Russia’s invasion of Ukraine

Vladimir Putin defied the West and, against hopes and many expectations, proceeded with the deplorable invasion of Ukraine on February 24th. This engendered an historic policy response. Severe sanctions against Russia and politically-connected individuals were coordinated globally. The Russian equity market remained closed for 19 business days, the ruble fell to all-time lows, though it has subsequently rebounded, oil surged to $130 per barrel and spot gas prices in Europe and Asia spiked to all-time highs. The invasion has shaken people around the world with camera footage and reports from Ukraine defying most modern day beliefs. As the fiduciaries of our clients’ assets, we have focused ourselves on the financial impact from this tragic war. Below we look at the various implications that are beginning to emerge.

Despite disruption and unprecedented sanctions, Russia is unlikely to be a systemic risk to the global financial system

Sanctions have been coordinated, severe, quickly executed and broad based. They targeted Russian banks, oligarchs, and various assets; they included restrictions over exports of technology to Russia and investment in new issuance of Russian sovereign debt and equity. Some Russian banks were removed from the SWIFT financial messaging system. Sanctions were also applied to Russia’s central bank, impacting the country’s $600+ billion of foreign currency reserves and potentially limiting Moscow’s longer-term ability to stabilize volatility in the ruble and economy. In response, the Russian central bank raised interest rates from 9.5% to 20% and imposed capital controls. The intention of the sanctions is to damage the Russian economy, with the hope that Putin will begin to lose support domestically, limiting his ability to continue with the war.

Russia is the 11th largest economy in the world (2021), but aside from trade in energy and materials, global linkages are not material. International financial exposure to Russia started to decline after the Crimean invasion and today that financial exposure, relative to the size of the global economy, is significantly less than it was 25 years ago when Russian market volatility was a contributing cause of the Long Term Capital Management (LTCM) collapse. This is mirrored in the exposures of global companies as well where despite political policies to try to integrate Russia into the world economy, revenues generated in Russia as a percent of MSCI World revenues are less than 1 percent. Mondrian international equity portfolio exposure outside the energy sector is of a similar magnitude.

Under strong central bank leadership Russia has so far avoided a sovereign default though it may only be a matter of time once sanctions bite; and the local stock market has now reopened. However significant restrictions still apply: foreigners cannot trade local securities, and ADRs/GDRs remain suspended. Any shares held by foreign investors are unable to be traded, and may be so for some time. Most Mondrian equity portfolios did not hold any Russian securities. Where a portfolio’s emerging markets exposure included a small exposure to the Russia, in line with index policy, securities are being priced at zero. We hope in time to be able to realize some value for these.

