Korea’s Value-up Opportunity

Korea is home to some of the world’s leading and most innovative companies. Samsung Electronics is the world’s leading memory semiconductor and smartphone maker. SK Hynix is pioneering High Bandwidth Memory for Nvidia’s AI chips. Hyundai Motor and Kia have emerged as two of the most competitive automakers in the world, now accounting for approximately 9% of all cars sold globally, while LG Chem is one of the world’s leading battery makers for electric vehicles. Yet despite the underlying strength of many of its largest listed companies, the Korean stock market has not displayed anything close to world leading performance, instead trading at a persistent and steep discount to other emerging markets. The reason often cited to explain the Korean discount is poor corporate governance, which takes shape in a few forms, but is widely accepted as not meeting global standards. Fortunately, it seems that the Korean government has finally taken note of this, and in a nod to the turnaround of the Japanese stock markets fortunes that followed a focus on improving corporate governance, the Koreans have now embarked on their own value up program.

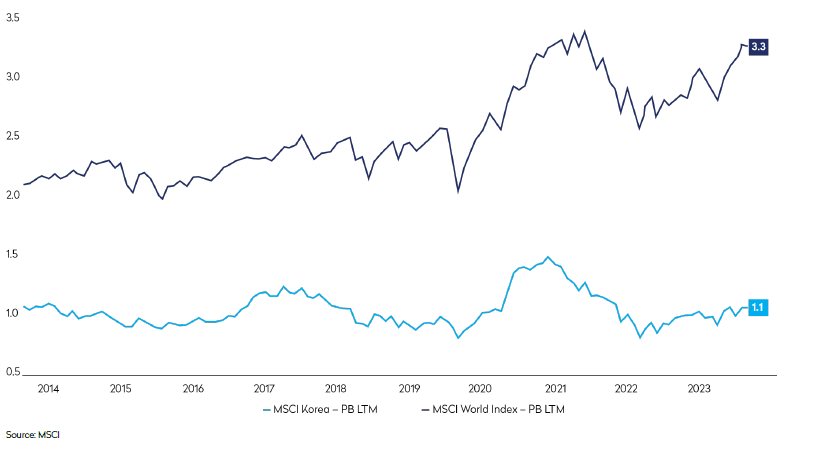

Korea’s P/B discount to MSCI World – Last 10 years

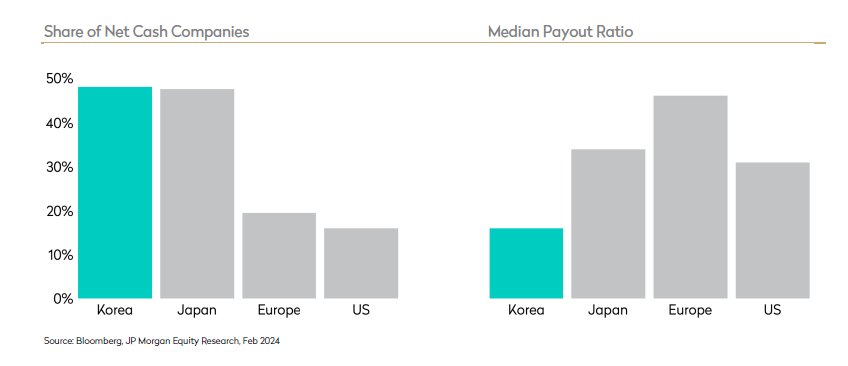

As can be seen above, Korea trades on a Price to Book (PB) ratio of 1.1x, a 66% discount to the MSCI World PB ratio of 3.3x. Part of the reason for this discount is poor corporate governance, while some can be attributed to the low Return on Equity (ROE) earned by many companies. However, in reality, low ROEs are also attributable in part to governance factors, with the equity base of Korea’s Chaebol groups bloated by cross shareholdings. Furthermore, these cross shareholdings fuel investor scepticism over alignment between founding family interests and those of minority shareholders and provide an incentive to retain capital within the group. For this reason, the Korean market has historically offered weak shareholder remuneration policies compared to global norms. That said, the direction of travel in this area has been somewhat positive over several years now, although clearly not at the pace investors, or Mondrian would have like to have seen. As can be seen below there is ample room for dividend payout ratios to grow in Korea.

