Emerging Markets Investment Outlook

The start of the year brought with it renewed optimism about Emerging Markets (EM), given the re-opening of China’s economy. However, markets retraced somewhat as the geopolitical backdrop remained challenging with renewed tensions between the US and China, and no end in sight to the war in Ukraine. Separately the collapse of Silicon Valley Bank (SVB) in March (the second largest banking failure in US history) lead to a widespread loss of confidence in US and European banks, and a major sell-off in the developed market financial sector. On the inflation front, headline inflation continued to ease over the quarter on the back of low energy prices, but core inflation generally remained stickier, forcing global central banks to tighten monetary policy further, with US rates reaching their highest level since 2007 in March. EM posted positive returns over the quarter but lagged the MSCI World Index.

China

Chinese shares achieved robust gains at the start of the quarter after Beijing loosened the Covid-19 restrictions that had constrained the country’s economic growth. Supportive property market measures and a loosening of the regulatory crackdown on China’s technology companies also bolstered investor sentiment. Unlike much of the developed world, inflation has thus far remained low with February’s CPI print below expectations, rising only 1% year on year, allowing the People’s Bank of China (PBOC) to maintain an easing monetary policy. The PBOC announced a 25bps cut to its reserve requirement ratio for banks in March, which was earlier than expected.

The Mondrian portfolio benefited from positioning in China, as it did in the last quarter of 2022. As we enter the second quarter, we expect China’s economy to continue to be supported by its Covid reopening. Nevertheless, we took advantage of the market rally to reduce our overall allocation to the market. We sold Yum China, and took money out of Tencent, Baidu, NetEase and Zijin Mining after strong performance resulted in less attractive risk-adjusted valuations. Our overweight to China is now below 5%, compared to close to 9% at its highest level last year.

Mean Reversion

As value investors, we regularly scour the market looking for opportunities among the laggards. Being contrarian and not following the herd is often important in emerging markets where sentiment can change so quickly causing markets to reverse course with little warning. Mean reversion was clearly on display during Q1, as many of 2022’s best performing markets and sectors were the worst at the start of 2023, and vice versa. This helped Mondrian’s relative performance during the quarter.

We had already benefited from China’s reversal at the end of 2022 and this continued to some degree in Q1. Taiwan (+14.8%) and Korea (+9.6%) outperformed to a greater extent; we are overweight, given cheap valuations post last year’s sell down. Conversely, our underweight markets fared poorly, as India fell 6.4% and the Middle Eastern countries fell 2%. India generated negative returns amid allegations of fraud and share price manipulation at a major conglomerate, Adani, early in the quarter. Economic data released over the period was also below consensus, highlighting how careful investors need to be of areas in EM that become very highly regarded and bid up.

This divergence in performance created an opportunity to make an investment in Saudi Arabia towards the end of the quarter, whilst also increasing our position in India. However, we remain underweight both areas as valuations are less compelling versus the broader market.

Brazil was down in dollar terms against a backdrop of softening economic data and anti-government riots that damaged government buildings in January. Brazil is a significant underperformer over 1 year now and we have been adding to our positions there, moving to a larger overweight given attractive valuations. We think it is a reasonable expectation for Brazil to mean revert in the not too distant future.

Sectors told a similar story. IT (+14.7%) and Communication services (+12.6%) were the best performers having been the worst in 2022. Utilities was the best sector last year but was the worst in Q1, down 10.5%. Our positioning in all three areas added value.

Financials and Outlook

In March, the collapse of SVB and broader concerns around the financial sector hit bank shares hard, while government bonds rallied.

The EM financials sector only fell 1% and while it is very difficult to definitively rule out any similar problems within the asset class, thus far, EM banks have been relatively resilient. The majority of EM economies haven’t followed such an extreme interest rate path as the US and Europe over the last few years, while inflation in many countries, especially in Asia and the Middle East has remained reasonably low.

The recent banking sector events in the developed world especially are likely to lead to a further tightening of bank lending standards, which could further slow growth in developed economies, possibly leading to a moderate recession over the course of the year. However, with little evidence of extreme excess in the real economy and with better capitalized banks, a repeat of 2008 seems unlikely, while EM financials should be less vulnerable.

