to its early 1990s highs in the mid- 2010s. Over our history, Mondrian has added value to portfolios through stock selection, positive absolute returns, and asset allocation out of Japan. Across our developed equity portfolios, Mondrian was underweight the Japanese market for many years, however in recent years, we have seen value opportunities emerge, underpinned by strong growth in earnings and shareholder returns, alongside overcapitalized balance sheets supporting a positive skew of outcomes. Nevertheless, we are the first to acknowledge that Japan has had more than its fair share of false dawns – so what is driving recent returns, and is it sustainable?

Corporate governance reforms attract investor interest

The Tokyo Stock Exchange (TSE) is the latest institution to lead the domestic push for corporate governance reform, which has gathered momentum since it was started in earnest by former Prime Minister Abe a decade ago with the introduction of Japan’s first corporate governance and stewardship codes. Corporate governance standards in Japan still lag those in other developed markets, but we believe that Japan is now seeing the fastest governance improvement among peers and that it has the most value still to be unlocked from relatively straightforward improvements.

Hiromi Yamaji took over as CEO of the Japan Exchange Group, which owns the TSE, in April and has wasted no time in seeking to drive reform. The TSE has subsequently written letters to all Japanese companies asking them to explain their return on capital relative to cost of capital, to update this annually with improvement plans, and to facilitate better dialogue with shareholders. The request that management teams be more aware of cost of capital and stock prices may seem basic to global investors but it is significant in Japan where many companies still focus primarily on P&L performance.

“First of all it is important that the company’s cost of capital and profitability of capital are accurately understood, and the current situation analyzed by the board regarding the content and market evaluation. After evaluation, we would like you to formulate and disclose a plan for improvement, and then continue to implement a series of measures such as updating initiatives through dialogue with investors.”

Source: JPX, extract from April letter sent to all Prime and Standard listed companies

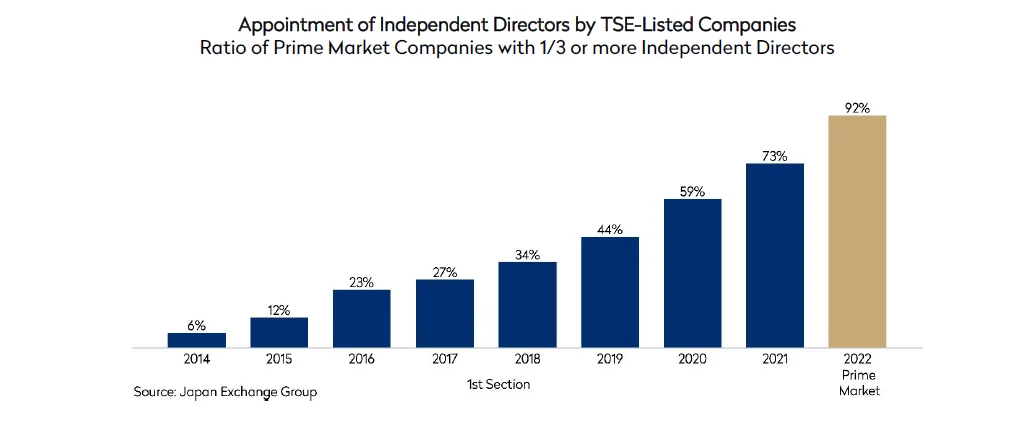

We have exchanged views with Mr. Yamaji and his colleagues this quarter in both Tokyo and London and have been encouraged by these interactions and by the message that they expect more reforms to come. These reforms add fresh impetus to over a decade of corporate governance improvements. Tangible results of these ongoing efforts are highlighted by the rise in independent directors in Japan, a reform generally believed to be correlated with higher shareholder returns.

Cross-shareholdings have long been a frustration for investors in Japan. Investments in other related businesses can be valuable if the ownership is integral to business strategy rather than just to protect vested interests – but this has been the weakness in Japan. However, the proportion of the market held as cross-shareholdings has significantly declined since 1990 and continues to decrease.