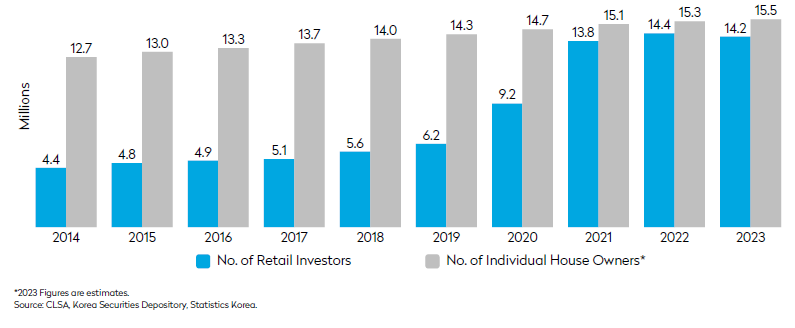

While these structural factors can explain the past behaviour of Korean corporates and the related valuation discount, Korea’s increasingly pressing demographic issues may now create a catalyst for change. Korea has one of the most challenging demographic profiles of any country, which will inevitably create a significant taxation burden on the younger generation. As in Japan, the government therefore needs to implement policies to revitalise the economy and support rising real incomes. In this respect, having a robust stock market which provides consistent investment returns could be a key component to drive wealth creation. Arguably, this need has existed for many years, over which time we have seen little government focus on stimulating shifts in the equity market. However, another important factor is that retail ownership of the stock market has increased almost threefold since the pre-Covid era, with retail investors now rivalling the number of homeowners. Prior to this change, Korean voters’ attitudes to the stock market were apathetic at best, with many seeing equity holdings and dividend income as the exclusive preserve of the privileged few. This dynamic meant that policies focused on improving market returns offered little prospective political advantage. With much wider stock ownership, arguably both the incentive to improve market practices, and the political leeway to do so have never been greater.

Number of Retail Investors Now Close to Number of Homeowners in Korea

The recent experience in Japan demonstrates how reform can provide a powerful driver for stock market performance, as well as how such reforms could be achieved. Like Korea, the Japanese stock market has long suffered from a valuation discount attributed to poor governance and capital allocation practices. In Japan, the Kishida administration has recently been pursuing corporate governance reforms, believing that a clearer focus on long-term value creation can invigorate corporations, and that a long-term rise in stock prices can turn individual tax-free equity investment accounts into a stable source of financial income. Hiromi Yamaji took over as CEO of the Japan Exchange Group, which owns the Tokyo Stock Exchange (TSE), in April 2023 and wasted no time in seeking to drive reform. The TSE subsequently wrote letters to all Japanese companies asking them to explain their return on capital relative to cost of capital; to update this annually with improvement plans; and to facilitate better dialogue with shareholders. The request that management teams be more aware of the cost of capital and stock prices may seem basic to global investors, but it was significant in Japan where many companies still focused primarily on P&L performance. Since April 2023, the Japanese stock market is up over 40% in local terms. This is likely at least in some reasonable degree due to governance enhancements already made, and the prospect of continued improvements to shareholder returns.

The Korean’s have clearly taken note of their neighbor’s actions and intent. In February, the government, through the Financial Services Commission (FSC) provided guidelines for its own ‘Value-up’ program. At this stage, we only know the outlines of reform initiatives, with tangible implementation yet to come. The tone though is clear. FSC Chairman Kim Joohyun stated the key pillars as follows – establishing a fair and transparent market order, improving accessibility to capital markets, and strengthening protection for shareholders. The idea being he said was ‘….to provide a positive feedback loop in our capital markets where listed companies are able to get a proper valuation for sound growth and investors are able to share the profit of that growth….’.