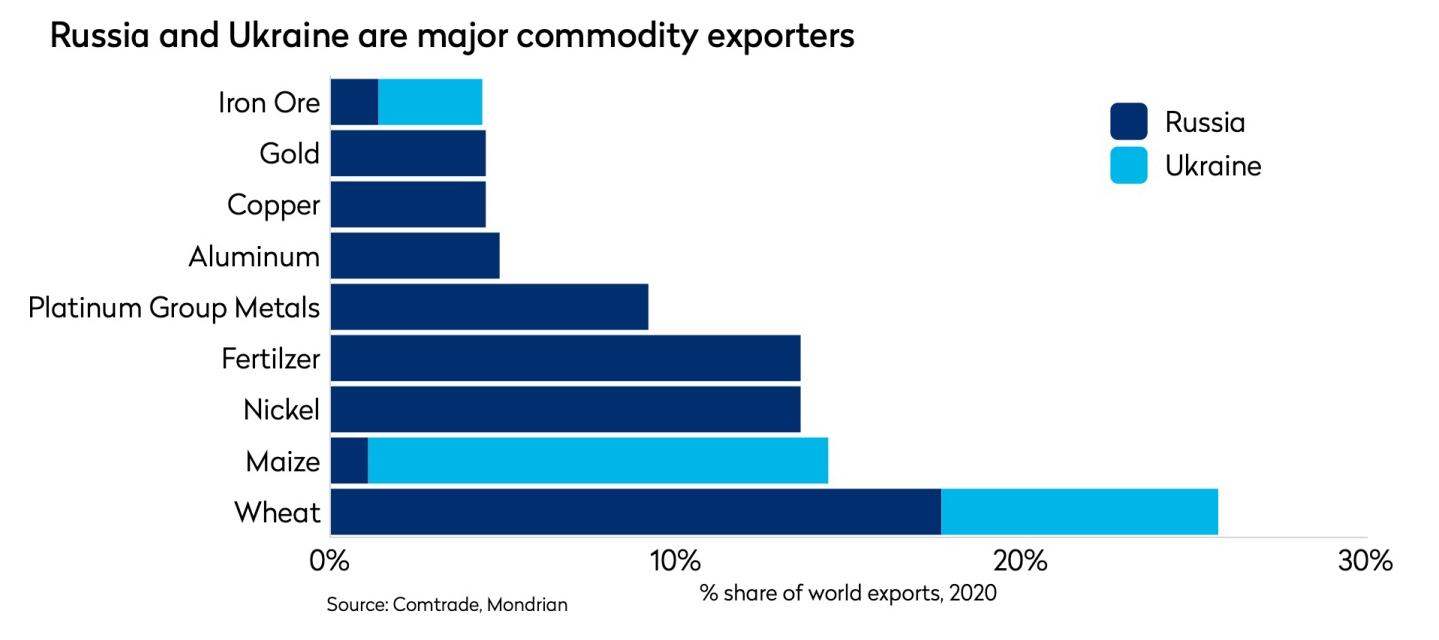

However Russia as a significant producer of energy and hard and soft commodities is systemically important in the real economy

Energy costs were already trending higher from the middle of last year and are now likely to stay elevated in the near-term with the Russian invasion: Russia is responsible for approximately 10% of global energy production. It is the third largest oil producer globally and the second largest producer of natural gas. While we expect that eventually most Russian oil will make its way onto the global market, the gas market is likely to remain at least partially disrupted as Europe searches for= alternative supplies. In the wake of the pandemic, the price of everything from semiconductors and baby formula to grains and steel had already shot up, forcing many central banks to begin a shift from trying to stimulate growth to fighting inflation. The war has now also damaged supplies of staple resources such as potash, neon gas and maize from Russia and Ukraine, worsening the inflation outlook. Most economists have now raised their inflation forecasts and lowered global growth forecasts for 2022. With the global economy already suffering from Covid–19 disruption and elevated levels of inflation, the commodity price shock as a result of the conflict has only served to exacerbate price rises and economic uncertainty.

Disruption in Russian gas supplies to Europe the biggest challenge; will lead to global gas markets evolving in the long-term