Further momentum towards unwinding is being accelerated by proxy voting advisers such as ISS and Glass Lewis recommending that shareholders vote against management teams with equity investments exceeding a percentage of net assets (20% for ISS and 10% for Glass Lewis) as well as those achieving persistently low ROEs. Upcoming changes in global bank capital rules will increase the risk-weightings for holding stocks, further incentivizing unwinding. Reduced cozy cross-shareholdings and the rise of activist investors in Japan are finally making AGM season into more than a rubber-stamping event. This was seen most starkly in the very low 50.6% approval rating for longstanding Canon chairman Mr. Mitarai this year, who only narrowly avoided a humiliating result. Other management teams have had to take note: this year has seen the highest number of shareholder AGM proposals in Japan on record.

Among portfolio holdings, Toyota Industries stands out in having more than 100% of its market cap in cross-shareholdings and we continue to engage with the company on this topic, including a meeting with new president, Mr. Ito in Nagoya last month. We were encouraged by Toyota Motor stating for the first time that the group is reviewing its cross-shareholding structure. While any unwinding is not in our base case, Mondrian’s scenario analysis captures the value of these holdings in our best case, supporting the skew of outcomes.

Fundamental research on the ground is a key part of Mondrian’s investment process and particularly important in Japan. Face-to-face communication offers real added value in identifying companies which take a more progressive approach to governance improvements, and it facilitates more impactful engagement with management. The four of us who travelled to Japan last quarter all found that management teams are very aware of the TSE requests and increasingly proactive in making positive changes. Examples this quarter among portfolio holdings include large share buybacks, adding new independent directors, increasing alignment of management compensation with shareholders, and exiting low return businesses (including using the new tax-free spin-off law). While some Mondrian holdings such as Fujitsu, Hitachi and Sony are among governance leaders, we think corporate Japan overall is still at an early stage in this journey with significantly more value to be unlocked.

Deflationary headwinds abate

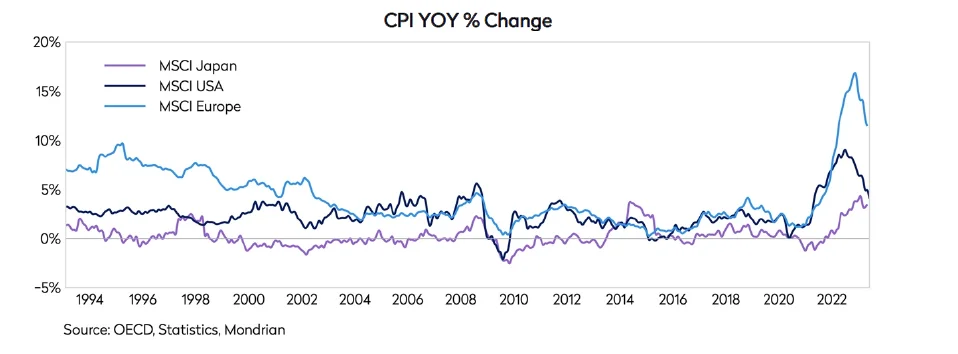

The other key change in Japan in the past two years has been increased evidence of a possible exit from the deflationary environment which had persisted for almost three decades. While labor market structures and entrenched attitudes are helping to keep inflation below other developed markets, inflation has now exceeded the Bank of Japan’s 2% target for 14 consecutive months. Recent wage hikes and a change in price setting behaviors by corporates also highlight a shift in mentality.

Japan has long suffered from a relatively narrow domestic retail investor base but the return of inflation and government reforms, including trebling individual tax-free investment allowances, may help bring domestic retail investors back to the Japanese equity market. Many Japanese companies have also engaged in stock splits aimed at facilitating retail investment after the TSE called on listed companies to lower the minimum investment amount to a more manageable level.