Investors have reacted to this concerted policy effort quickly and positively. Areas which are expected to be the mostly likely beneficiaries of tangible policy when it comes through are those which (i) trade at low price to book multiples in absolute terms or vs. global peers – for example many cyclical sectors including autos, and (ii) where the government has direct influence through ownership – SOEs, or indirectly through regulators – financials. Many stocks in these areas have already moved up notably this year in anticipation of the benefits to come.

While it is tempting for outside investors to see the result of change in Japan, and draw parallels to Korea, it would be a mistake to do so blindly, without consideration of important differences between the two markets. One of these is the ownership structure of many Chaebol groups, where controlling families have significant stakes which they intend to pass down to the next generation, in turn creating a disincentive to see higher share prices given Korea’s very high inheritance tax rate. While in Japan the mere directive from the stock exchange to make improvements was apparently sufficient to effect change, it is doubtful whether government persuasion alone will be sufficient in Korea, at least for Chaebol groups. To achieve lasting results, the two most important areas will be tax reform, and measures which enshrine clear legal protection of minority shareholders. By lowering inheritance tax rates or deferring its payment until stakes are sold, corporates could be incentivised to simplify their governance structures and align interest with minority shareholders. A constructive set of policies on these two issues will be critical in persuading investors of the sustainability of the momentum seen in Q1. Hence the upcoming election in April and the hoped for re-election of the incumbent Yoon government is the next important step the market will watch closely. If re-elected, the expectation is that in May, there will be an announcement elaborating on dividend taxation which many, including Mondrian, believe is the key ingredient to encourage Korean corporates to improve dividend policies and unlock value.

Over the years, the persistent and deep discount on Korean companies has attracted many value investors, including Mondrian, with mixed success. A meaningful shift in dividend culture needs to be the link to efficient value transfer to minority shareholders. We are overweight Korea, with exposure across a range of sectors. This positioning is not reliant, or based on meaningful “value up” catalysts; rather the value of the underlying businesses and a mild improvement in shareholder return over the long term where we are already seeing signs of improvement from some of our portfolio companies. We have taken some profits this year on the back of strong price performance in financials, telecoms, and IT, as a positive outcome from value up initiatives remains uncertain. For a rally to be sustained in the way we have seen in Japan, we would need to witness positive and concrete developments relating to dividend taxation and further commitments from the newly elected government that the value up program remains a priority. If so, after many false dawns, Korean stocks could finally deliver the performance the quality of their businesses arguably warrant.

Disclosures

- This marketing communication is for Professional Investors only.

- This Investment Outlook may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results or performance to differ materially from those reflected in such forward-looking statements.

- Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. Views should not be considered a recommendation to buy, hold or sell any security and should not be relied on as research or investment advice.

- Calculations for characteristics such as P/E, P/B, dividend yield, sector country allocations and market caps are based on generally accepted industry standards. Any characteristics referenced are based on a representative account from the Emerging Markets Equity composite and derived by first calculating the characteristics for each security, and then calculating the weighted-average of these values. The details of exact calculations can be provided upon request.

- Characteristics including the likes of those listed in the above point are not reliable indicators of future results.

- All characteristic data provided is produced using Mondrian’s accounting system data.

- The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed.

- It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this outlook. Examples of securities will represent only small part of the overall portfolio and are used to illustrate our investment approach. Any holdings are subject to change and may not feature in any future portfolio. More information on holdings is available on request.Past performance is not indicative of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate, and you may not get back the amount you originally invested.

- Unless otherwise stated, all returns are in USD.

- All references to index returns assume the reinvestment of dividends after the deduction of withholding tax and approximate the minimum possible re-investment, unless the index is specifically described as a “Gross” index

- Mondrian Investment Partners Limited is authorized and regulated by the Financial Conduct Authority (Firm Reference Number: 149507). Mondrian Investment Partners Limited is also registered as an Investment Adviser with the Securities and Exchange Commission (registration does not imply any level of skills or training).