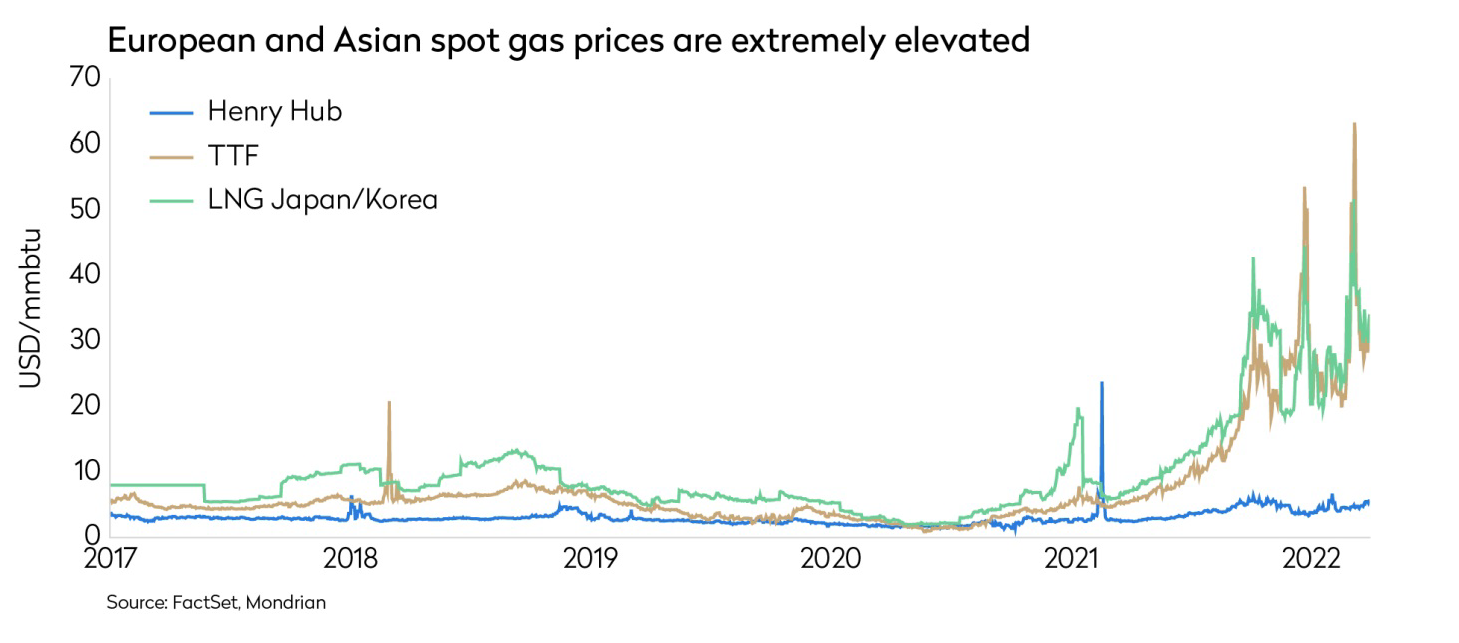

Russia currently supplies 170bcm of gas to Europe, approximately 30% of total European demand. While Europe has abruptly committed to replacing Russian gas over the medium term, this will require substantial new supply (most likely from the US, Qatar and North Africa), significant investment in LNG infrastructure, renewables and hydrogen and legal wrangling over existing multi-year purchase commitments. Resolving this structural challenge in Europe will be messy and take time; it will likely keep upward pressure on gas prices in the near-term.

Gas markets were historically based on long-term supply contracts with oil-linked prices. In recent years, European gas markets have evolved towards local hub-based spot gas prices as purchasers looked to take advantage of the growth in LNG and the availability of lower prices compared to oil-linked pricing. This dynamic abruptly collapsed last year, and Europe is now pushing up spot prices globally as it draws in supply to protect against a possible cut-off in Russian supply.

Russia had already reduced gas supply to Europe from the middle of last year as part of the now moot negotiations over Nordstream 2. European hub gas prices rose sharply from last summer (see chart). Given the current conflict, there is a lot of rhetoric and political pronouncements around sanctions and supply. The evolution of the debate from both sides is complex and will ultimately be driven by developments around Ukraine, but our conversations with industry participants and our understanding of political motivations indicate that it is unlikely to be in most participants’ long-term interest to see the abrupt cut-off of Russian gas supply to Europe. Russia needs the income and it doesn’t want to damage its long-term position as a supplier of gas to Europe while European governments are reluctant to risk a further cost of living squeeze from higher gas prices undermining the overwhelming popular support for Ukraine. While the politics remain volatile, assuming supply can continue, it is likely that over the near-term, European spot prices will stabilize around today’s higher levels, but well off the extremes of the past couple of months while European purchasers look to transition away from Russian gas and Russia looks for new customers.