Earnings and dividend growth in Japan has outstripped other major markets

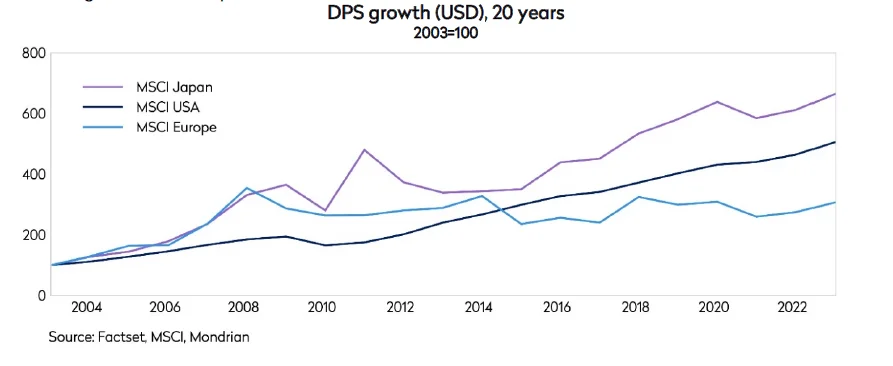

It is well understood that Japanese equities now trade at a significant discount to US equities but less commonly appreciated that Japanese corporate earnings have outgrown the US market over the past 10 and 20 years. Japan’s outstanding industrial and manufacturing expertise is serving new growth areas, with global leaders in factory automation, gaming and semiconductor supply chains. Near-term earnings are also benefitting from ongoing post-Covid travel reopening and recovering auto production as chip shortages ease. Overcapitalized balance sheets can be put to work both investing for growth and increasing shareholder returns. Corporate Japan’s excess cash has continued to build up despite dividend growth exceeding other markets and share buybacks rising six-fold in the past decade.

These strong fundamentals have not been reflected in share price performance to date, with the market continuing to de-rate. This creates opportunities which have not gone unnoticed by the likes of Warren Buffett who noted that Japanese stocks remain ‘ridiculously’ cheap.

Japan is a cyclical market and risks remain

Given Mondrian’s significant absolute and relative allocation to the Japanese equity market, we are acutely aware of the potential risks.

Japan remains an economically sensitive market at a time when the US and global economies look potentially vulnerable to recession, although strong balance sheets will provide some stability in a downturn. Demographics are a well-known challenge; Japan is not alone in confronting population decline but for the Japanese the issue is more acute. Nevertheless, corporate earnings growth has accelerated since the population peaked in 2010 and Japan’s politicians since Abe have increasingly understood that demographic headwinds increase the imperative to improve return on capital and economic productivity.

High government debt also brings risks which we continue to closely monitor, although high domestic ownership helps, while signs of a normalization towards modest inflation are healthy for economic functioning and debt repair, so long as kept to modest levels. The yen appears significantly undervalued according to Mondrian’s Purchasing Power Parity analysis and we would expect yen appreciation over time to support US dollar returns. Given this view, we do also incorporate the potential drag on margins for Japanese exporters in our bottom-up models.

Japan is susceptible to natural catastrophes including earthquakes which does impact our risk management and overall allocation. Geopolitics, energy prices and structural changes in the auto market present further risks, although there are also related opportunities. Japan has been slow to digitalize, but COVID and the addition of a dedicated Digital Minister has sharpened the focus – with Mondrian investments in Fujitsu and Hitachi among the companies well placed to benefit.

We have been underweight Japan for most of the more than 30 years that we have managed international and global equity portfolios and retain a healthy degree of skepticism. We see the recent reforms as part of a long-term governance improvement story rather than a silver bullet and fully expect bumps along the way. Crucially, however, the gathering momentum for governance improvements and more of a returns-focused culture is now driven from within Japan.

Japan offers attractive opportunities for active managers

Stock selection in Japan has contributed positively to Mondrian international and global equity portfolios’ relative returns over the long-term. Japanese holdings have again supported portfolio returns so far this year and we have rebalanced exposures from selected strong performers. Nevertheless, while volatility is expected and some near-term momentum may reverse, we see significant further upside and a positive skew of outcomes from what remains an attractively valued and under-appreciated equity market.

Within Japan, we continue to find strong bottom-up value opportunities in this broad and deep market, especially in those companies with overcapitalized balance sheets and those seeing improvements in corporate governance. This approach has worked well for Mondrian over time. We continue to see attractive opportunities in Japan today and aim to continue to identify mis-priced securities, in what we believe is probably the least well-covered developed equity market, using our fundamental, forward-looking, bottom-up, and value-focused approach.

Disclosures

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.

This marketing communication is for Professional Investors only.