There has been renewed interest in frontier markets as global bond yields remain low and the continued search for yield widens to evermore niche asset classes. Interest in frontier markets first peaked prior to the Great Financial Crisis (GFC) of 2008 and then in the aftermath of the Eurozone crisis of 2011/12 as global yields plunged. Value opportunities within frontier local bond markets can arise, but due to these markets being small and highly illiquid we apply a higher hurdle than other emerging markets before investing in them to reflect the liquidity premium and higher currency volatility.

What is a Frontier Market?

A frontier market is typically a developing country with a small or underdeveloped local bond market. With few sources of internal demand for its local debt (such as local corporates or domestic pension funds) it may have issued debt in US dollars (or other hard currency such as Euros or Yen) as the primary source of financing budget deficits. Because most frontier markets are usually found lower down the credit quality spectrum, yields are often higher than more developed markets, partly to attract global investors and partly due to many of these countries having weak macroeconomic foundations such as high inflation, weak levels of foreign reserves and low income per capita. In addition, given frontier markets are typically small, the higher yield also reflects a liquidity premium and many of the bonds are highly illiquid. Further, because many frontier markets are also likely to have poor environmental, social and governance (ESG) credentials they are more prone to idiosyncratic risk, which of course can be both beneficial (in terms of having low correlation with other markets and thus enhanced diversification benefits) as well as detrimental.

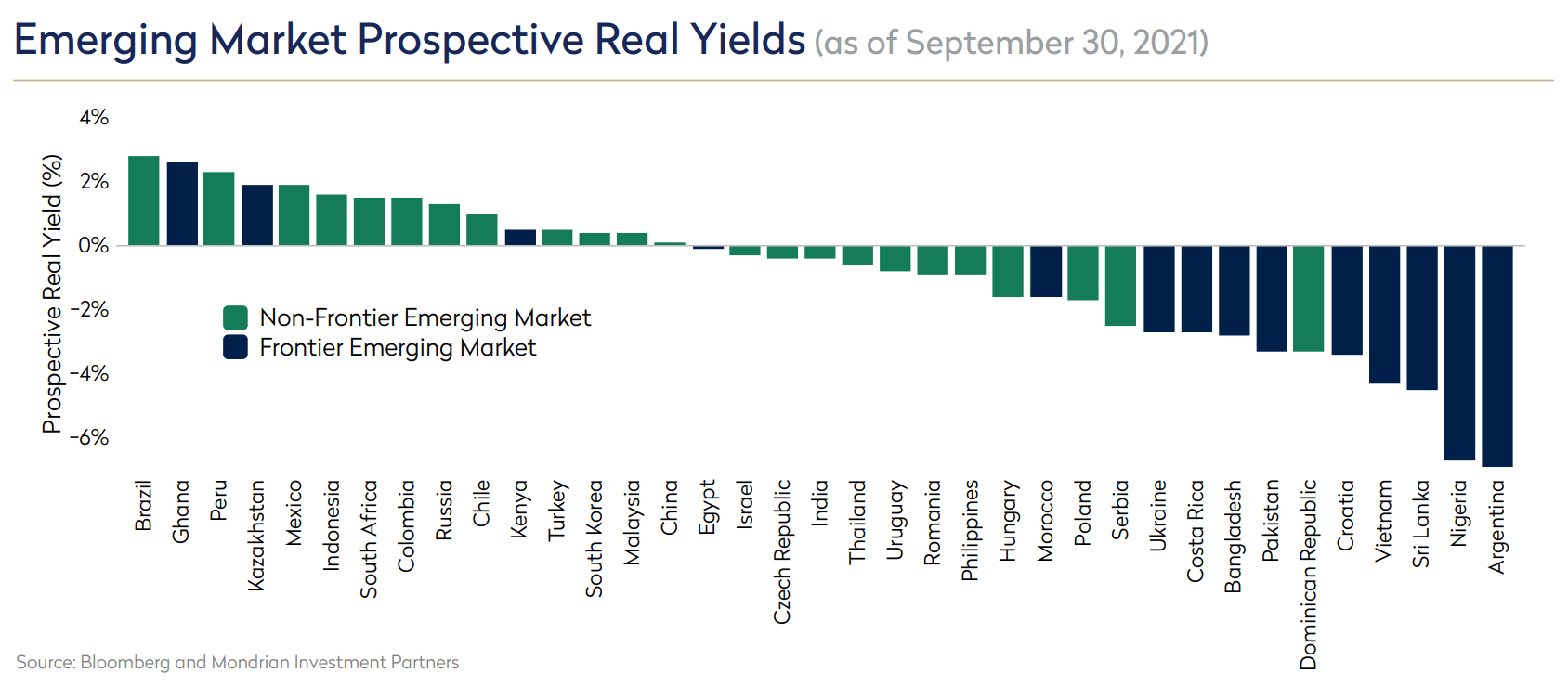

The Mondrian approach to fixed income management is to provide investors with a diversified portfolio of bonds that overweights those markets that possess the highest Prospective Real Yields (PRYs). In other words, those markets which have a nominal yield that best compensates investors for both inflation and sovereign credit risk. Mondrian’s proprietary sovereign credit risk assessment follows a disciplined process, incorporating a range of factors including environmental, social and governance (ESG). Although we look at similar factors to external rating agencies, the nature of our approach allows us to be nimble, identifying a change in sovereign credit risk as it is occurring. The following chart shows that when emerging markets are ranked in terms of their PRYs, frontier markets appear towards the lower end.