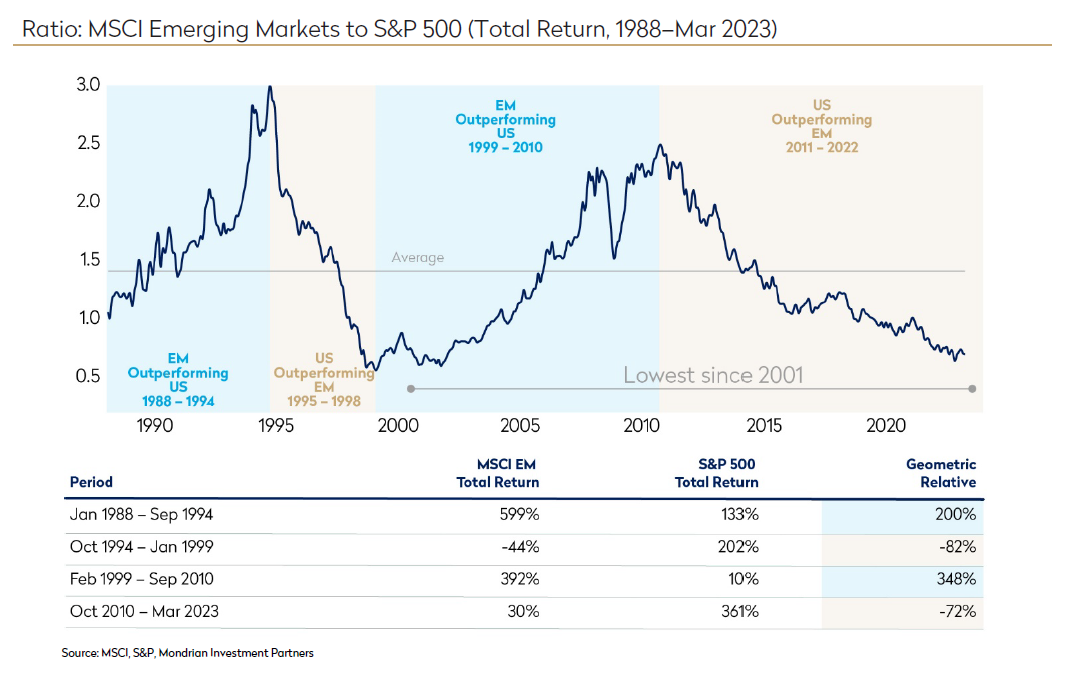

At this stage, one can say there are considerable uncertainties – in both directions – over the extent to which the recent turmoil will affect sentiment and activity. This uncertain backdrop argues against extreme positioning between or within asset classes but should bode well for emerging market equities when compared with US equities. US equities remain a large outperformer against EM equities (see chart below), with valuations at a steep discount. If EM can avoid the kind of blow-ups we just witnessed in the developed world financial system, the probability of mean reversion in favor of EM becomes surely ever greater.

Disclosures

This marketing communication is for Professional Investors only.

Views expressed were current as of the date indicated, are subject to change, and may not reflect current views. All information is subject to change without notice. Views should not be considered a recommendation to buy, hold or sell any investment and should not be relied on as research or advice.

This document may include forward-looking statements. All statements other than statements of historical facts are forward-looking statements (including words such as “believe,” “estimate,” “anticipate,” “may,” “will,” “should,” “expect”). Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Various factors could cause actual results to differ materially from those reflected in such forward-looking statements.

This material is for informational purposes only and is not an offer or solicitation with respect to any securities. Any offer of securities can only be made by written offering materials, which are available solely upon request, on an exclusively private basis and only to qualified financially sophisticated investors.

The information was obtained from sources we believe to be reliable, but its accuracy is not guaranteed and it may be incomplete or condensed. It should not be assumed that investments made in the future will be profitable or will equal the performance of any security referenced in this paper. Past performance is not a guarantee of future results. An investment involves the risk of loss. The investment return and value of investments will fluctuate.