Artificial Intelligence, IT and Emerging Markets

The theme which has overwhelmingly captivated markets this year is Artificial Intelligence, or AI. Since the public launch of the Chat GPT application by OpenAI late last year, the impressive way large language model algorithms appear to have achieved a quantum leap in “intelligence”, has spurred a flurry of further activity in the industry. With OpenAI backed by Microsoft, rival tech behemoths have rushed to launch competing versions of the technology to assuage investor concern that they might be left behind in this developing trend. Adoption has broadened much further than this however, with developers rapidly publishing applications beyond chatbots on OpenAI’s platform in the same manner as, but much more quickly than they did for the App Store when it was launched 15 years ago. These applications for Generative AI address the full gamut of technological, financial, and artistic disciplines, and once again highlight to us how the technology sector is one of the clear long term structural growth areas in the world today, driven by innovation.

Of course, this excitement quickly fed through into financial markets, and it seemed that any company which could demonstrate a tangential connection to AI enjoyed a strong increase in its stock price. While it typically pays to approach new technological themes that suddenly cause sharp moves in stock prices with some skepticism, it would equally be churlish to deny that there hasn’t been a meaningful development in the industry. As a result, significant sums are being invested, which will likely result in material improvements to how multiple industries operate.

Thus far, the clear beneficiary of these investments is US company NVIDIA, which is proving to be the classic “picks and shovel” play on Generative AI, as its H100 chip enjoys a dominant position with AI training servers. NVIDIA’s stock has seen breath-taking gains off the back of raised guidance, up 189% in the year to end June 2023. It is worth pointing out though, that the development of AI is also an area of comparative advantage for the Emerging Market asset class. (There may be risks to China given current limited access to high end AI chips which we are of course cognizant of, but don’t intend to elaborate on here).

There are several Emerging Market technology companies that are integral to high end AI training server production, not least TSMC, without whose advanced manufacturing platform, NVIDIA’s H100 chip could simply not be produced. It is expected that NVIDIA will gradually see increased competition for the H100, but it is likely that TSMC will produce some or all those competitor chips. TSMC itself may see competition over time, but the most likely competitor for advanced node foundry is another emerging market company – Samsung Electronics. In a similar manner, the H100 requires specialized High Bandwidth Memory (HBM), for which SK Hynix – yet another emerging market company – is currently the only producer qualified to supply NVIDIA. The likely next producer to supply HBM? Again, its Samsung.

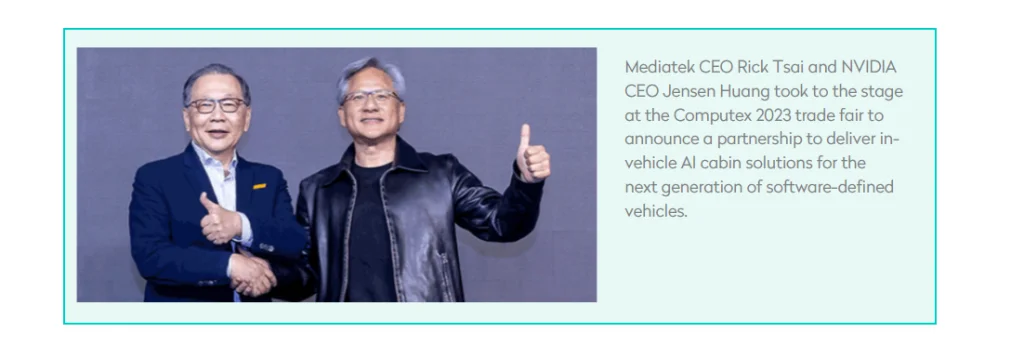

Of course, NVIDIA has a much more direct exposure to Generative AI than the emerging markets companies discussed, which have also seen good share price performance recently, albeit from a depressed starting point given the semiconductor downcycle of 2022. Nevertheless, the quantum of investment going into the infrastructure needed to train and deploy AI algorithms will create growth opportunities for many other companies, although in a more diluted manner than for NVIDIA. While NVIDIA currently dominates the market for chips used to train AI algorithms, chip designers such as Taiwan’s Mediatek are likely to leverage their advanced design capabilities to win projects for the specialized Application Specific Integrated Circuits (or ASICs) that are typically used to deploy AI algorithms. Mediatek already deploys some AI functionality in their own smartphone chips, chiefly to improve the quality of images taken by their smartphone cameras. Indeed, Mediatek recently agreed to collaborate with NVIDIA on the development of onboard AI solutions for the automotive sector (see photo below). Meanwhile, Taiwanese companies such as Hon Hai Precision, Quanta Computer and Wistron dominate the market for server design and assembly, while other Taiwanese companies dominate the supply of the myriad components used in servers and data centers. Many of these companies are suppliers to NVIDIA and will benefit from a broadening out of investment in AI as other companies seek to join the fray.

