2023 rollercoaster ride ends with a strong year for developed equity markets

2023 was a head-spinning year for equities. After a strong start to the year, interest-rate induced fissures appeared in the global banking system with the collapse of several regional banks in the US, triggering recessionary fears and a rush for growth stocks on expectations that interest rates would shift lower. From March, market sentiment gradually recovered over the course of 2023 as macroeconomic data, against expectations, highlighted the underlying strength of the US economy, as well as the resilience of European economies in the face of ongoing energy price turmoil. The market first embraced the idea that the US Federal Reserve and other central banks might be able to increase interest rates without pushing their economies into recession and then, as year-end approached, given a potentially propitious combination of resilient growth and fading inflation, investors enthusiastically welcomed the possibility that the Fed might be in a position to cut rates sooner than had been previously expected. Exuberance returned once again, though it manifested itself slightly differently across markets and market segments.

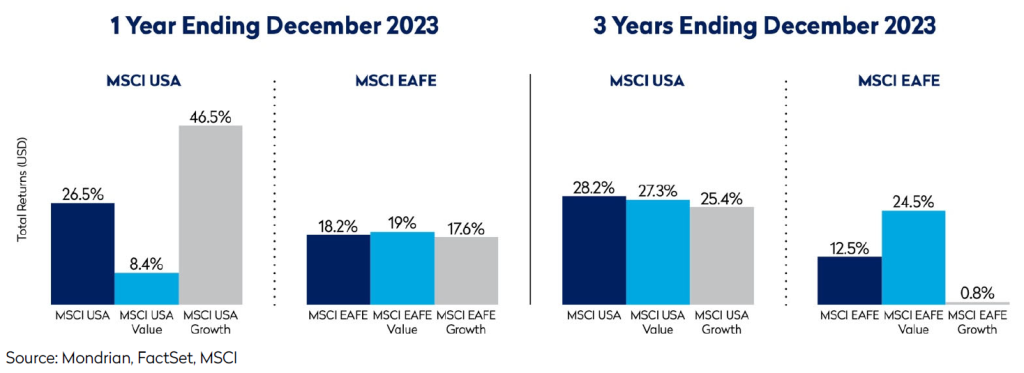

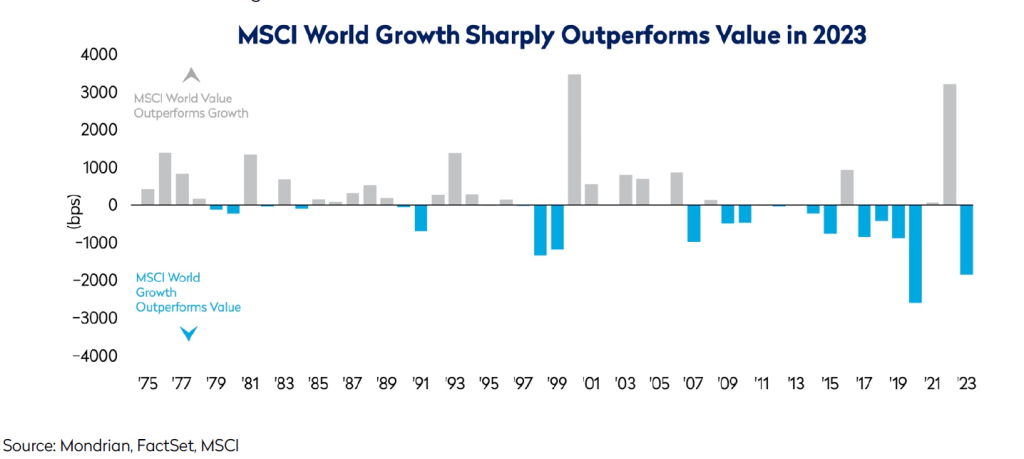

The US market led returns but as has been well documented, it was driven by the growth-oriented corners of the market and, in particular, the “Magnificent Seven.” As a result, MSCI World value equities lagged growth equities by over 25% – one of the widest periods of underperformance for the value style relative to growth since the inception of the MSCI style sub-indices in 1975, second only to 2020 when technology-related names benefited from one-off COVID earnings.