As a growing producer and exporter of LNG, the US-based energy industry stands to benefit from the new export opportunities around the world. As the US takes advantage of these opportunities, longer-term this should create greater integration in global gas markets. In the near term, US markets which are well supplied with gas today will continue to have beneficial supply and prices, but in the longer-term, some industries reliant on gas as an input may feel a drag on their relative cost advantage as more local US gas is exported and regional hub prices show greater convergence.

In contrast in Asia, gas is still typically purchased on long-term oil-linked contracts and exposure to Russian-sourced gas, while having grown in recent years, is still much lower than in Europe. While the price of the approximately 30% of gas purchased at regional hub-based prices has moved up to global levels, prices of oil-linked purchases will rise more slowly over the next six months, giving Asian policymakers some unusual visibility on inflation evolution and cost-of-living pressures. While Japan and Korea, for example, will need to replace some Russian gas exposure, historically Asian contract gas prices have been high relative to other parts of the world. Longer-term, should the market transition into a new, more globally integrated market, Asia may find itself competing on a more level field with other regions.

The portfolio is overweight in Asia and is marginally overweight Europe. It does not hold material positions in the large European industrial and chemicals companies that are today dependent on Russian gas. It does however have a holding in Enel, a European utility which is a likely beneficiary of increased investment in renewables and alternative energy sources. We expect that pressure from the current crisis will mean that Europe continues to extend its competitive lead in this area.

The range of outcomes is very uncertain but increasingly skewed negatively

Market reaction to the Russian invasion has been relatively sanguine against the human, physical and economic destruction and disruption it has wrought. While bond yields have risen some to reflect the increased inflationary pressure and expectations of central bank action, global equity markets are now flat-to-up since the end of February. Swap and breakeven inflation rates only imply higher levels this year and next, then trending quickly back to long-term pre-pandemic levels.

We believe that underneath this calm exterior, the uncertainties are huge and the range of outcomes between our scenarios is widening. The world is starting from an ongoing Covid-disrupted economic position compounded by Russia’s importance in commodity markets and geo-politics. Significant uncertainty hangs over central bank policy and market valuations, and realistically disruption breeds more disruption so we have to believe there is a heightened risk of another “disruptive” event emerging. From this fragile position, when we look at the range of possible near and longer-term outcomes, we are comforted that our expected returns for most global equity markets exceed our 5% real hurdle rate. However, we also have to believe that the chance of something going badly wrong has risen while a better than “base” case outcome has a decreasing and low probability. While we have highlighted the growing risks within the system for some time now, the accumulated risks are increasingly challenging high valuations as a potential threat to future long-term real returns.

Real Returns: Japan presents a contrarian opportunity

In a world of high inflation, tightening monetary policy, negative real yields in bond markets, high property prices and expensive equity valuations, searching for real return is challenging. While we don’t have any magic bullets, other than to logically (at least it seems to us) suggest that investors should focus on areas of the market where valuations are depressed such as value-oriented equities, we have noted one striking conundrum. In the recent market uncertainty, the yen has stood out for not acting (as it historically has) as a safe haven. While there are many reasons that can be posited for the yen’s weakness – rising global interest rates, high oil prices, risk of a cyclical slowdown – it is strange to us that, if investors want real returns, why wouldn’t they start with areas of the market where there is low inflation? In currency markets, relative low inflation means increased competitiveness and an increase in underlying real value. However the yen is now one of the most undervalued currencies globally based on Mondrian’s purchasing power parity (PPP) analysis. Japan is experiencing one of the lowest rates of inflation in the developed world. The government is able to maintain low interest rates because debt is domestically financed. While recent high gas prices have pushed the country into a current account deficit, this is unlikely to hold over the long-term. We are surprised that as the market focusses on the possibilities of higher interest rates elsewhere, it is ignoring the competitive, economic benefits of a lower yen exchange rate. Select opportunities for real returns can exist in forgotten areas of the market.

Disclosures

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.