Currency Risk within Frontier Markets

Currency risk is a very important consideration for frontier markets. Many frontier markets operate some form of capital control on currency movements either to prevent excessive currency volatility or to maintain a peg against another currency. This can sometimes mean capital becoming trapped within a market for periods of time, the likelihood of this occurring being increased during periods of market stress. Furthermore, given the small size of these markets, they can be overwhelmed by international capital flows leading their currencies to become increasingly volatile. This was especially the case in the GFC (2008) and taper tantrum episode of 2013. For those frontier markets which maintain a peg or are managed against other currencies, these capital flows can have a destabilizing impact, especially where the peg or level against which the currency is managed against becomes divorced from economic fundamentals or the economy is subject to an idiosyncratic shock, leading to a break in the peg or sudden devaluation in the currency.

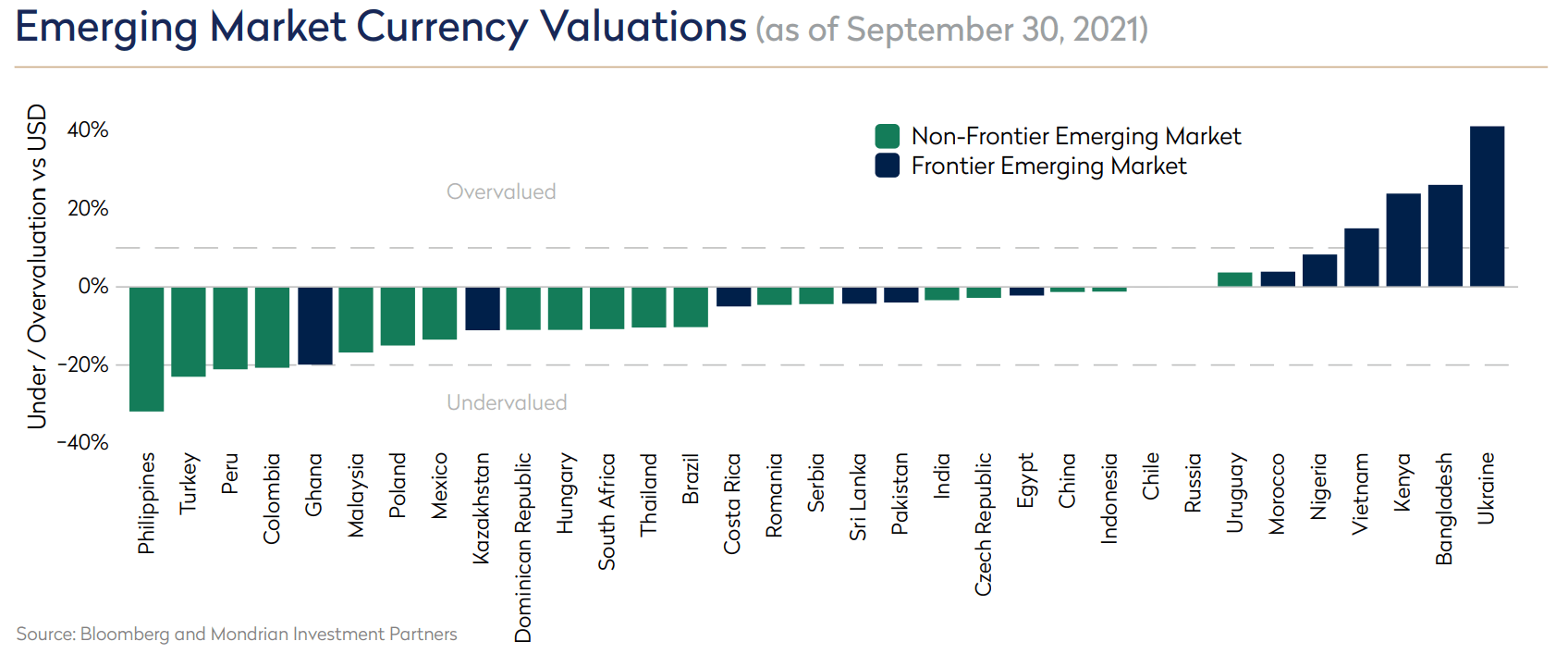

Currency is another key strand of the Mondrian fixed income investment process; we consider FX valuations using our own proprietary Purchasing Power Parity (PPP) valuation and modify currency exposures accordingly by hedging exposure to those currencies we deem to be expensive and increasing exposure to those that we deem cheap. As we can see below, frontier market currencies appear more expensive when emerging and frontier market currencies are ranked from most undervalued against the US dollar to least undervalued based on our PPP currency valuations. Furthermore, given the highly illiquid nature of frontier markets, we apply a higher threshold of undervaluation before investing in them to reflect the liquidity premium.

Conclusion

We find that currently there is better value to be found in non-frontier markets. Nominal yields in many frontier markets simply do not compensate for inflation risk or sovereign credit risks, with high nominal yields reflecting high inflation and/ or high sovereign credit risks. We also find that there is better value in non-frontier market currencies with frontier markets appearing at the more expensive end of the spectrum. Overall, we find that better value opportunities are to be found in non-frontier emerging markets. However, we continue to monitor frontier and non-frontier local bond markets and currencies for value opportunities and will invest in these markets if the value is there.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views.

Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. All information is subject to change without notice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward- looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements. The material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate. There can be no assurance that the investment objectives of the strategy will be achieved. This document is solely owned by and the intellectual property of Mondrian Investment Partners Limited. It may not be reproduced either in whole, or in part, without the written permission of Mondrian Investment Partners Limited.