The Magnificent Seven are a group of US stocks including Nvidia, Apple, Microsoft, Amazon, Alphabet, Tesla and Meta Platforms.

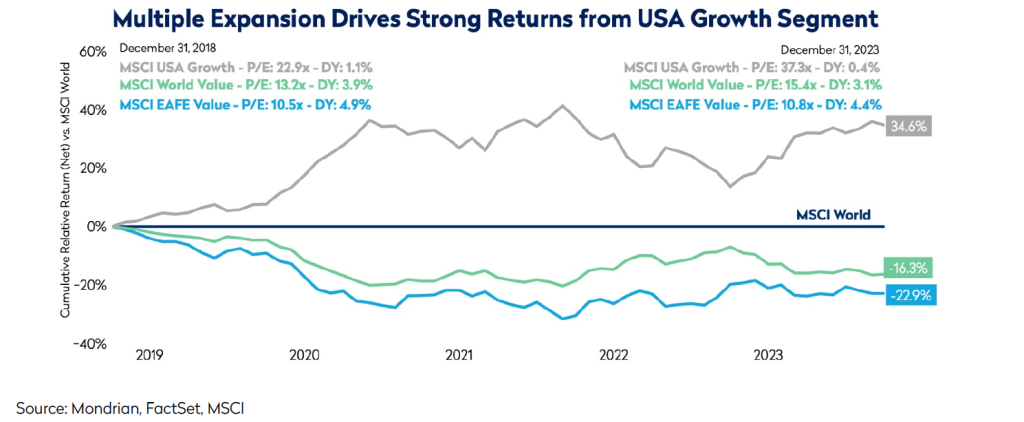

The super-sized impact of the large US technology stocks dominated MSCI World returns in 2023. Outside the US, we saw a different outcome with value-oriented equities outperforming their growth peers, supported by strong, relative and absolute earnings. As a result, despite strong returns, PE multiples for the EAFE Value remain low, having barely moved over the course of the year. While AI hype was a recurrent theme last year, the technology is still far from being a revenue or profit generator for most, if not all companies. Recent MSCI USA Growth outperformance has required significant multiple expansion, both last year (P/E multiples expanding from 28x to 37x) and over the past five years (23x to 37x). Rather than chasing hype, Mondrian continues to focus on the large universe of companies we have identified in more attractively valued segments of both the US and international markets, opportunities that we believe offer good long-term return potential.

Significant movements in bond yields create risks in the financial system

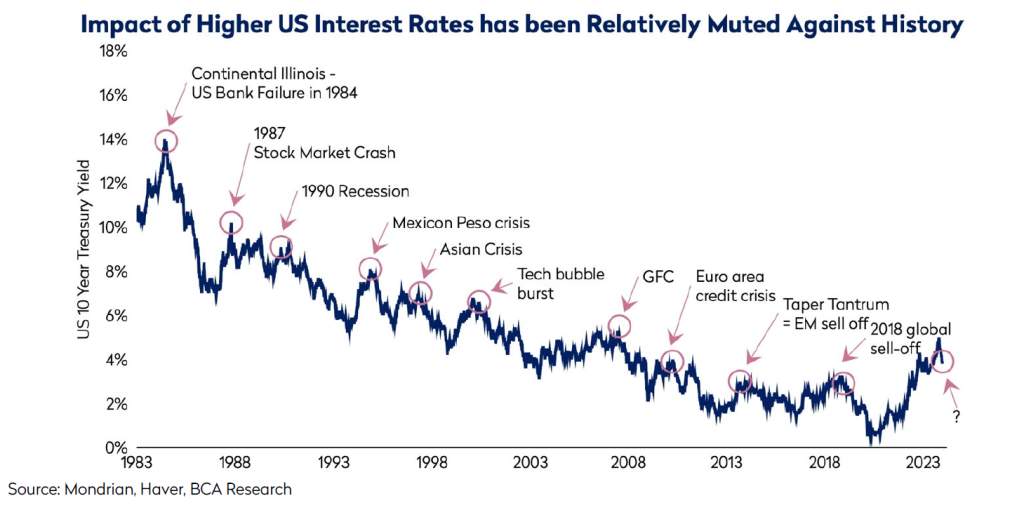

For decades, interest rates have been on a downward trajectory, punctuated by significant financial dislocating events when long bond yields rise significantly – as shown in the chart below.