The dominance of many of the critical technologies required to deliver AI therefore represents a clear area of comparative advantage for the Emerging Markets universe today. Moreover, the commanding position of Taiwanese and Korean companies within the supply chains for semiconductors and technology hardware – built over decades – represents a durable competitive advantage that has tended to keep many of these companies on the right side of repeated disruptive trends in technology. Although NVIDIA and generative AI are in focus today, TSMC has been the foundry of choice in several new waves of investment and innovation, whether for Smartphone Application Processors, ARM based CPUs or Cryptocurrency Mining chips due to its combination of advanced technology and reliability. In a similar manner, each of this century’s big technology adoption cycles – from Smartphones to different wireless standards within Smartphones, to the roll-out of server and cloud computing – have all tended to lead to increased demand for memory, benefitting the oligopolistic industry, which is dominated by three companies, two of which are Korean. AI appears no different to these previous investment cycles. Of course, the rising interest in AI will disrupt and displace certain other areas of technology investment and thereby create net losers as well as beneficiaries. On balance though, we believe this is a net benefit for many of the leading companies that are well represented in the Emerging Markets index and our portfolio.

The technology sector is often perceived as challenging for value investors for a combination of both good and bad reasons. One of the better reasons is that the fast paced and disruptive nature of the industry makes it more difficult to have confidence in earnings durability across cycles, and this we agree applies to a significant proportion of the sector. For the companies discussed above though, we believe the comparative advantage described allays this concern, and the companies have proven the robustness of their returns to both new technologies and competitive threats.

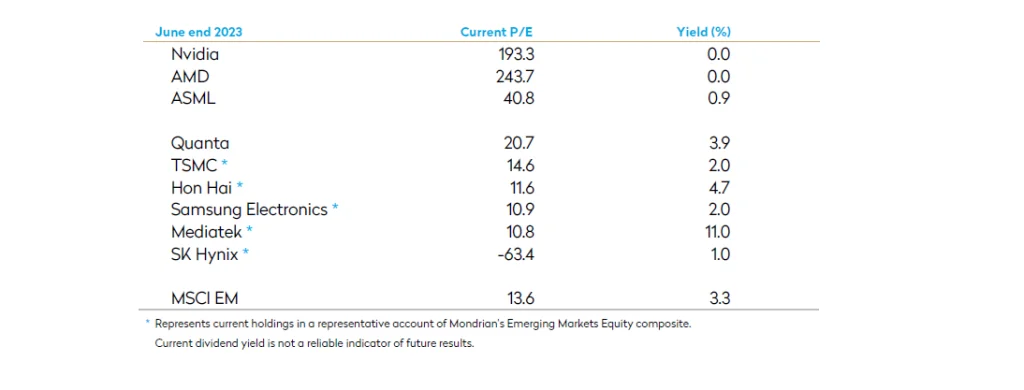

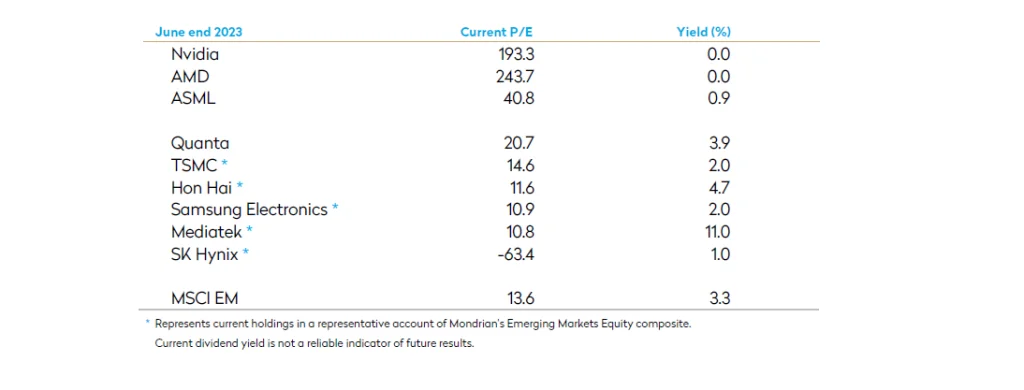

Despite being disciplined value investors, we have been overweight IT for some time and remain so today. We have argued that we are able to access a wide range of leading companies that exhibit the rare attraction of both sustainable long-term growth with strong balance sheets and ample shareholder returns; whilst trading at attractively valued stock prices. NVIDIA wouldn’t pass our valuation hurdle, but many in Taiwan and Korea in particular do, see below.

P/E Ratio and Dividend Yields for Select AI Exposed Stocks

Developed market stocks at large premium to EM names.

The technology sector has posted strong returns this quarter, and we have maintained our discipline by trimming areas of strength. We nonetheless maintain a healthy exposure to some of the companies mentioned, as we believe the long-term valuations and outlooks remain attractive, particularly when compared to some pockets of the semiconductor space in developed markets.

Disclosures

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed, and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Examples of securities will represent only a small part of the overall portfolio and are used to illustrate our investment approach.

Holdings are subject to change and may not feature in any future portfolio. More information on holdings is available on request. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.