This time, so far, has been different. After a shaky start to 2023, economies and equity markets finished the year on a positive note. Despite a sharp increase in interest rates in the past couple of years, the only significant casualties (SVB, Credit Suisse) in the first quarter of 2023 were well contained. The failed US banks had unique business models and a severe and abrupt withdrawal of deposits, coupled with unrealised losses on securities, portfolios, led to their demise. Nevertheless, given the magnitude of the increase in rates, it is likely significant tensions remain in the world’s financial system.

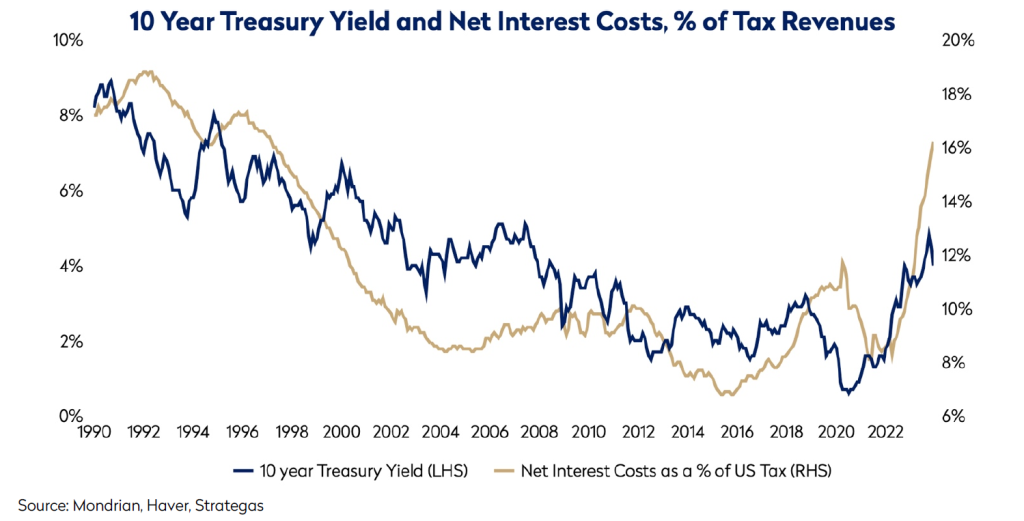

Government fiscal policy has played an important role in the global economy since the onset of the COVID-19 pandemic. Generous subsidies and handouts bolstered the balance sheets of US consumers, but these policy choices came at a cost to the balance sheet of the government. For years, debt servicing costs for the US government have declined, despite a higher volume of debt, but this trend has started to reverse. Approximately 50% of US government debt is due to mature in the next three years. With the current US weighted average cost of debt outstanding at a mere 1.9% and the US federal budget deficit – and refinancing needs – at record levels, US debt servicing costs are projected to remain high and likely grow. The political theatre of debt ceilings and shutdowns will likely intensify over the next few years. The US economy begins 2024 from a weak fiscal starting position.

US debt servicing costs continue to rise

Outside of the US, higher rates have flowed quickly into shorter duration markets such as mortgages in the UK or parts of Europe. Projects which were viable under the previous interest rate regime may no longer be profitable in the current interest rate environment. Many corporates (similar to governments) have benefited from years of declining financing costs. An economic and business scenario in which interest expense and leverage weigh on profitability would be a significant departure from the experience in the past decade. Many companies have locked-in lower rates, especially during the pandemic. In some cases, they are even enjoying higher returns on their cash balances, but this sweet spot will quickly pass; in time, interest costs will rise and that will weigh on profitability, capital investment, employment and shareholder returns. We are only beginning to see the impact of higher longer-term rates on corporate balance sheets globally as companies report their year-end results, while a lack of transparency may further mask the impact of the re-setting of rates in private equity markets. There could be a myriad of other possible risks lurking in the financial system.

Heightened geopolitical tensions increases the risks of negative surprises

2023 ended on a fairly grim note, with wars in Gaza and Ukraine still raging. Will 2024 be any better? Neither war appears to be getting better; neither may be easily contained. In the Pacific, presidential and parliamentary elections in Taiwan have taken place in January. Chinese President Xi Jinping has already made his thoughts on Taiwanese sovereignty clear, using his annual New Year’s Eve address to sound a warning to Taiwanese voters: Xi emphasized the “historical inevitability” of the “reunification” of China and Taiwan. China, which claims sovereignty over Taiwan, has not ruled out using force if Taipei refuses unification indefinitely. While the election outcome is unlikely to have any immediate impact, the future of Taiwan remains a source of instability that could be mined by disruptive actors.

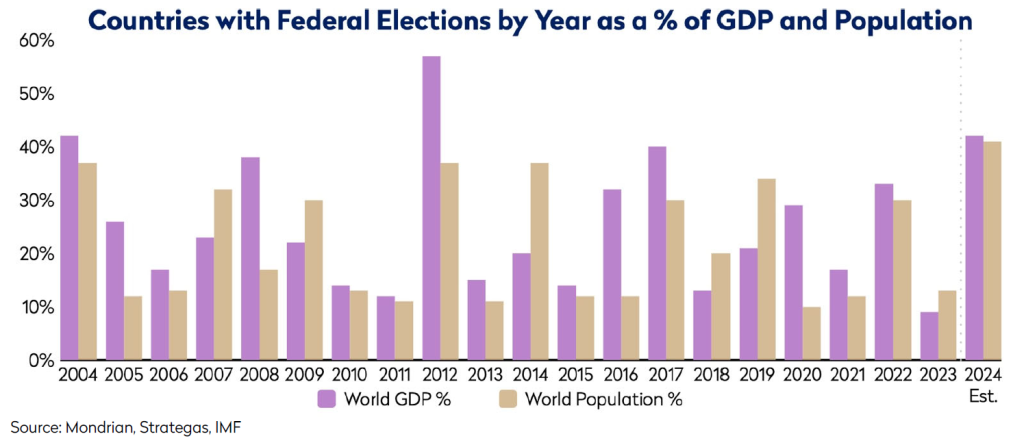

2024 – an unusually active political year – may well be testing for markets. The world is about to go to the ballot box: eight of the ten most populous countries, some 2bn people, are among the more than 70 states holding elections. This includes the core of the western world (US, EU and the UK). In addition, six countries that account for over 50% of the emerging markets index head to the polls: India, Korea, South Africa, Mexico, Indonesia, as well as Taiwan. Russia, too, will vote in a largely performative presidential election. Anointing Putin for another six-year term will set him on course to have been in power for longer than Stalin. 2024 will have 40% of the world’s GDP voting for a head of state (see the chart below).

If this does not quite equal the banner year of 2012, when both the US and China “chose” a leader, politics still has the potential to derail markets.

The 2020s have so far been something of a “disorderly decade”: in a short space of time, investors have had to deal with the pandemic, simmering tensions between the world’s two largest economies, Russia’s invasion of Ukraine and now war in the Middle East. Moreover, the US election this autumn, probably the single most important election, carries the possibility for further disorder in the form of a contested election with a disputed outcome, and a repeat of the civil turmoil seen four years ago. Given the muddled backdrop, it is unlikely that elections will provide markets with much clarity on the future global outlook. While markets have historically shrugged off most election results, the challenging geopolitical and fiscal issues governments face will continue to prove challenging to whoever is elected.

Despite strong market returns in 2023, public equities at the value end of the market continue to offer attractive long-term expected returns

Last year we wrote:

“Looking forward, one conundrum which we have been wrestling with in recent months is that for a universally forecasted recession, market earnings forecasts appear generally sanguine about the outlook for future corporate profits. We think one element of the explanation is that inflation will likely provide some support to nominal earnings even if earnings fall in real terms. Beyond that, we would caution that our analysis of market forecasts indicates that there is more undue optimism at the growth end of the market and, in contrast, much more realism in forecasts for the more value end of the market.”

Fortunately for investors, that “universally forecasted” recession never happened. For this, investors should be grateful. Equally, we should all probably worry, at least a little, that everyone now thinks a recession has been avoided.

Over the year, we have highlighted several areas of global markets that we continue to think are attractive for investors. International currencies are one; the yen continues to stand out as significantly undervalued against.

Most international currencies, in particular against the US dollar. We have also highlighted a number of companies in Japan which we believe are undervalued because of the low expectations investors hold for the market and the economy. While the market has outperformed in 2023, we continue to believe that high-quality global businesses with very strong operations are being under-priced because they are based in Japan. We also believe that they have a significant skew towards the upside as the Japanese corporate sector increasingly focuses on governance reforms and shareholder returns. While the recession never came, earnings, as outlined above, held up in Europe and Japan. As a result, valuation ratios remain attractive in EAFE, especially in the value segment where multiples are broadly unchanged despite the strength of the market over the past year. As one reference point, the EAFE Value sub-index trades on circa 10x forward earnings. We accept there is a good chance that consensus earnings are too bullish, because a “soft landing” is not assured and profit margins are somewhat high, but the starting point for valuations suggests that attractive absolute returns are possible even in a slightly more challenging macroeconomic environment. Within the growth segment in the US, multiples have expanded significantly and certain growth companies in the US now look very expensive. Nevertheless, we continue to identify many alpha-generating opportunities in the US. We continue to maintain our valuation discipline in this large and liquid market and invest in attractively valued names in our global equity portfolios.

We have highlighted the likelihood that 2024 could be a testing year for equity markets. We welcome that because we think that our investment approach offers a competitive advantage in complex times. First, we have a robust long-term, disciplined valuation framework. Second, while we try to anticipate how the future might develop, we do not rely on any single point forecast given the inherent uncertainty in markets and the widening range of possible scenarios in equity markets. The evaluation of stocks under different scenarios, and thinking about the skew of possible outcomes, has always been entirely central to our investment process and decision-making. We believe this structured scenario analysis framework, within a disciplined valuation methodology, will help us understand the likely distribution and skew of future returns and enable us to build portfolios that will support our clients in achieving strong risk-adjusted real returns in the long-term.

Disclosures

- This Investment Outlook may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

- Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice.

- Calculations for characteristics such as P/E, P/B, dividend yield, sector country allocations and market caps are based on generally accepted industry standards. Any characteristics referenced are based on a representative account from the Global Equity composite and derived by first calculating the characteristics for each security, and then calculating the weighted-average of these values. The details of exact calculations can be provided upon request.

- Characteristics including the likes of those listed in the above point are not reliable indicators of future results.

- All characteristic data provided is produced using Mondrian’s accounting system data.

- The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed.

- It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this outlook. Examples of securities will represent only small part of the overall portfolio and are used to illustrate our investment approach. Any holdings are subject to change and may not feature in any future portfolio. More information on holdings is available on request.

- Past performance is not indicative of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate, and you may not get back the amount you originally invested.

- Unless otherwise stated, all returns are in USD.

- All references to index returns assume the reinvestment of dividends after the deduction of withholding tax and approximate the minimum possible re-investment, unless the index is specifically described as a “Gross” index.

- Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing, or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages

(including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. - Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority (Firm Reference Number: 149507). Mondrian Investment Partners Limited is also registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).